Chinese economy struggles in April as oil imports precipitously decline

While Chinese goods exports surged in April, domestic household consumption weakened, and industrial production growth decelerated.

Summary

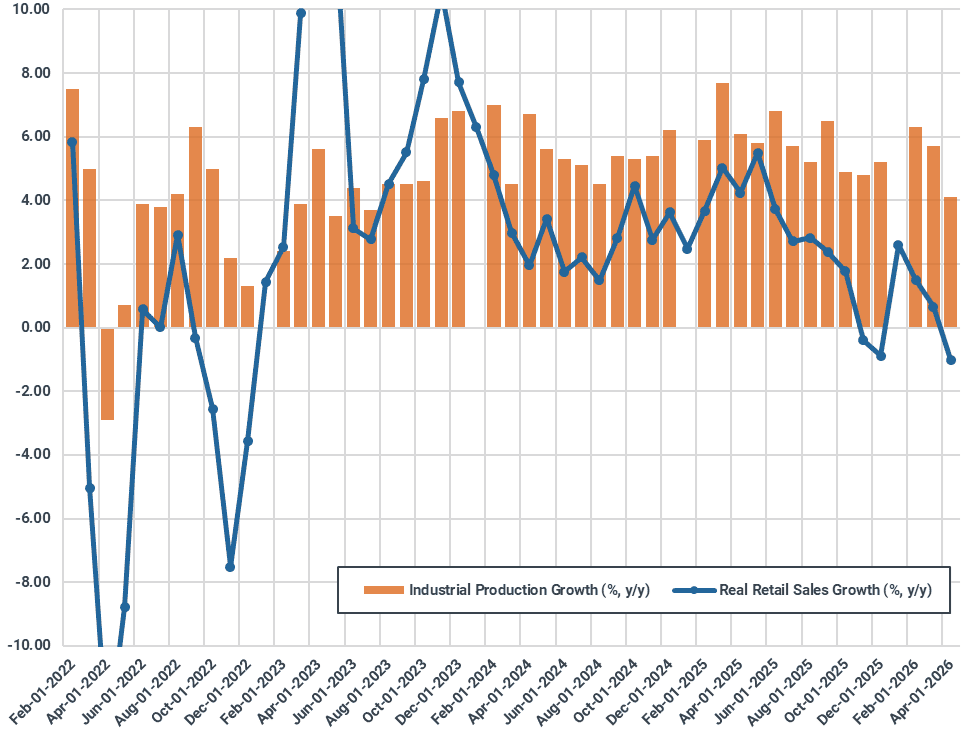

- Reliance on External Demand: Real retail sales fell 1% y/y in April, while industrial production held at +4.1% y/y, firmly keeping a persistent production – consumption gap in place. This dynamic keeps China highly reliant on external demand to absorb excess output. This dependence is unlikely to ease much this year and is a core reason China would prefer to see the Iran conflict end. Higher energy prices imply a weaker global economic environment.

- Narrowing Trade Surplus: Net exports fell to $85bn (-$11bn y/y) in April. However, the move was driven by higher semiconductor volumes and prices for AI infrastructure rather than a reflection of improving household demand. We expect this to persist and limit the pace of net export expansion, though the full-year goods surplus will still finish at a record high $1.2tn, roughly in line with levels from 2025. We also caution reading the compression as a shift towards consumption-led growth.

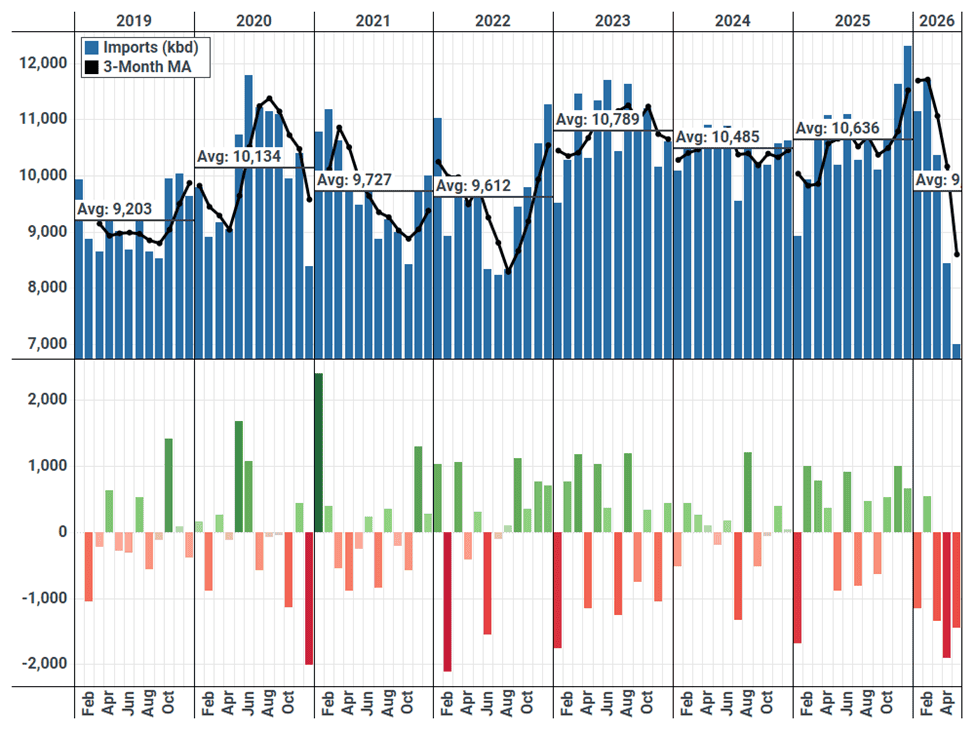

- Chinese Oil Imports Decline: An elevated dependence on crude imports is another driving factor behind why China would prefer to see an end to the Iran conflict and the Strait reopened. So far through May, Chinese seaborne crude/co imports have fallen 4.7 Mbd against pre-Iran levels. Transportation fuel exports have not recovered into May, currently holding at 126 kbd, down from 625 kbd pre-Iran.

Market Analysis

Last week (May 13), amid the Trump – Xi summit, we argued that China faced a nuanced position regarding the Iran war. On the one hand, China gains from watching US hard and soft power take a hit. Trump faces a bad decision set that involves either escalating or walking away, leaving Iran with control over the Strait of Hormuz. However, given an elevated reliance on external demand and a need for large amounts of imported oil, China would ultimately prefer to see the Iran conflict come to an end.

As the closure of the Strait of Hormuz approaches the three month mark, China’s economy is showing signs of strain. In April, retail sales growth, when adjusted for inflation, declined 1% y/y, falling from an already meagre +1.6% y/y growth rate in Q1. Over the final two months of 2025, similar real consumption declines were also prevalent. Broadly speaking, the Chinese consumer has struggled since the middle of last year, when consumption growth topped out at +5.5% y/y, nearly overtaking the pace of industrial production growth, a rare development. For now, the government has not shown much willingness to step up fiscal support beyond incremental measures that largely just pull forward demand.

Chinese Industrial Production and Real Retail Sales Growth (%, Y/Y Terms)

Source: NBS; Kpler calculations, Industrial production growth is reported for Jan/Feb, retail sales data is only reported for Jan/Feb but has been split equally and computed against headline inflation

Industrial production growth is also slowing, expanding by just +4.1% y/y in April, well off a Q1 average of 6%. Nonetheless, Chinese exports, when assessed in USD terms, rose nearly 14% y/y in April, continuing a pace of strong growth seen in Q1, when departures increased 14.5% y/y. Such large export gains reflect a large and persistent gap between the pace of industrial production and retail sales growth, which has steadily widened since the middle of 2025. This is a major reason why China needs the global economy to remain healthy. Without external demand, China will have a narrowing outlet for excess production at home.

Interestingly, net exports, which best reflect the gap between production and domestic absorption (consumption + investment), narrowed in April to $85bn, down $11bn y/y. However, much of this is being driven by higher chip imports (and prices) meant for AI infrastructure, rather than a reflection of improving Chinese household demand. This trend could very well persist through the duration of this year and could act to limit the pace of net export expansion in 2026. China’s goods trade surplus will likely finish in a range near $1.2tn, roughly the same level from 2025. We want to caution that this does not necessarily imply that the Chinese economy is rebalancing towards a consumption-led growth model.

In addition, China continues to rely heavily on infrastructure investment as an offset to weak household consumption, and property investment. Through the first four months of the year, infrastructure investment managed at a resilient +4.3% y/y, albeit spending growth likely decelerated a bit in April. Nonetheless, it is our belief that elevated infrastructure outlays will remain a core theme for the Chinese economy this year. Note that much of the infrastructure investment that is now taking place is un-economic, raising China’s debt burden without a positive payoff.

Monthly Chinese Seaborne Crude/Co Imports (kbd, top) and M/M Delta (kbd, bottom)

Source: Kpler

Finally, China remains highly exposed to the energy supply issues gripping the global economy, reflecting a second reason why China would prefer the Iran conflict come to an end. Chinese seaborne crude oil imports have declined precipitously since the war began. So far through May, seaborne crude arrivals are on pace to finish at 7 Mbd, down 1.4 Mbd against month earlier levels, and lower 4.7 Mbd against pre-Iran levels. We currently model Chinese refinery runs at 13.4 Mbd in May, down 2.3 Mbd from pre-Iran. China is helping to balance the global oil market by limiting imports.

Despite announcements that the Chinese government would allow for more clean product exports, there is little evidence that this is happening. Shipments of jet, diesel, and gasoline so far through the month of May have managed at just 126 kbd, down from 217 kbd in April, and 625 kbd pre-Iran. It seems unlikely that clean product exports will recover much until the Iran conflict finishes, and global oil supply availability recovers.

See why the most successful traders and shipping experts use Kpler

.jpg)