Urea's Gulf squeeze has eased, but the acreage hit is locked in

Urea-laden vessel traffic in the Middle East Gulf hit a record high during the Strait of Hormuz disruption, then unwound fast once the strait reopened. Prices have since eased down from four-year high but the spike landed at planting time. Wheat in Australia, corn in the US and other summer crops globally have suffered acreage reduction as a result.

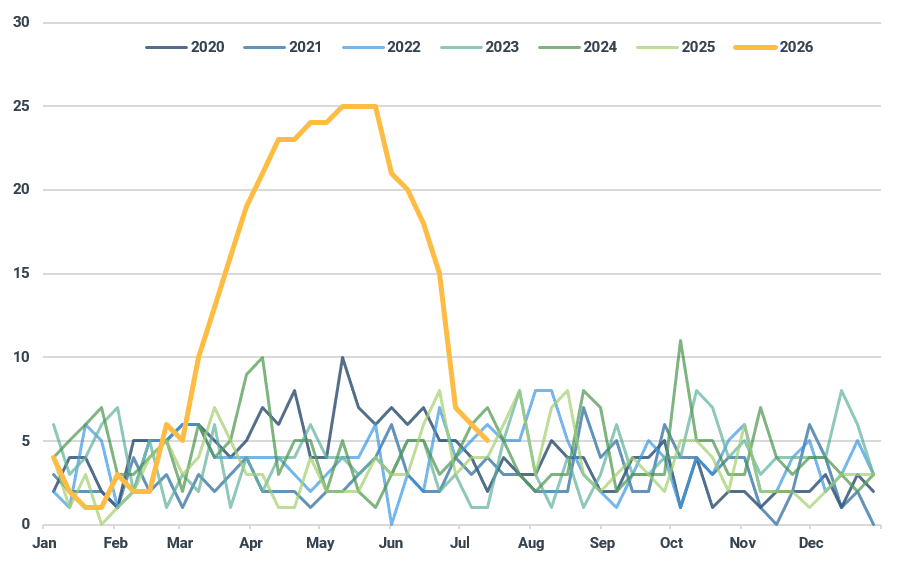

A record Gulf vessel backlog builds, then unwinds within weeks

Around 40% of global seaborne urea trade moves through the Strait of Hormuz, most of it produced in the Gulf states and Iran, where cheap gas underpins the region's energy-intensive urea output. When the Strait's disruption began in March 2026, cargoes kept loading but could not transit, and the number of urea-laden vessels waiting within the Middle East Gulf climbed from a typical 2-6 a week to a record high by mid-May, 4 to 5 times the usual level and a historical high for the region.

The backlog held near its peak for around 6 weeks before unwinding sharply once the strait reopened, in line with the wider fleet exodus from the Gulf as loaded cargoes finally moved.

Urea-laden vessel traffic in the Gulf hits a record 25 vessels before unwinding (vessel count)

Source: Kpler

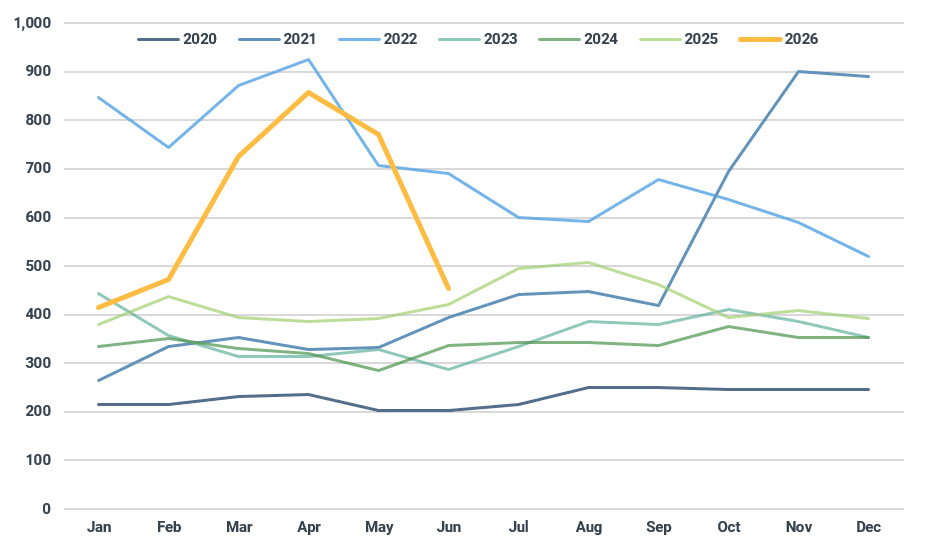

Urea prices spiked alongside the backlog, but there were no new curbs from other exporters

Urea prices rose sharply over the same period, climbing from a subdued start in January 2026 to a level not seen since the 2022 energy crisis by April, before easing back in May.

Unlike sulphur, where several exporters layered on new restrictions, other major nitrogen suppliers left urea trade largely untouched. Russia suspended ammonium nitrate exports for a month, then returned to a quota system from 22 April 2026. Global urea supply outside the Gulf did not tighten further.

Urea prices spike before easing ($/t)

Source: World Bank

Russian and Egyptian urea volumes have redirected to India, and away from Brazil

Trade flows shifted alongside the price and vessel moves. Russian urea volumes to India rose to around 870 kt in the first half of 2026, up roughly 90% y/y, while volumes to Brazil fell by around 30% y/y. Egyptian volumes have shifted further still, from a negligible presence in India in the first half of 2025 to over 600 kt in the first half of 2026, including a single 343 kt month in May.

The shift reflects price action and India's rapid move to secure urea volumes. Brazil has more breathing room since its imports peak in the fourth quarter, for application on to safrinha corn area during planting in January and February.

Higher urea costs are reshaping planting decisions

In Argentina and Australia, farmers were weighing winter planting decisions through the disruption. Higher urea prices discouraged wheat planting, since wheat is more nitrogen-intensive than barley, pulses, or canola. Wheat area in Australia is down 12% this year, according to official estimates. In Argentina, growers have instead pushed area towards spring planting, fallowing land until then.

In the Northern Hemisphere, growers are now deciding which spring crops to plant. Arguably, the US would have seen higher corn acres had urea prices been lower. China, India, Europe, Ukraine, and Russia will all see acreage shifts of varying degrees, with rice and corn the most affected crops. High grain stocks across Europe, India, Australia, and Argentina should cushion the effect on production, though El Nino-linked dryness could compound the yield hit if it materialises. Higher urea prices will not cut grain supply immediately, but they have caused acreage shifts. Persistent high prices will limit yields for cereal crops harvested later in 2026 and into 2027.

See why the most successful traders and shipping experts use Kpler

.jpg)