Rebalancing the liquids markets amid SOH disruption

In this Market Pulse, we analyse how the market is rebalancing after the removal of around 20 Mbd of flows through the Strait of Hormuz. The adjustment is being driven by supply cuts, refinery run reductions, limited rerouting, demand erosion, and inventory drawdowns, but remains incomplete, leaving the system structurally tighter.

Sixty days into the disruption, the Strait of Hormuz continues to operate at minimal capacity, with only limited vessel movement observed. What initially appeared as a logistical bottleneck has now evolved into a prolonged structural dislocation, significantly reducing the flow of crude and refined products from the Middle East Gulf into global markets.

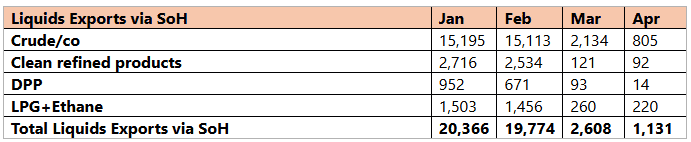

As shown in Table 1, flows through the Strait have collapsed from around 20 Mbd pre-disruption to nearly 1 Mbd in April, highlighting the scale of the supply shock.

Table 1 (kbd)

Source: Kpler

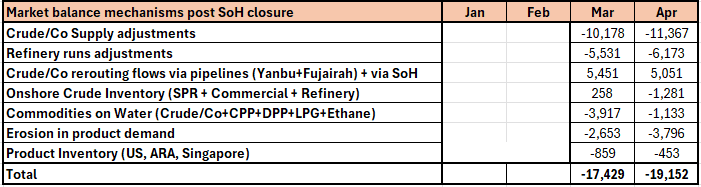

The market has responded through a multi-layered adjustment process, combining supply-side curtailments, refinery run cuts, logistical rerouting, demand erosion, and inventory drawdowns, as detailed in Table 2.

The primary response has come from crude supply reductions, with producers curtailing output as export routes remain constrained. This has been reinforced by refinery run cuts, particularly in the Middle East, where refinery disruptions and export bottlenecks have pushed utilisation to multi-year lows. In Asia, as a crude import-dependent region, tighter feedstock availability is also limiting throughput. Refinery run cuts and supply losses are expected to persist as long as the Strait remains constrained; under our base case assumptions, only a partial recovery in flows is anticipated from June, followed by a gradual improvement thereafter. Together, these two levers account for the bulk of the immediate rebalancing.

Table 2 (kbd)

Source: Kpler

Note: March and April data is change wrt to the pre-war (February data)

Logistical adjustments have provided only partial relief. Pipeline rerouting, most notably via Saudi Arabia’s East-West pipeline and the UAE’s crude flows routed via Fujairah, has increased, with incremental volumes of around 2.9 Mbd in March and about 4.2 Mbd so far in April compared to January–February levels. However, these flows remain structurally limited and fall well short of replacing lost seaborne volumes. Similarly, barrels already on water have been redirected to deficit regions, helping smooth near-term imbalances but offering only temporary support.

On the demand side, early signs of consumption erosion are emerging, particularly across price-sensitive regions such as Asia, East Africa, and Latin America. Higher freight costs and tighter availability are gradually feeding through into end-user pricing, resulting in demand softening, albeit with a lag.

Inventories continue to act as a key buffer. Drawdowns across onshore and commodities on water, along with key hubs such as ARA, the US, and Singapore, are helping bridge supply gaps. However, inventory support remains finite and cannot sustainably offset prolonged disruptions.

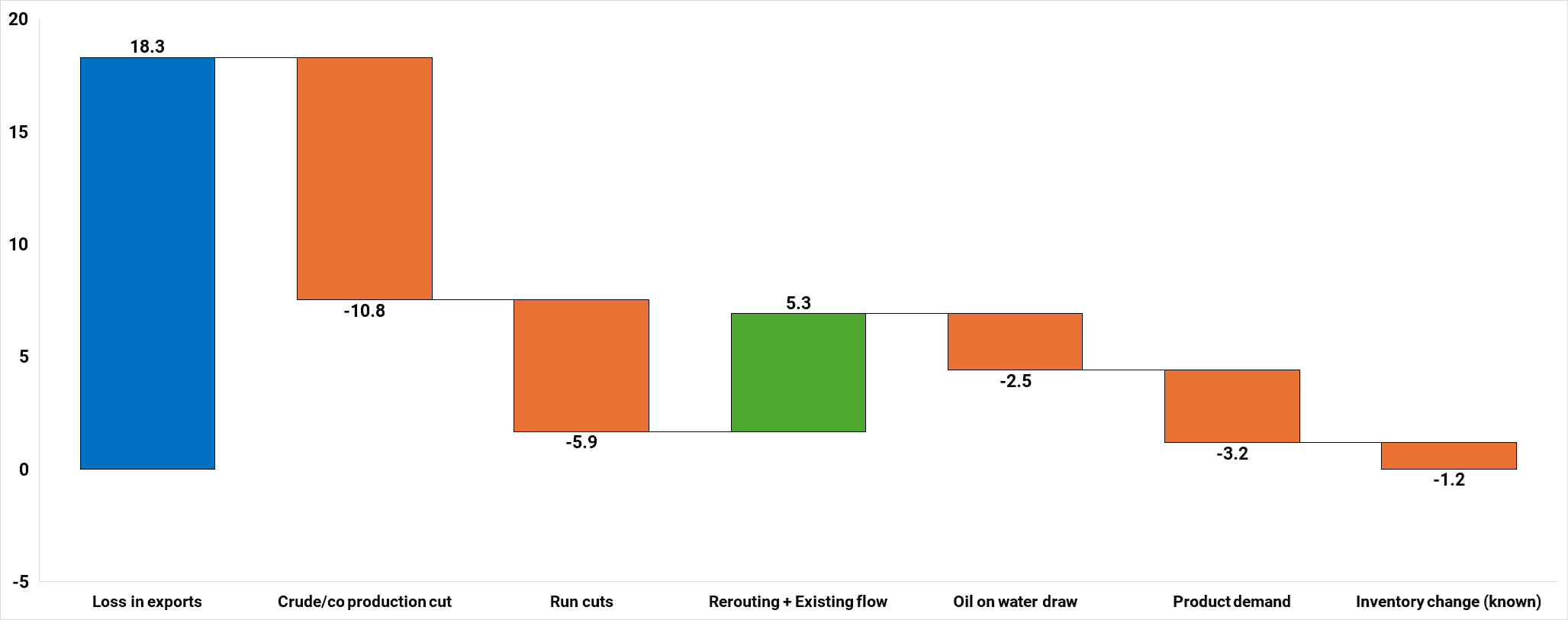

Rebalancing of Lost SoH Flows (Mbd)

Source: Kpler

Note: March & April average data points

As shown in the chart, over two-thirds of the rebalancing has come from supply curtailments and refinery run cuts, highlighting the limited flexibility of alternative adjustment mechanisms.

In effect, the rebalancing is occurring through:

- Upstream supply curtailments (primary adjustment)

- Refinery run cuts (secondary but significant)

- Limited rerouting of flows

- Demand erosion

- Crude and product inventory drawdowns across onshore storage, refineries, and terminals

- Oil on water drawdowns

However, these mechanisms are redistributive rather than additive. The system is not replacing lost Middle East Gulf barrels; it is absorbing them.

Conclusion

The global oil market is now operating in a low-flexibility, high-friction environment, where supply losses are being offset through constrained adjustments rather than new supply. While a gradual recovery is expected under the base case from June onward, the rebalancing remains incomplete.

In essence, the market is solving a 20+ Mbd disruption primarily through supply destruction rather than replacement. The loss of Strait of Hormuz flows is not being replaced, only redistributed, leaving the system structurally tighter and increasingly reliant on inventories and demand adjustment to maintain cohesion.

Market insights you can actually trust

Kpler delivers unbiased, expert-driven intelligence that helps you to track critical crude oil market developments for your own analysis. Our precise forecasting empowers smarter trading and risk management decisions. In times of conflict and geopolitical uncertainty, our real-time data keeps you ahead of supply disruptions and price volatility.

Unbiased. Data-driven. Essential. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler