Ras Laffan loading activity poised to pick up as available ballast tonnage increases

Satellite imagery and AIS data point to a sizeable buildup of ballast Qatari tonnage at and around Ras Laffan, with ~17 vessels potentially available to load. While this signals a likely ramp-up in exports following weeks of reduced terminal activity, the additional volumes will not hit the market immediately — transit uncertainty through the Strait of Hormuz remains a key bottleneck, with two vessels attempting to enter already observed performing U-turns. Once clear of the MEG, most of these cargoes are expected to head to Asia during peak restocking season.

Market and Trading calls

- Increased loadings at Ras Laffan as more ballast tonnage is expected to enter the MEG while the vessel count at Ras Laffan anchorage builds up

- Bearish pressure on TTF and JKM as the market prices in the potential increase in Qatari supply

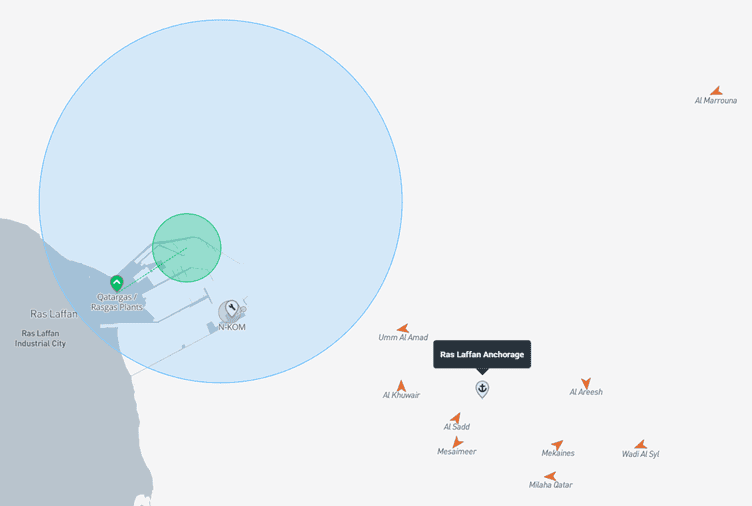

Recent satellite imagery indicates an increase in ballast Qatari tonnage inside and outside the MEG, indicating a possible increase in the pace of loadings at the 77 mtpa Ras Laffan terminal. As of 26 June 15:00 GMT, 9 Qatari vessels (0.7 mt of combined loading capacity) are idling at Ras Laffan anchorage – Al Marrouna, Wadi Al Syl, Mekaines, Milaha Qatar, Mesaimeer, Al Sadd, Al Khuwair, Al Areesh and Umm Al Amad. Four of these vessels are Q-Flex/Q-Max, the rest are conventionals. Kpler Insight is also monitoring approximately 8 other ballast Qatari vessels that are currently operating “in the dark” – with their last AIS signal having been received at least 4 days ago, and are thus believed to be at various stages of entering the MEG. This amounts to a total of ~17 ballast Qatari vessels that could be available to load at Ras Laffan. Two vessels – Shandong Redwood and Al Kharaitiyat – are also currently berthed at the terminal and are likely loading.

Ballast vessels idling at Ras Laffan Anchorage

Source: Kpler. Screenshot taken on 26/06/26 15:00 GMT

On average, Ras Laffan loads 2.9 vessels per day during this time of year (using a 2-month average of daily loadings for June and July 2025). For comparison, so far in June, the average loading rate has been 0.5 vessels per day – reflecting the intermittent pace of activities in recent weeks. Indeed, the terminal is currently operating at reduced capacity - Kpler thermal imagery on 22 June confirmed that activity is taking place at only five trains (QatarGas T5 and RasGas T1, 2, 3, 7). This equates to approximately 35% of the terminal’s total nominal capacity. It is also worth noting that thermal activity is not necessarily indicative of actual LNG production levels.

In addition, there were rumours of possible damage to at least one of the six jetties at the facility following March’s drone attacks. While there has been no official confirmation, Kpler analysis shows that only jetty No.2 has not received any vessels since the attacks.

Given these constraints and accounting for some congestion time and delays (especially for the vessels operating in the dark), we could therefore estimate that these 17 vessels could theoretically load within ~25 days, adding up to 1.6 mt of LNG to the market (assuming full loads). This would also include the LNG from the two vessels currently docked at the terminal. This timeline could even be shortened if more trains come online. Moreover, QatarEnergy has reportedly not sent its usual ~1 month advance notice to customers of force majeure renewal for July, implying that it may look to resume normal supply obligations to Asian buyers.

However, this additional LNG will not necessarily hit the market immediately. Indeed, once laden, getting these vessels out of the MEG will take some time, due to ongoing uncertainty regarding transit safety. Earlier this afternoon, two ballast vessels (Umm Slal and Gaslog Shanghai) were detected doing a U-turn as they attempted to cross the strait, in a context where the IRGC navy has issued warnings against “unauthorized” Hormuz passage. This could limit transit tonnage going forwards if this threat persists and delay laden vessels looking to exit the strait. It is likely that some laden vessels will cross with their AIS on, while others will go dark, in a similar fashion to the ballast Qatari vessels entering the MEG earlier this week.

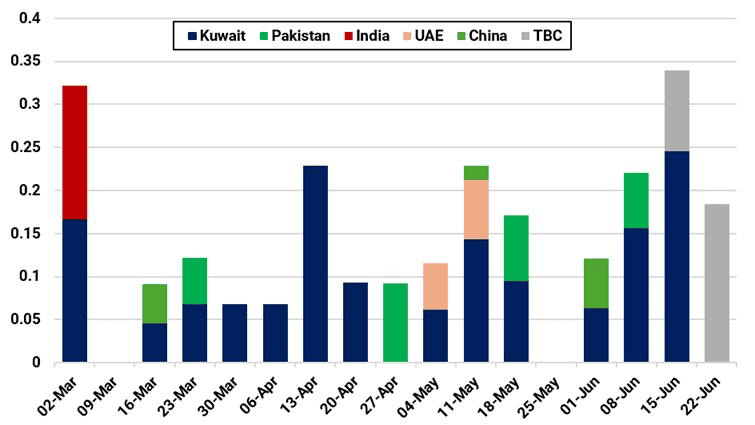

Weekly Ras Laffan exports by destination country (mt)

Source: Kpler

Lastly, once these vessels exit MEG, it is likely that most of these volumes will head to Asia, as we enter the start of peak restocking season in the JKTC region. Kpler Insight’s latest forecast for July Qatari exports is 2.2 mt, with possible upside risk if flows pick up quicker than expectations.

See why the most successful traders and shipping experts use Kpler