Even with a peace deal, demand will take time to recover

The US and Iran are expected to sign a peace deal on 19 June, reopening the Strait of Hormuz and gradually restoring seaborne flows. But a deal is not an instant recovery: supply will come in steps, with meaningful divergence across countries and products well into 2027. Our 8th June outlook rests on our de-escalation scenario assumptions we set before the deal was announced, a phased reopening of the Strait from mid-to-late July, normalising by October. Hence, the risks to our demand forecast are skewed to the upside, as the decline, outside of immediate disruption to Middle East activity, has been driven primarily by the physical supply constraints and price transmission effects. A faster recovery in supply and a correction in crude and product prices could push our demand forecast higher.

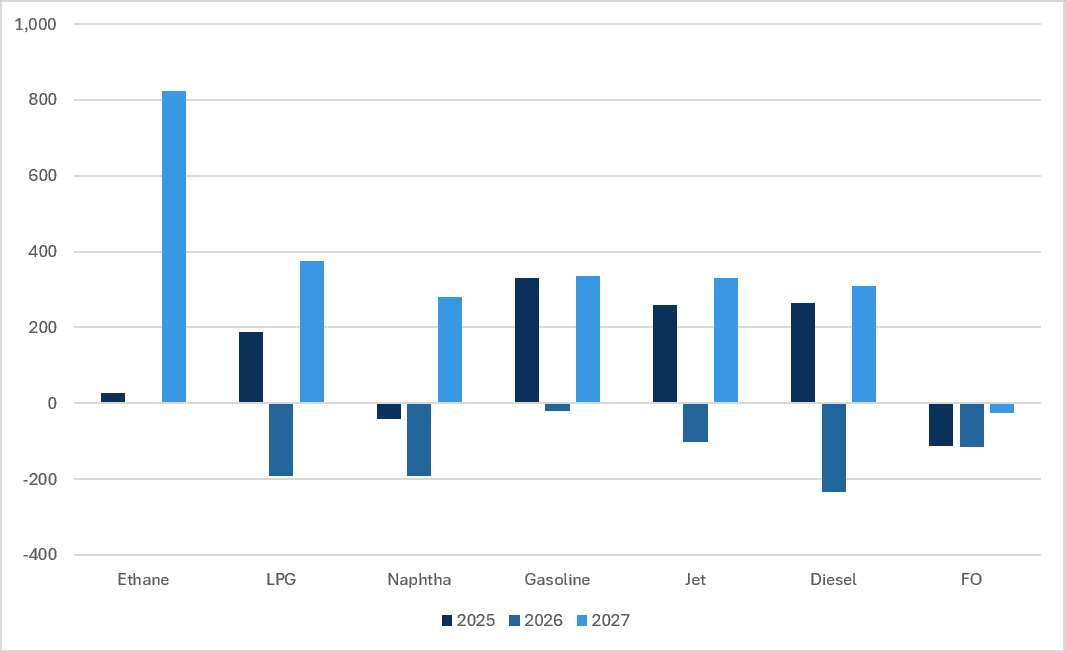

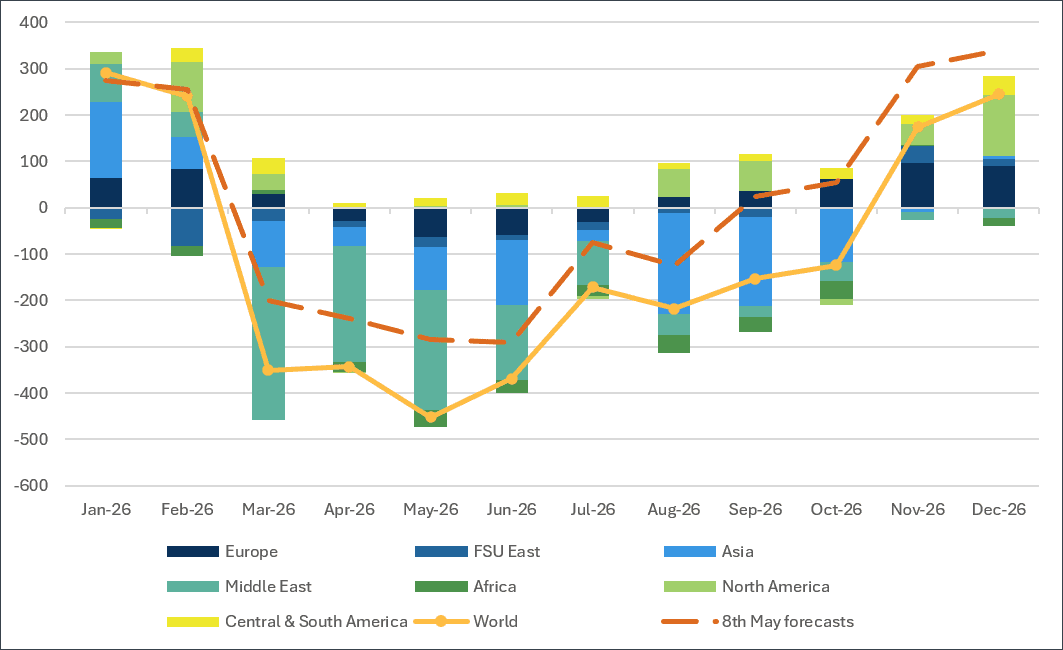

Refined demand growth (y/y, kbd)

Source: Kpler

With a potential re-opening of the Strait of Hormuz on 19 June, we could expect upward revisions to our demand outlook especially for Q3 and Q4. Our preliminary estimates set this year’s demand decline at ~0.7 mbd vs ~1.2 mbd estimated in our early June outlook.

CPP Deep Dive

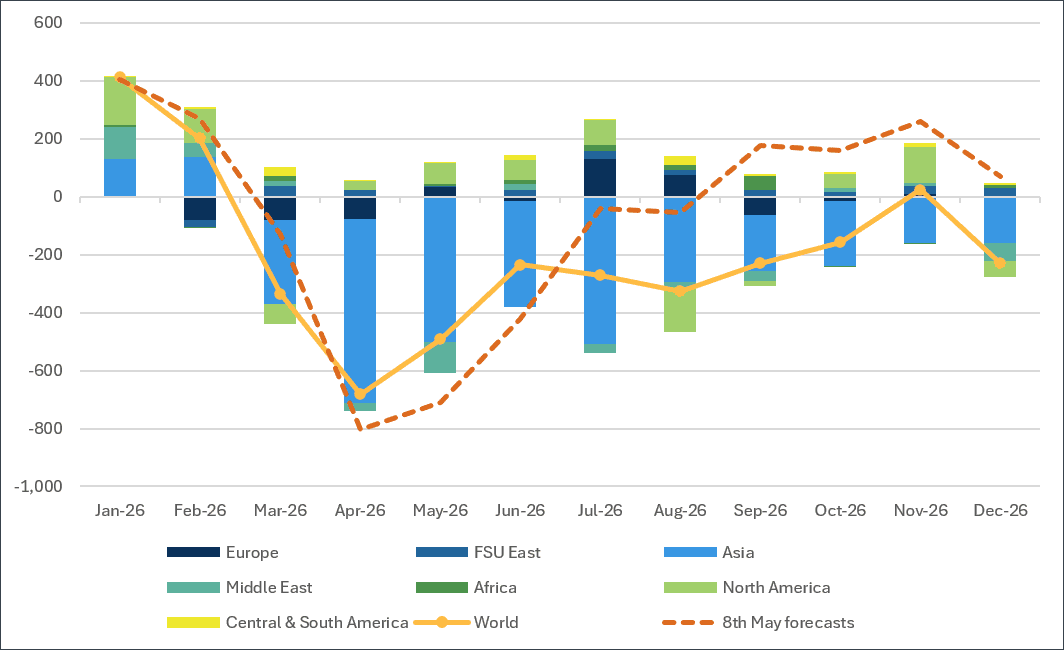

LPG y/y demand growth by region (kbd, 8th June forecasts)

Source: Kpler

LPG demand rose by 190 kbd in 2025 and, pre-conflict, was expected to grow by a further 300 kbd in 2026, supported by around 100 kbd of growth in China, primarily from new PDH capacity additions. We now expect LPG demand to decline by roughly 200 kbd y/y instead, with Asia—particularly India and China—leading the contraction.

India is especially exposed, having relied on the Middle East for more than 90% of its LPG imports in 2025. The conflict had a direct impact on India’s LPG demand as the government took several measures including the rationing of LPG supply to end-use customers. Across Asia, and particularly in China, PDH units were also forced to reduce run rates amid the supply shortage.

That said, we see upside risk to our H2 2026 demand forecast. An effective reopening of the Strait of Hormuz from 19 June, in line with the latest MoU and progress toward de-escalation, could prompt an upward revision of 200–300 kbd, bringing demand closer to our previous May projection. LPG is likely to be among the first commodities to resume flows through the Strait if the peace deal is signed this Friday. This would be particularly supportive for India, given the critical importance of LPG supply security and the country’s likely prioritisation of LPG cargoes through Hormuz.

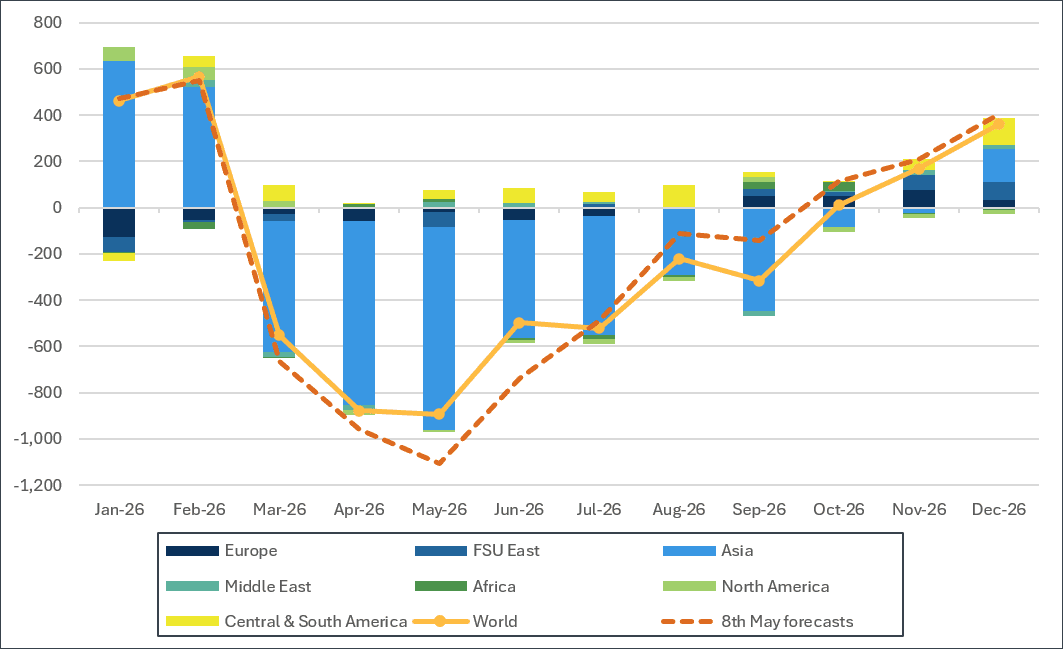

Naphtha y/y demand growth by region (kbd, 8th June forecasts)

Source: Kpler

Naphtha demand fell by 40 kbd in 2025 and is projected to decline by a further ~200 kbd in 2026, reflecting constrained feedstock availability, reduced steam-cracker utilisation, and a slower recovery in petrochemical operations — a downward revision of 330 kbd from the February forecast. The losses peaked in May, by our estimates, when demand fell by an estimated 900 kbd y/y, with the steepest reductions in China, Korea and Japan as they faced petrochemical feedstock shortages and were forced to cut operating rates or declare force majeure. We revised European naphtha demand higher for H1 2026 as cracker restarts lifted operating rates due to stronger margins amid lower Asian supply. However, weaker NWE margins as maintenance eases point to H2 downside risk, especially if the US-Iran deal holds and olefins oversupply returns.

If the US–Iran peace deal goes through, we expect upward revision to the tune of ~80 kbd in H2 2026 to our naphtha forecast as supply increases, based on preliminary estimates, with refiners in Asia increasing crude runs coupled with the return of imports from the Middle East. However, naphtha imports recovery is expected to be gradual as commodities deemed more critical to essential needs — crude, LNG, diesel, LPG and fertiliser — will be prioritised for movement through the Strait.

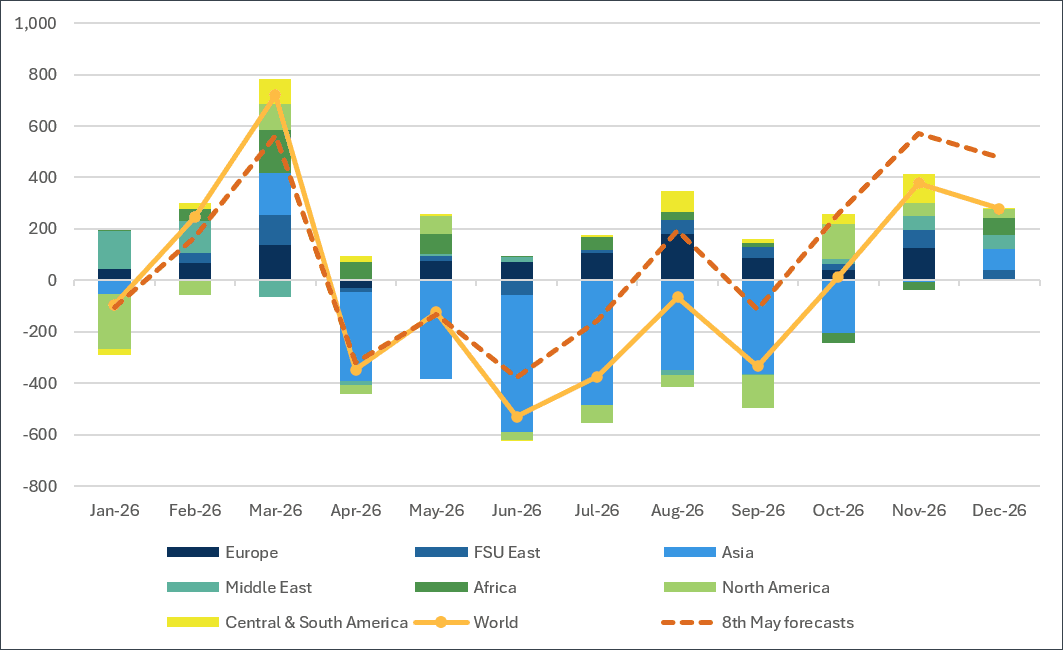

Gasoline y/y demand growth by region (kbd, 8th June forecasts)

Source: Kpler

Gasoline demand grew by 330 kbd in 2025 but is now expected to fall by ~20 kbd in 2026, a downward revision of ~130 kbd from pre-conflict forecasts. We expect the losses to peak in June 2026, with Asia leading the decline. While most of the fall reflects supply shortages, government-led conservation measures and higher pump prices are adding to the drag. The war has also sharpened the slide in China's gasoline demand, compounding the structural erosion already under way from accelerating electric-vehicle adoption. We expect demand to stay weak through Q3 while fuel costs remain high, and gasoline supply remains constrained.

With the US–Iran peace deal, we could expect upward revision to our demand outlook to the extent of 100-150 kbd in Q3 and Q4 2026, especially in Asia as supply increases and retail prices are expected to correct.

Jet fuel/Kerosene y/y demand growth by region (kbd, 8th June forecasts)

Source: Kpler

Jet demand rose by 260 kbd in 2025 and is projected to fall by 100 kbd y/y in 2026. Based on our estimates, losses peaked in May 2026, led by the Middle East, where demand was directly disrupted by the closure of regional air routes.

We have also revised down our Q2 and Q3 jet demand forecasts by 500 kbd and 380 kbd, respectively, compared with our 9 February outlook. The largest downward revisions are concentrated in the Middle East and Asia. These cuts reflect the impact of elevated jet fuel prices, which have increasingly weighed on airline economics and prompted several carriers globally to rationalise capacity or suspend selected routes that have become commercially unviable. We have also lowered our demand outlook for Europe, particularly the UK and France, as well as Africa, given their high dependence on Gulf imports and increased exposure to supply disruptions.

However, with a potentially earlier resolution of the conflict, we may see upward revision to our demand outlook to the extent of 100 kbd through August to Dec 2026 on average, as supply increases and jet prices decline.

Gasoil/Diesel y/y demand growth by region (kbd, 8th June forecasts)

Source: Kpler

Diesel demand, after growing by 260 kbd in 2025, is projected to fall by around 230 kbd in 2026, with a particularly sharp Q2 drop of 740 kbd y/y. The downturn reflects a swing from ~400 kbd y/y growth in Q1 2026, with the Q2 fall led by Asia, Europe and Africa. In Asia, the decline reflects supply disruptions caused by the closure of the Strait of Hormuz, the demand-curbing measures that followed, and the impact of higher fuel prices on already structurally weakening Chinese diesel consumption. In Africa, demand also declined as lower supply availability weighed on consumption, given the region’s high dependence on Gulf imports and limited inventory buffers. In Europe, a sharp rise in diesel prices further pressured demand that is already in structural decline, as passenger car fleets continue shifting away from diesel toward hybrids, EVs, and gasoline-powered vehicles. Looking ahead to Q3 and Q4, diesel demand is expected to remain under pressure from supply disruptions, elevated diesel prices, and weakening industrial and freight activity following GDP downgrades across regions, particularly in Asia and Africa.

However, If the US–Iran peace deal goes through, we see scope for our diesel demand outlook to be revised higher by around 300 kbd over August to end of year, as industrial activity recovers and diesel prices ease from the historical highs reached in Q2.

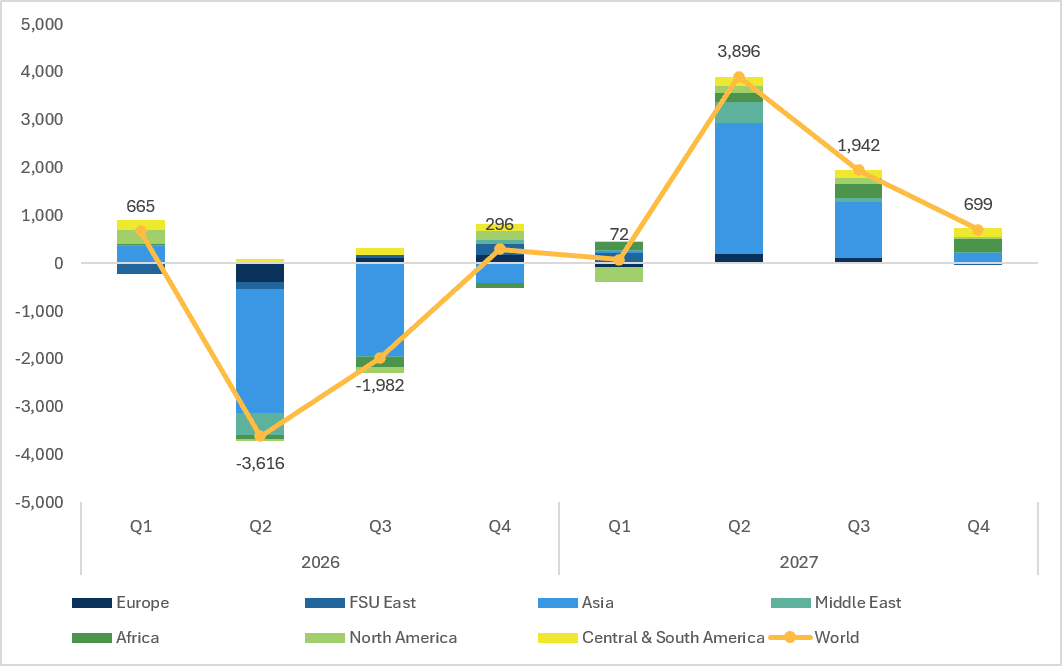

Recovery outlook: a temporary dislocation, not destruction

We continue to treat the 2026 demand shock as a temporary dislocation rather than structural demand destruction. We expect demand to begin to recover from Q4 2026, once supply normalises. However, the lost ground will take time to recover. Demand for refined products is now unlikely to reach around 103 mb/d even by 2027, compared with our previous expectation that it would reach that level in 2026. Despite the Strait reopening, refined product prices are expected to stay elevated while inventories are rebuilt and trade flows re-route, capping how quickly demand can respond.

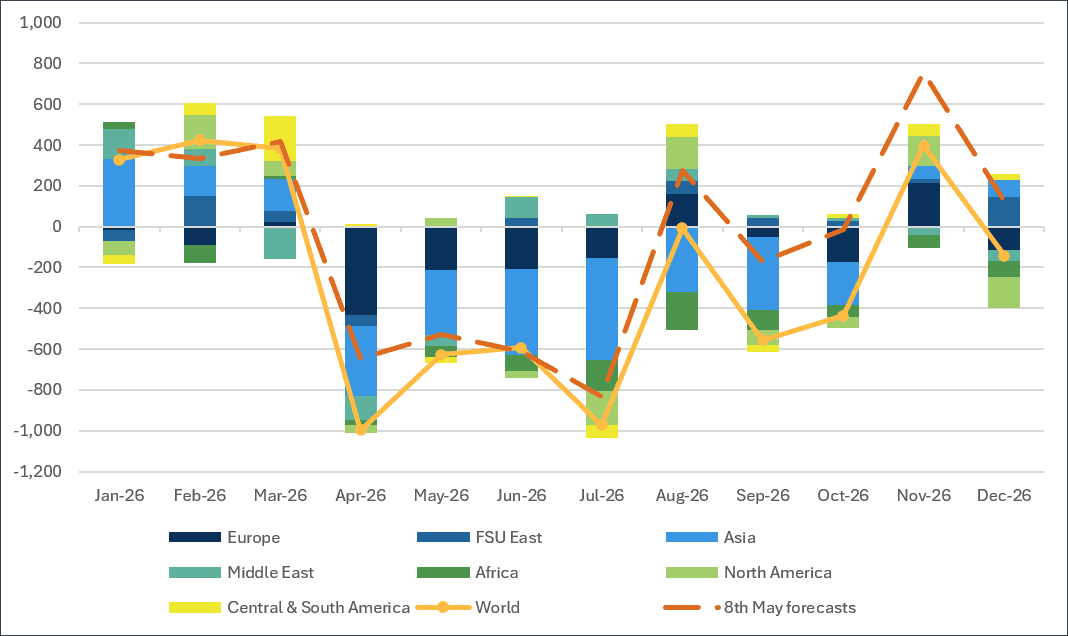

Refined products y/y demand growth by region (kbd, 8th June forecasts)

Source: Kpler

See why the most successful traders and shipping experts use Kpler