Russia's diesel export ban adds fresh fuel to rising prices

Russia's ban on diesel exports will not drive a large balance shift given already-curtailed volumes, but it adds fresh upward momentum for prices alongside the collapse of the US-Iran ceasefire. Its main buyers will either draw from inventories if the ban is a short pause, or turn to the US.

Key takeaways

- Bullish, diesel: Russia's export ban will not drive a large balance shift given supply was already massively curtailed, but it adds fresh impetus for prices to climb, along with the re-escalations along the Strait of Hormuz.

- Bullish, USGC: Brazil is likely to pull more diesel from the US, repeating the substitution pattern seen during the 2023 ban.

- Neutral, Med: Turkey's import pattern is unlikely to shift; expect a repeat of 2023, when it drew on inventories rather than replacing Russian volumes.

Russia introduced an export ban on diesel on July 8 in response to Ukraine's attacks on its refineries, running until July 31. Ullage constraints and the cost of forgoing export revenue mean this ban is likely to be short-lived, despite Deputy Prime Minister Alexander Novak's comments in late June that such a ban would run for a matter of months. There is precedent for this: Russia's last diesel export ban in September 2023 was partially lifted after only two weeks.

The ban also lands just as the US-Iran ceasefire has collapsed, with Washington declaring the framework deal over after Iran struck tankers transiting the Strait of Hormuz. The reimposition of oil sanctions and renewed strikes reintroduce a supply-risk premium that reinforces the bullish case independent of the diesel ban itself.

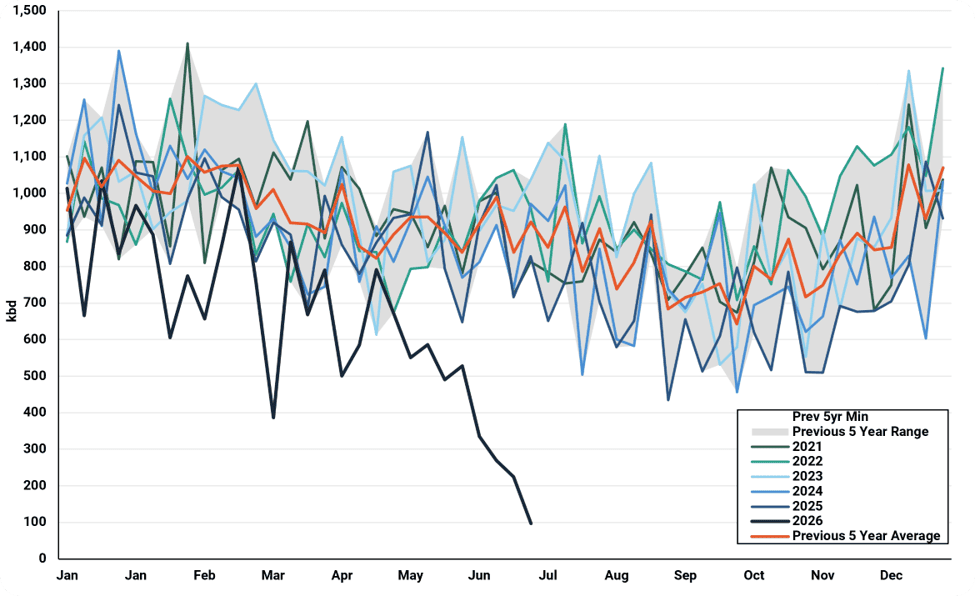

Ukraine's attacks have already constricted Russian supply, with diesel exports averaging 214 kbd in the week beginning June 29, down 492 kbd y/y and down 615 kbd from the five-year average for the week. The decline reflects reduced complex primary capacity utilization following attacks on refineries including Moscow and TANECO, which has cut diesel production while shifting middle distillate output toward higher-sulfur gasoil (HSGO) rather than ULSD. Russia's refining sector has managed comparable disruptions before, and outages have tended to be sporadic rather than sustained, supporting the case that this ban is a short-term measure rather than a structural shift.

The total shut-in will weigh on leading importers Turkey and Brazil. Turkey brought in 222 kbd from Russia in June, and Brazil brought in 135 kbd. Turkey's diesel imports from Russia declined by 150 kbd m/m in October 2023 when Russia last banned its diesel exports. It did not replace Russia's supply and instead drew on inventories while lowering consumption.

Brazil saw imports from Russia fall by 66 kbd m/m in October 2023 during the last ban, with deliveries from the US rising by 71 kbd m/m. That shift is likely to recur, with the US maintaining maximum refinery runs over 17mn bbl/d against seasonally weak domestic diesel demand.

Russian weekly gasoil/diesel exports (kbd)

Source: Kpler

Market insights you can trust

Kpler delivers unbiased, expert-driven intelligence that helps you stay ahead of supply, demand, and market shifts.

Trade smarter. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler

.jpg)