Renewables extend CWE correction as German wind keeps volatility alive

Week 10 opens with a bearish bias in France amid mild weather, rising hydro reserves and a fundamentals-driven 4 GW nuclear adjustment, while Germany remains slightly bullish as wind revisions and thermal outages keep upside risks in play. In Week 8, renewable surge across CWE slashed residual demand by -14 GW, and drove a 20–30% w/w spot price correction, especially France that witnessed repeated zero and negative price events.

Executive Summary

Week-Ahead Market & Trading Calls - Week 10 2026

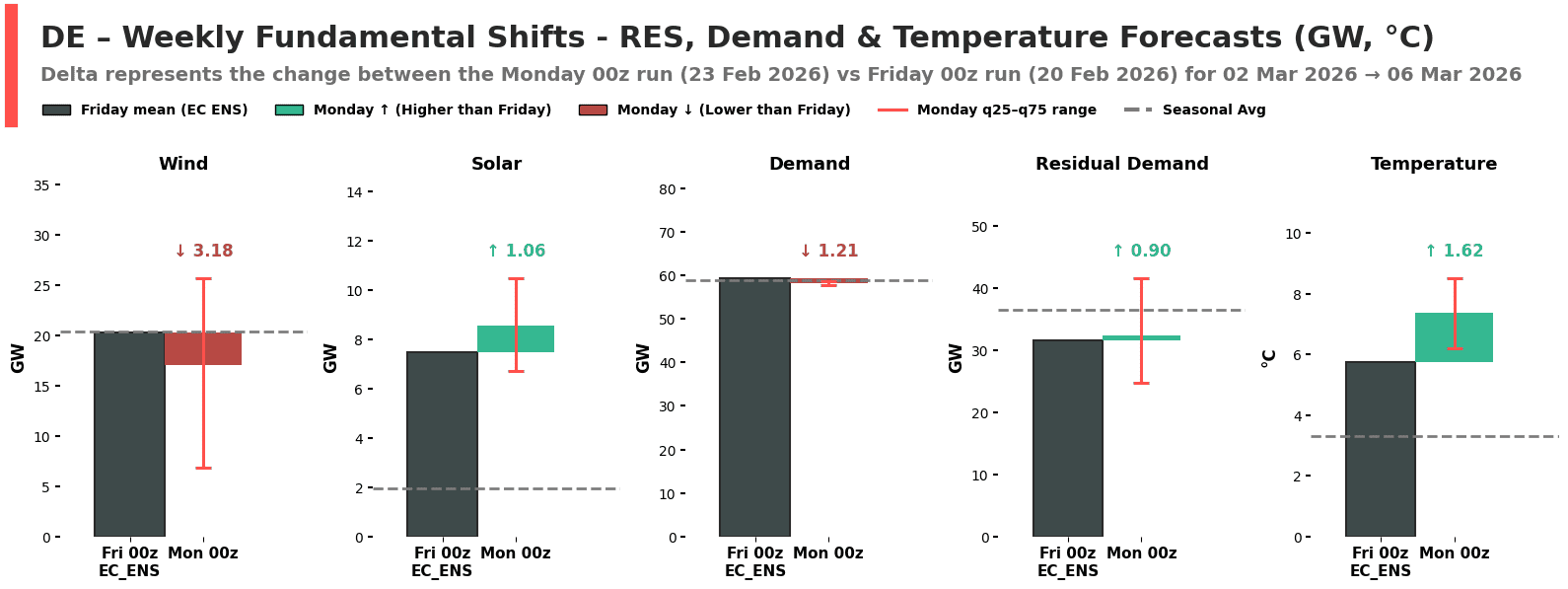

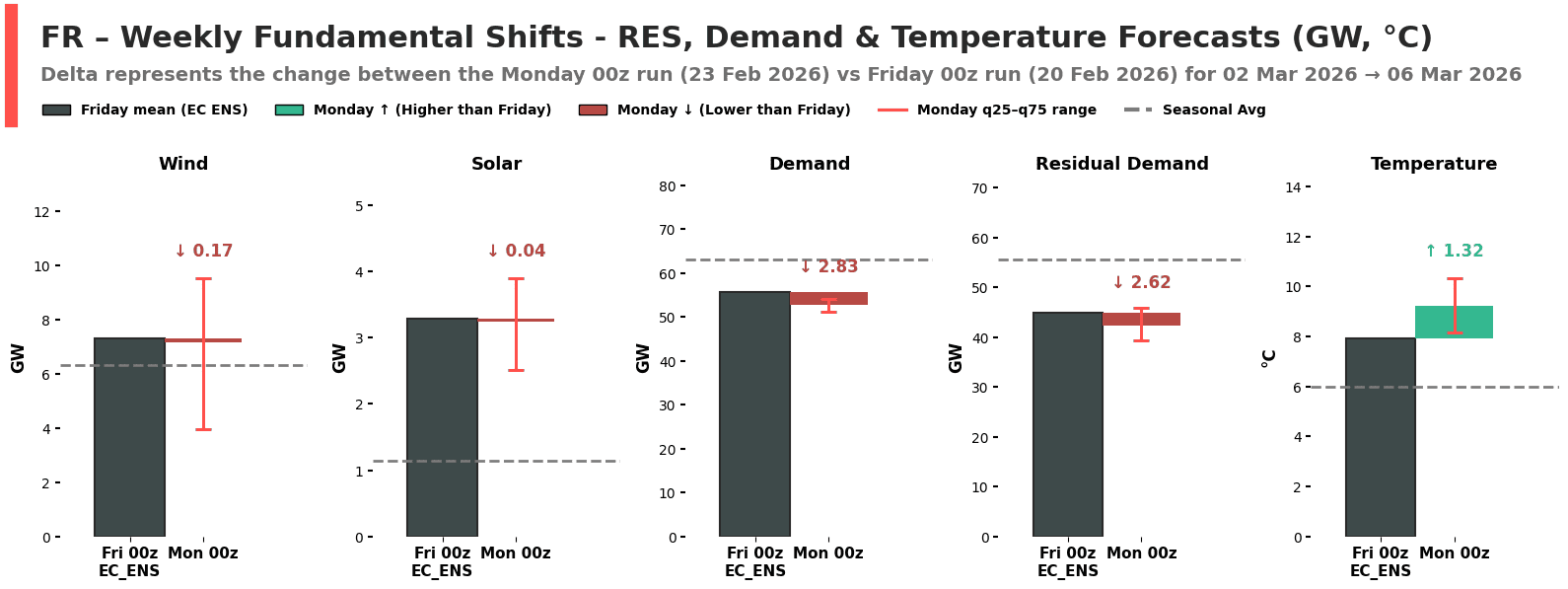

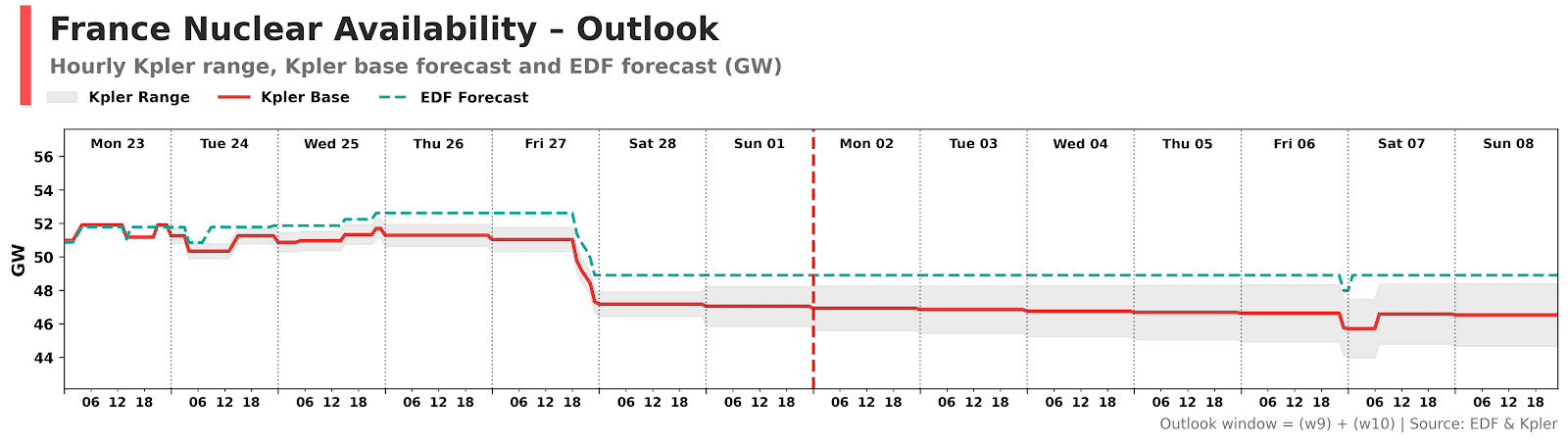

- France: Bearish, as the latest fundamental view reinforces the milder weather trend. Higher temperatures and replenishing hydro stocks ease pressure on demand and add flexibility to the mix. Amid winds above seasonals, Kpler Insight views next week’s 4 GW decline in nuclear availability as a fundamentals-driven adjustment rather than a sign of fleet weakness.

- Germany: Slightly Bullish, as wind revisions are keeping upside risks in play, with models now broadly converging toward 10–15 GW average wind output over the first three days of Week 10. Net thermal stack.

- DE-FR spread: Bullish, reflecting a bearish outlook for France versus a stable-to-bullish stance on Germany.

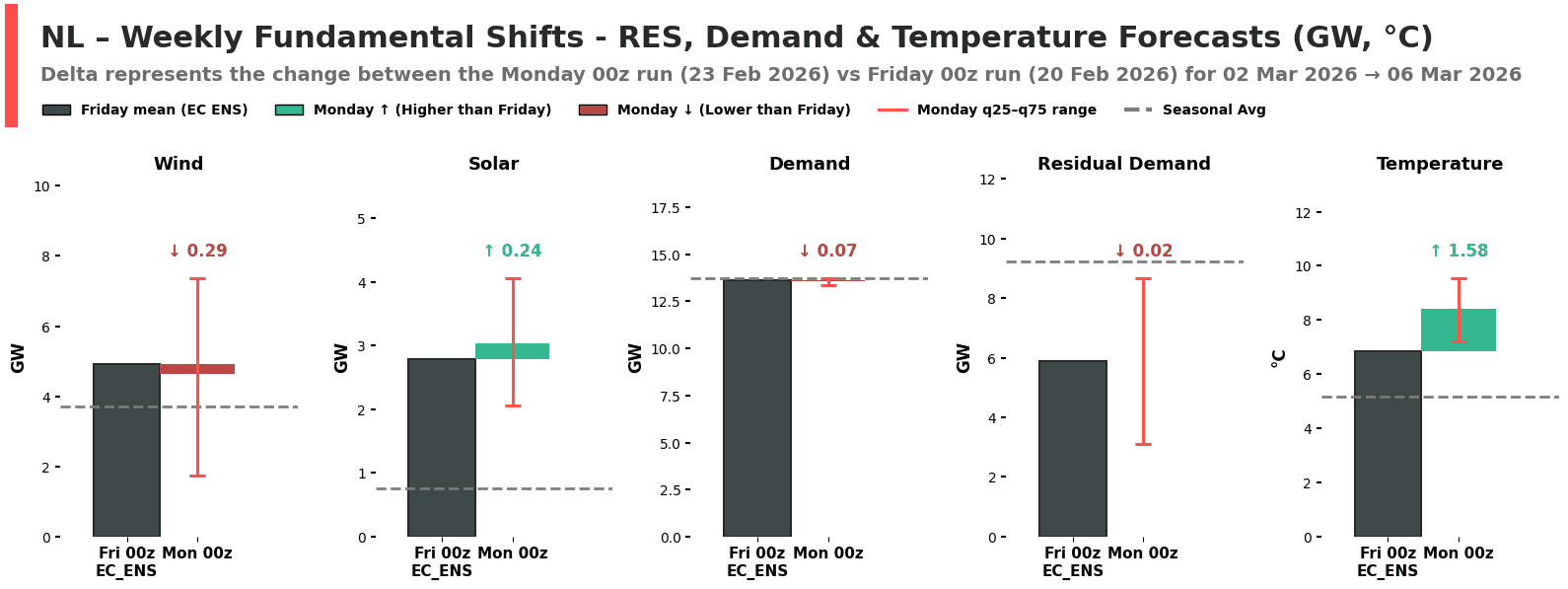

- Netherlands: Slightly Bearish, as milder weather eases demand across the region and offsets the 300 MW slight drop in wind output.

- TTF front-month: Slightly bearish, as warmer temperatures are forecasted across most of Europe. Ample pipeline supply remains available, with a notable increase in imports from the UK. However, downside revisions to the wind forecast provide some upside for gas-fired generation. Heightened geopolitical risk due to the US-Iran nuclear talks remain the main source of price upside.

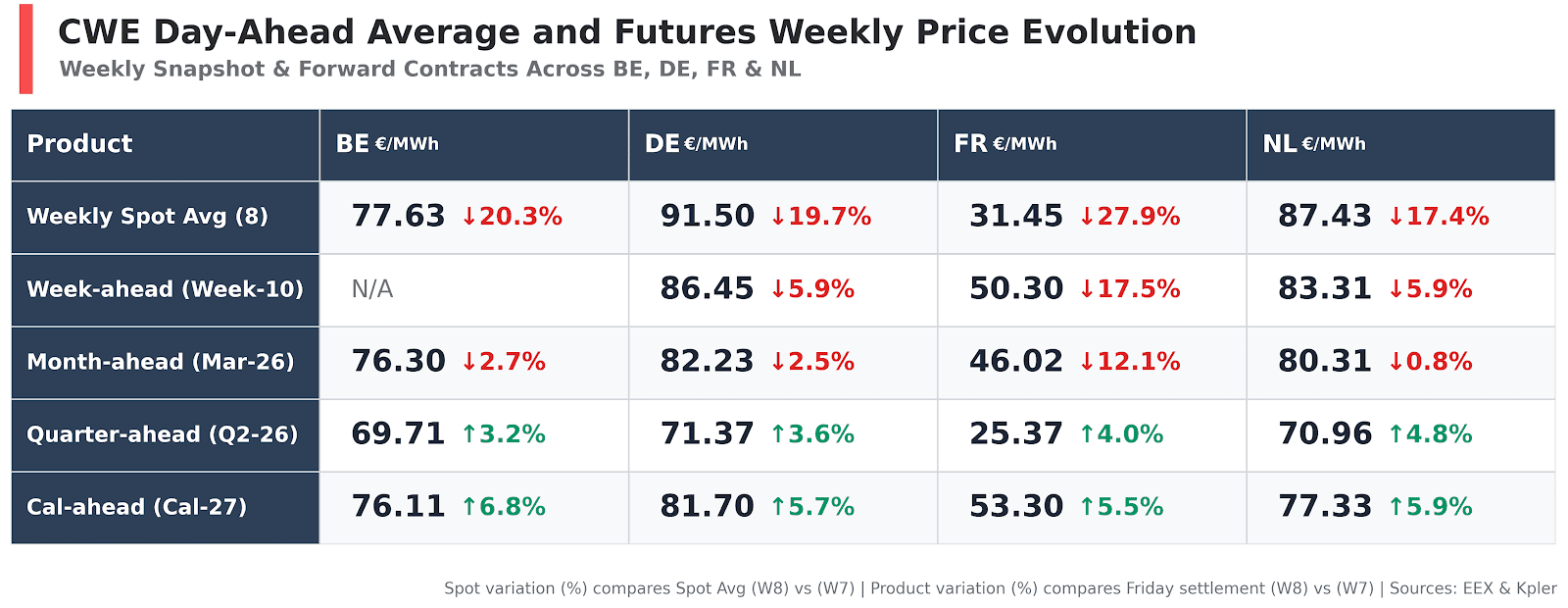

CWE Weekly Review - Week 8 2026

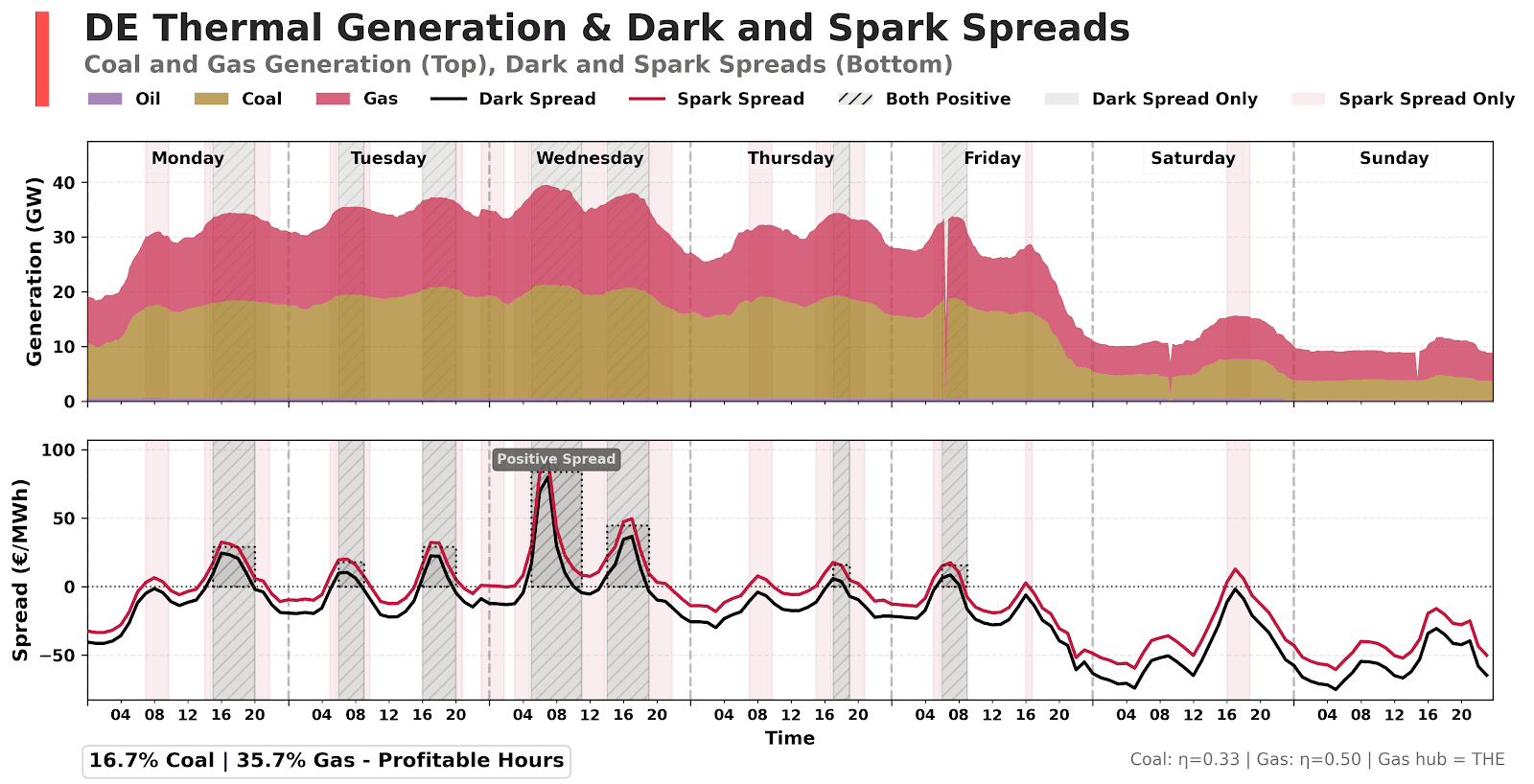

- CWE spot prices dropped sharply by 20–30% w/w, driven by a strong renewable surge that materially eased regional fundamentals. Week 8 marks the first week of solar coming back to make an impact in wholesale price formation. France led the correction, with day-ahead prices falling -28 % to 32 €/MWh, marking the steepest decline across core markets.

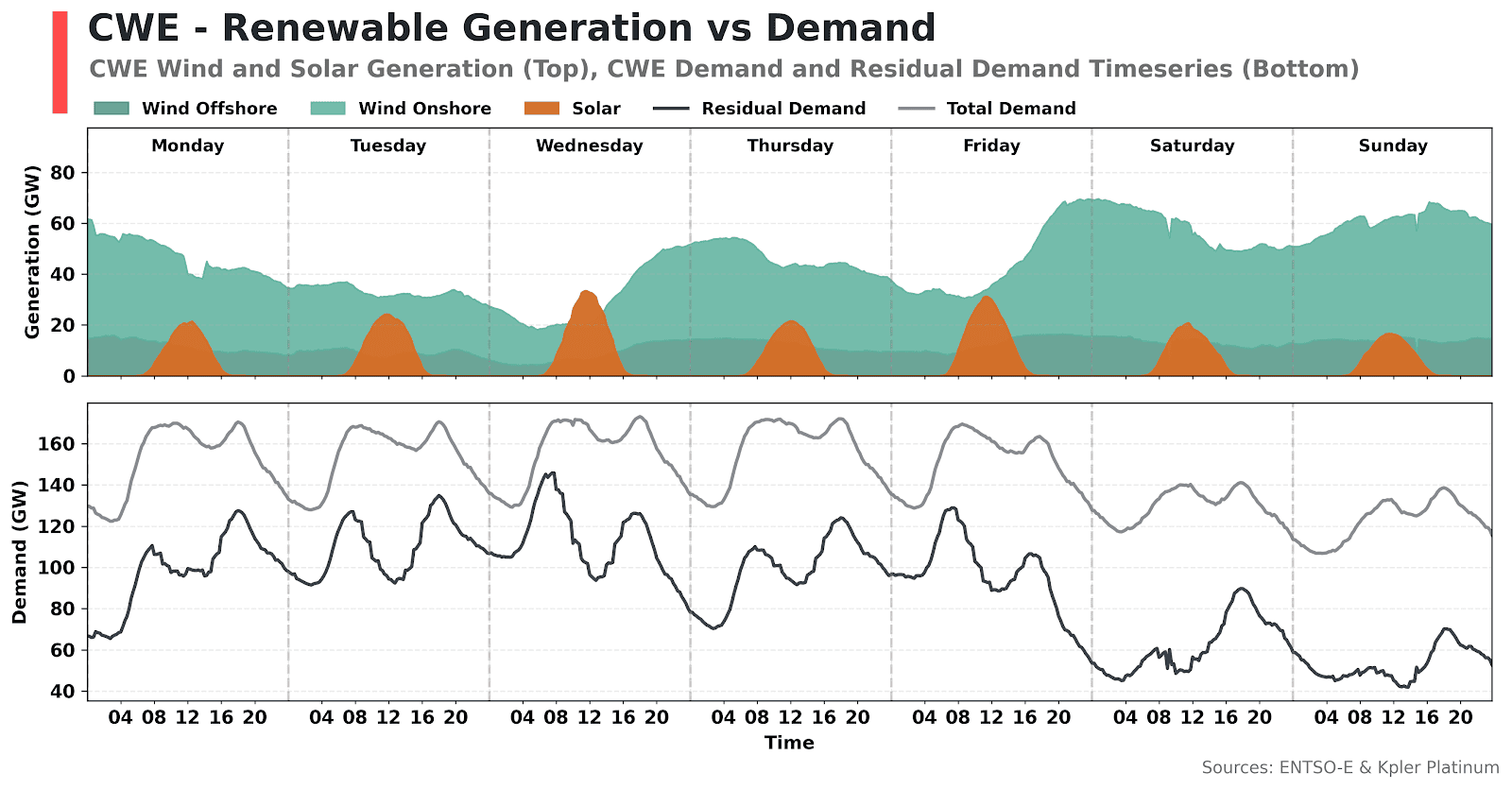

- France recorded multiple zero and negative-price events, similar to Week 7, which significantly dragged the weekly average lower. This occurred despite a +1.5 GW increase in total demand, as stronger wind generation combined with solar output during daytime hours pushed prices down. The midday oversupply forced curtailment of roughly 3-5 GW of wind capacity multiple times throughout the week.

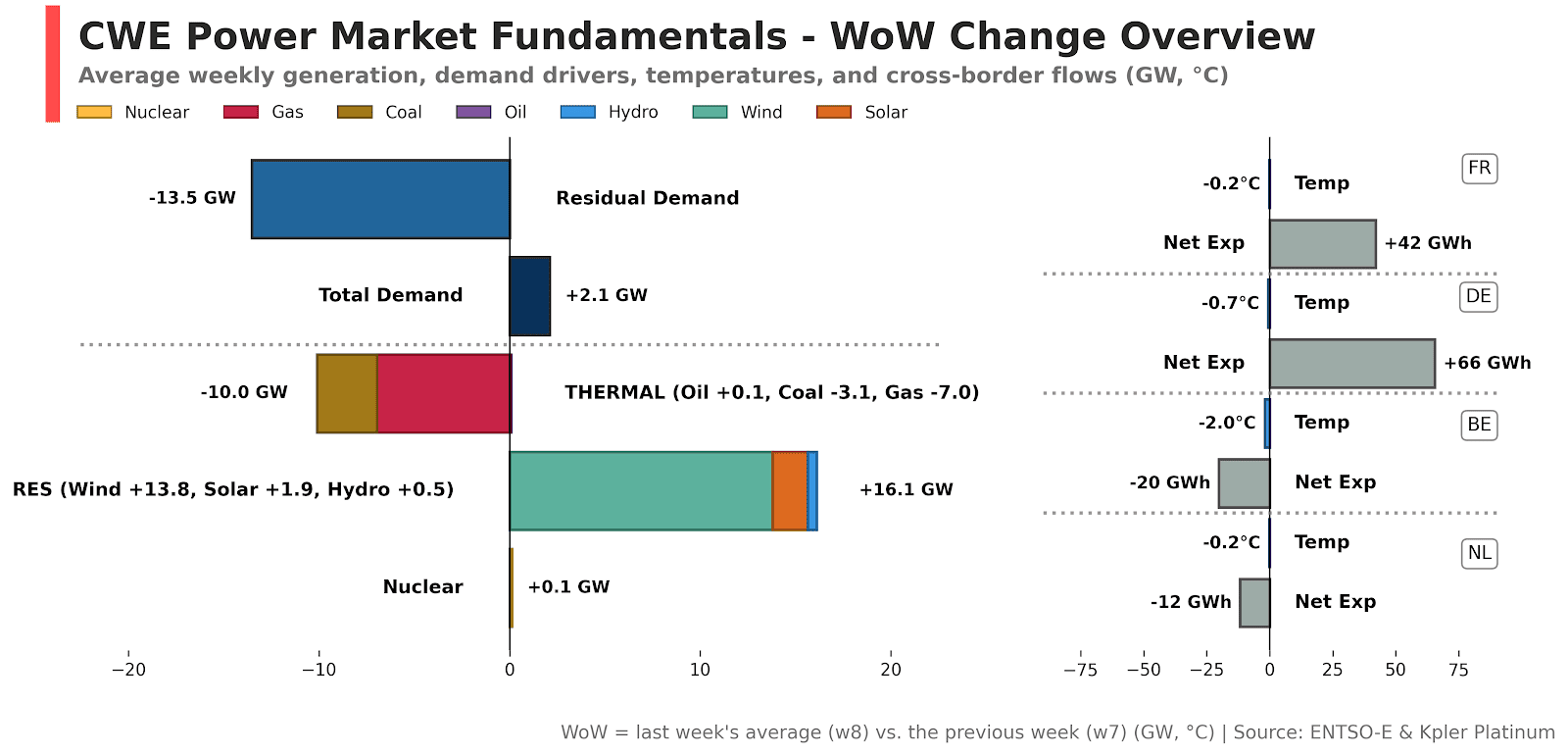

- At the regional level, renewables increased by +16 GW across CWE, driving residual demand down -13.5 GW w/w and displacing nearly -10 GW of thermal generation w/w. Germany was the primary contributor, accounting for roughly 50% of the fossil pullback with around 9 GW of additional renewable output. As a result, dark spread profitability hours fell below 20 % for the first time this year, while spark spreads showed higher resilience at 36 %. This marks a steep decline from 40% and 60% in Week 7.

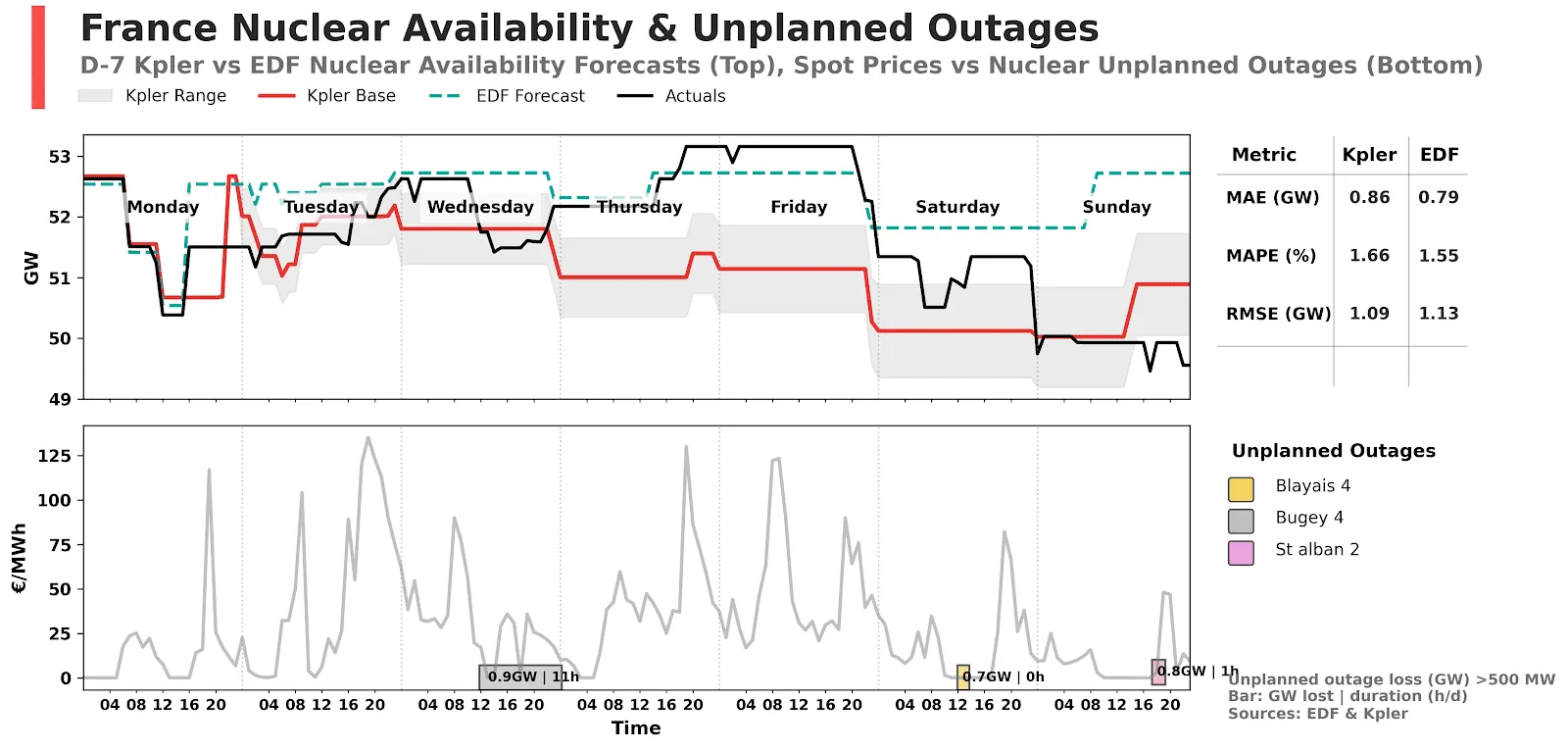

- Unplanned outages remained limited on the French nuclear side. To note only Bugey 4 was the most significant event, losing 9.7 GWh over 12 hours. Germany marked only a 1-day major thermal outage on Monday 16 Feb. from the Kraftwerk Rostock plant.

Market & Trading Calls - Week 10 2026

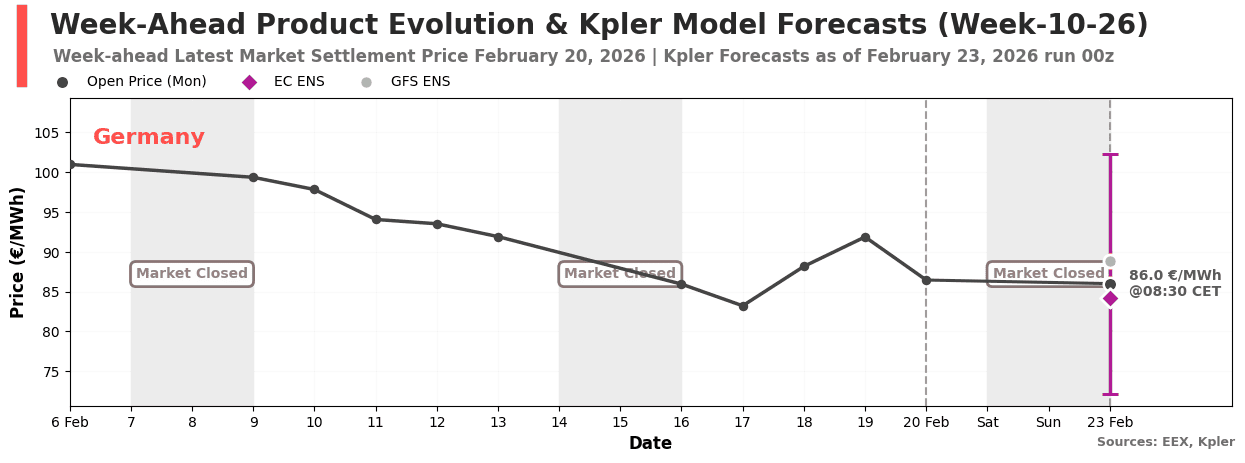

Germany

Germany’s week-ahead Monday price opens flat at 86 €/MWh vs Friday.

Sunnier and milder weather should ease demand through stronger net injections and higher behind-the-meter solar generation. On the other hand, wind revisions are keeping upside risks in play, with models now broadly converging toward 10–15 GW average wind output over the first three days of Week 10. Meanwhile, the thermal stack is set to lose 1.2 GW of available capacity, adding pressure during already tight hours.

About gas and carbon: Kpler Insight maintains a slightly bearish view on next week’s TTF front-month contract. This is supported by a broadly weaker EU ETS, pressured by political signals, including German Chancellor Merz’s willingness to revise the system to safeguard EU industrial competitiveness, and Italy’s decree to reimburse electricity costs linked to EU ETS. Ample pipeline and LNG supply also remain available. However, a narrowing Asian LNG/TTF spread and tighter US-to-Europe arbitrage could lend some upside support. For TTF the geopolitical risk remains a key upside factor, with US–Iran tensions around the Strait of Hormuz still elevated.

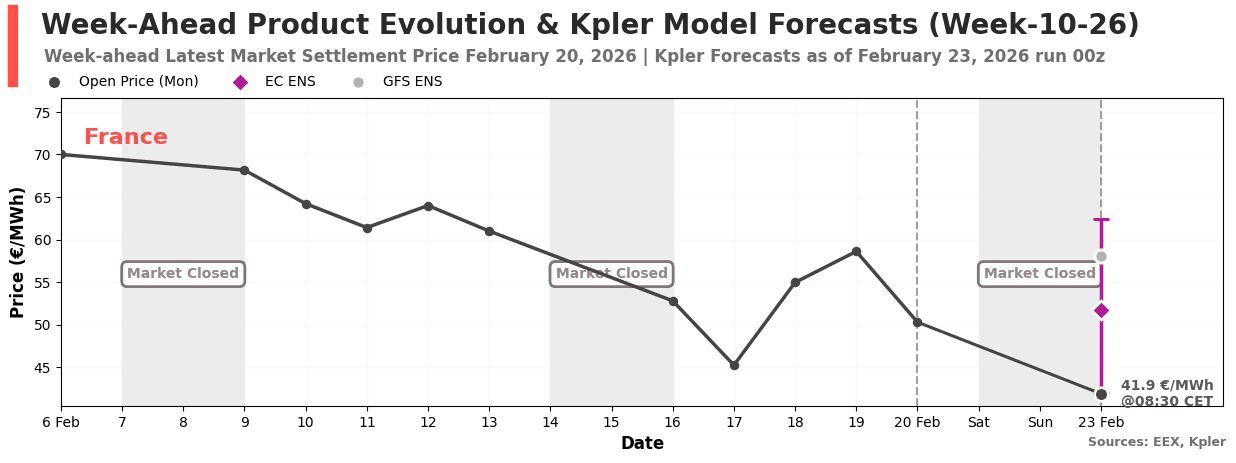

France

France’s Monday open price opens bearish at 41,9 €/MWh, 20% below Friday settlement.

After two consecutive weeks with average prices below 30 €/MWh, the week 10 fundamental outlook continues to point to downside pressure. Milder and wetter conditions are supporting hydro reserves, while higher temperatures are keeping demand subdued. As a result, hydro output is less needed in the current low-demand environment.

Residual demand is expected to remain around 2 GW below available nuclear capacity. Kpler Insight views the projected 4 GW decline in nuclear availability next week as a fundamentals-driven adjustment rather than a sign of fleet weakness, reinforcing the bearish outlook. This points to prices potentially readjusting to the 30 €/MWh regime.

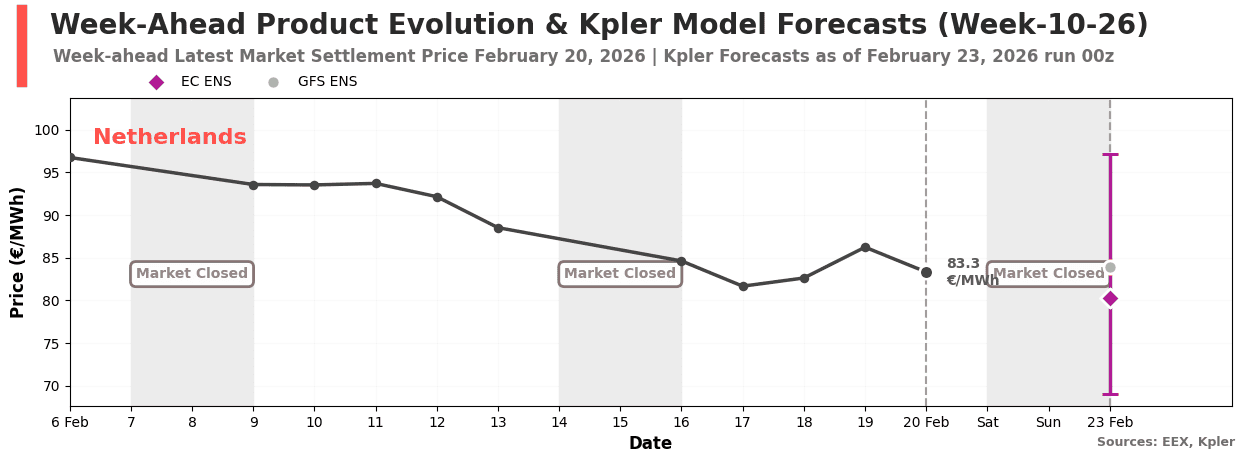

Netherlands

The Netherlands’ week-ahead market on Friday saw settlement price at 83.3 €/MWh, with Kpler price forecasts providing a slightly bearish outlook. The primary driver is a 1.5 °C rise in average weekly temperature (Monday vs Friday delta), which eases demand levels. Amid stable residual demand weekly average levels, it is important to note the offset is mainly driven by a 300 MW drop in wind output and an average 300 MW increase in solar output, which can increase price volatility.

Fundamentals Analysis (latest weather run vs last Friday)

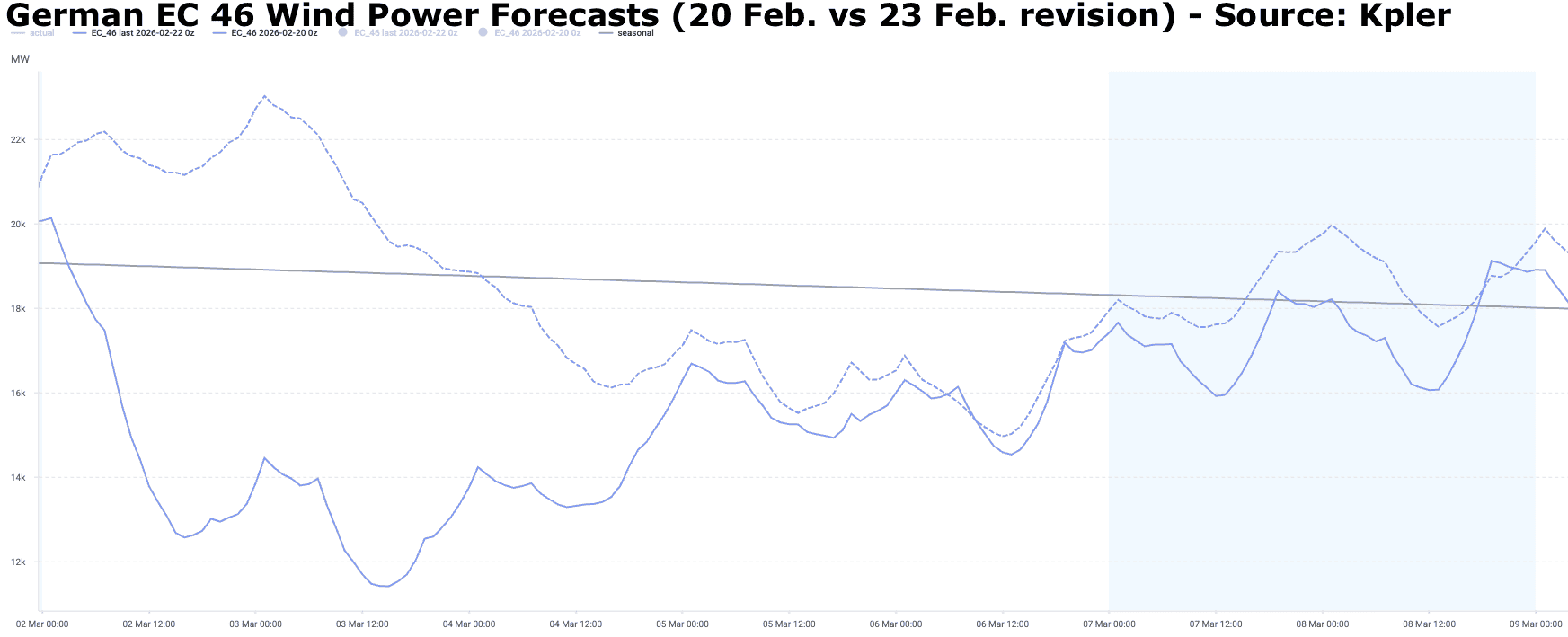

Germany

Germany’s Monday-to-Friday revision shows a downward adjustment in wind output, with wind probabilistic models now skewing below seasonal norms. Early week (Mon to Wed) wind output has been revised down by around 4 GW according to EC ENS and EC AIFS ENS, while GFS ENS points to an even steeper cut of close to 10 GW. All models are now broadly converging toward 10–15 GW average wind output over the first three days of the week.

Meanwhile, sunnier and milder weather is expected to ease demand slightly, reducing load by around 1 GW. The thermal stack is also set to lose 1.2 GW of available capacity, adding pressure during already tight hours.

To watch this week:

- Niederaussem H (500 MW): Planned outage started on Friday 20 Feb., expected to come back on 6 March.

- Niederaussem K BoA 1 (1 GW): at 7 AM this morning the plant published a 1 day planned 150 MW partial outage message.

- Emsland D (870 MW): Unplanned outage at 6 AM this morning, expected to come back at 1 PM.

Long outages:

- Huntorf GT (320 MW): after a 3-day unplanned outage last week, the plant published on Saturday a total outage until 4 May and a longer 200 MW partial planned outage until 31 Aug.

- GKW Hannover Block 1 (140 MW): on Friday the plant published a REMIT planning a full-year outage from 27 Feb. to 31 Dec. The plant should be offline for the rest of 2026.

- Herne Block 4 (520 MW): expected to shutdown Saturday 28 Feb. for a 3-month planned outage.

- Knapsack 2 (440 MW): expected 1.5-month planned outage to start this weekend.

- Irsching 4 (590 MW): expected 1-month planned outage to start this weekend.

Expected to come back for Week 10:

- HKW Reuter West (Block E & D - 560 MW): Block D to ramp up at 50% tomorrow night, while Block E is expected to ramp up 50 MW on Friday Feb. 27. Further delays could impact the coal availability for Week 10.

- KMW 2 (DT & GT units - 320 MW): expected to come back on Tuesday 1 March, after an unplanned outage started on 10-12 Feb. Delays impact Week 10 fossil gas availability curve.

France

With week 9 recording temperatures 3–5 degrees above seasonal averages, the weekend is set to bring a further increase, with week 10 expected to average around +3 degrees above normal. This points to two consecutive weeks of milder weather across France. Combined with last week’s improvement in hydro reserves, this should ease significant pressure on the demand side. Only marginal adjustments in renewable generation are detected from Friday to Monday, as wind output remains above seasonal norms.

Nuclear availability declined by 1 GW last week. However, given the overall mild outlook, a further 4 GW reduction is planned by EDF for Week 10, with no significant changes recorded over the weekend.

A weekly average nuclear availability of 47 GW would mark the lowest level in the past 18 weeks, largely reflecting subdued residual demand, which is expected to remain below 45 GW and peak at 50–52 GW during evening hours.

To watch this week:

- Gravelines 1 (900 MW): from a 5-day 50% partial planned outage expected to terminate on 22 Feb, the plant has extended full ram-up operations to Wednesday 25 Feb., this weekend seeing an additional 1-day extension.

- Dampierre 4 (900 MW): 3-day planned 50% partial outage announced Sunday night expected to end on 25 Feb.

- Penly 1 (1.3 GW): 1-month 100 MW partial outage announced on Sunday 22 Feb.

Refuelling and long outages: several refuelling outages planned this weekend align with the broader nuclear availability drop, potentially tightening the supply stack.

- Bugey 5 (900 MW): 6-week refuelling planned outage starting Saturday 28 Feb.

- Cruas 2 (900 MW): 6-week refuelling planned outage starting Saturday 28 Feb.

- Tricastin 1 (915 MW): 6-week refueling planned outage starting Friday 27 Feb.

- St Alban 1 (1.34 GW): 3-month planned outage from 27 Feb. to 4 June will see the unit fully shutdown.

Netherlands

The Netherlands’ Monday vs Friday revision shows a 300 MW drop in GFS ENS wind output that is offset by an upward increase in temperatures (around 1.5 °C) as of Monday. Both demand and residual demand saw minimal revisions over the weekend, while solar output continues to correct upwards.

On the thermal side, the Amer 9 hard coal unit has extended its initial weekly outage into a month-long outage, with restart now expected on 6 March. The outage was prolonged by a further three days this week, directly impacting week 10 availability.

CWE Weekly Review - Week 8 2026

- CWE spot prices corrected materially, falling 20 - 30% w/w, as a strong increase in renewable generation significantly loosened regional fundamentals. France posted the largest move, with day-ahead prices declining 28% to 32 €/MWh.

- France recorded multiple zero and negative-price events, similar to Week 7, particularly during daytime hours on Monday, Saturday, and Sunday, which significantly weighed on the weekly average. This occurred despite a +1.5 GW increase in total demand, as elevated wind generation combined with strong daytime solar output created oversupply conditions and forced roughly 5 GW of wind curtailment.

- Across CWE, renewable output expanded by +16 GW, pushing residual demand lower by -13.5 GW w/w and displacing close to -10 GW of fossil generation. The renewable surge was the primary driver behind the weekly price adjustment.

- Germany accounted for the majority of the renewable increase, contributing approximately +9 GW, which reduced residual demand by -8.5 GW, even as temperatures fell by -2°C w/w. The increase in clean generation more than offset the weather-driven tightening effect.

- Thermal margins deteriorated significantly. Dark spread profitability hours fell below 20 % for the first time this year, while spark spreads showed higher resilience at 36 %. This marks a steep decline from 40% and 60% in Week 7.

- Unplanned outages remained limited on the French nuclear side. To note only Bugey 4 was the most significant event, losing 9.7 GWh over 12 hours. Germany marked only a 1-day major thermal outage on Monday 16 Feb. from the Kraftwerk Rostock plant.

Market Deep Dive

CWE spot prices corrected sharply in Week 8, falling 20 - 30% w/w across core markets. France led the move, with day-ahead prices declining to 32 €/MWh (-28% w/w), while Germany dropped to 92 €/MWh (-20% w/w). The correction was broad-based and structurally driven, reflecting a significant easing in residual demand across the region.

The primary driver was the sharp expansion in wind generation. Across CWE, renewables increased by +16 GW w/w, pushing residual demand down -13.5 GW w/w to 96 GW. This displaced nearly -10 GW of thermal generation, materially reducing fossil units’ role in price formation.

CWE wind increased by +13.8 GW w/w, with Germany alone contributing roughly +9 GW of the renewable expansion. This drove national residual demand down -8.5 GW w/w, despite a -2°C decline in temperatures, and reduced thermal generation across CWE by nearly -10 GW, with Germany accounting for roughly 50% of the fossil pullback.

France experienced repeated oversupply conditions, particularly during daytime hours. At the start of the week, elevated output from Hautes Falaises contributed to price compression, while strong generation from Banc de Guérande toward the weekend reinforced downward pressure. Despite a +1.5 GW increase in total demand, renewable output exceeded system needs during several intervals, pushing prices as low as -0.01 €/MWh and forcing roughly 5 GW of wind curtailment. These episodes materially dragged the weekly average lower.

Thermal generation stepped back significantly. Regionally, gas fell by nearly -7 GW, while coal declined by more than -3 GW, confirming broad fossil displacement. In Germany, reduced fossil dispatch led to weaker margins, with dark spread profitability falling to 17% and spark spreads to 36%, compared with 40% and 60% in Week 7. The strongest thermal profitability occurred mid-week on Wednesday, when temporary wind weakness allowed fossil units to regain marginal pricing power.

Cross-border dynamics reflected stronger price convergence. The FR–DE spread narrowed by 8 €/MWh w/w, as elevated renewable generation reduced structural divergence between markets and softened marginal cost differentials.

On the outage side, system disruptions were limited and secondary to renewable dynamics. France recorded 126 GWh of nuclear energy loss, with Bugey 4 the most notable event at 10 GWh over 12 hours. Germany recorded only 12.5 GWh of thermal outage losses. Given the nearly -5 GW reduction in thermal dispatch, outage impacts remained marginal relative to renewable-driven easing.

Overall, Week 8 was defined by a structural renewable reset. The -13.5 GW contraction in residual demand remains the clearest quantitative explanation for the broad spot price correction across CWE.

Power market data & analytics

A one-stop-shop for data, analytics, and insights, Kpler is trusted by physical and financial market players to empower their decisions with confidence and speed. Power Insight delivers unbiased, expert-driven intelligence.

See why the most successful traders and shipping experts use Kpler

.jpg)