Ukraine's drone campaign pushes Russian refinery runs to 21-year lows

Russian refinery crude runs have fallen to around 3.80 mbd in July-to-date, the lowest level in well over two decades, as sustained Ukrainian drone attacks continue to disrupt the country's downstream sector, with refinery downtime and attacked capacity standing at around 4.3 mbd in July-to-date. Looking ahead, Kpler expects Russian refinery runs to remain largely subdued through Q3, with only a limited recovery as continued drone strikes and ongoing repairs constrain refinery operations.

Market & Trading Calls

- Bearish for Russian refinery runs and product exports: Continued drone strikes will keep refinery runs subdued, delaying restarts and limiting fuel exports.

- Bullish crude exports: Reduced refining leaves crude available for export.

- Bullish middle distillate cracks: Lower Russian diesel exports continue to tighten Atlantic Basin balances.

Ukraine's drone campaign against Russia's downstream sector has become increasingly extensive, degrading both refining capacity and operational capability. Since August 2025, at least 25 Russian refineries have been affected by drone strikes, with attacks impacting crude distillation units, secondary processing units—including FCCs, hydrocrackers, catalytic reformers and hydrotreaters—as well as storage tanks, pipelines and other critical logistics infrastructure. Damage to these assets often requires broader inspections and integrity checks before operations can resume, extending outages and delaying restarts. As a result, refinery disruptions have increasingly constrained both crude processing and on-spec transportation fuel production.

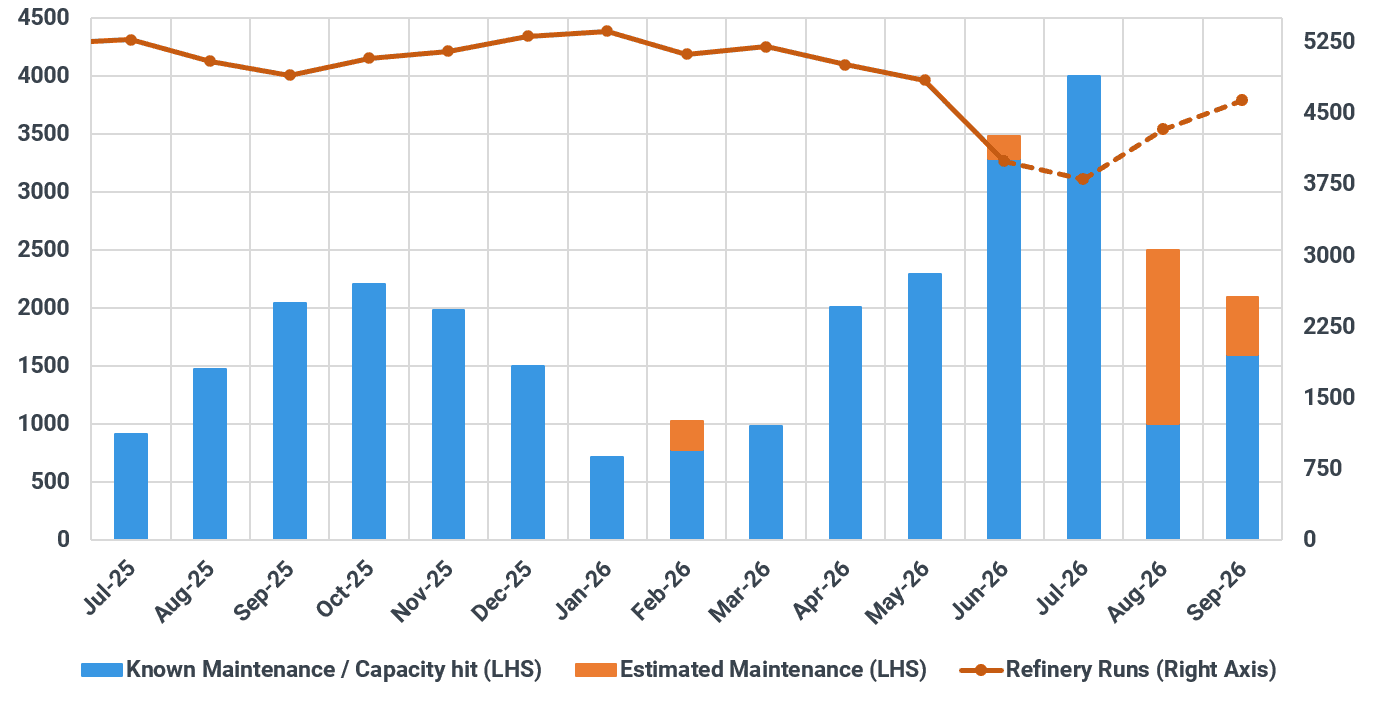

Russian refinery operations (kbd)

Source: Kpler and IIR

The cumulative impact has been a sharp increase in refinery outages. As of mid-July, refinery downtime and attacked capacity stood at around 4.3 mbd, representing roughly 58% of Russia's refining capacity, with an estimated 1.5–2.0 mbd of processing capacity effectively offline. Higher utilisation at unaffected refineries has only partly offset these losses, leaving Russian crude runs at around 3.8 mbd in July-to-date, the lowest level in more than two decades. Kpler expects runs to recover modestly to around 4.3 mbd in August as maintenance eases, although continued drone strikes leave risks firmly skewed to the downside.

Russian Refinery Runs Since 2006 (kbd)

Source: Kpler

The implications extend well beyond refinery runs. Russia is transitioning from one of the world's largest exporters of transportation fuels to a potential importer of selected products. Rather than supplying the global market, persistent refinery disruptions are increasingly creating incremental demand, providing structural support to global refining margins and product (Gasoline and Mid-distillates) balances.

Transportation fuels bear the brunt

The sharpest impact is being felt in transportation fuels, tightening domestic balances and reducing export availability. This is now evident in trade flows, with Russian refined product exports averaging just 1.2 mbd so far in July, down from 1.6 mbd in June, 1.85 mbd in May and 2.3 mbd (July) a year ago. In contrast, crude exports rose to 4.4 mbd in June and are averaging around 4.0 mbd so far in July, as unprocessed crude is increasingly redirected to export markets.

- Gasoline: Production is estimated to have fallen by 175 kbd between March and July, prompting Russia to maintain export restrictions, ease fuel quality standards, encourage naphtha blending and source additional volumes from Belarus and potentially the seaborne market.

- Diesel/Jet: Middle-distillate production is estimated to have declined by around 350 kbd over the same period. While diesel balances remain less tight than gasoline, lower diesel and jet yields have reduced export availability and lifted domestic wholesale prices. The temporary suspension of ULSD exports through July underscores that supply pressures are now extending beyond gasoline.

Product Supply Loss (kbd)

Source: Kpler

Recovery outlook remains subdued

Looking ahead, Kpler expects Russian refinery runs to remain subdued through Q3. While planned maintenance is easing, any recovery is likely to be limited, with runs rising only from around 3.8 mbd in July to 4.3 mbd in August and 4.6 mbd in September—still well below historical operating levels. Residual infrastructure damage and continued Ukrainian drone strikes will continue to constrain throughput. Recent attacks on Moscow, Volgograd, Omsk, Syzran and Saratov reinforce this view, as repairs to critical processing units and supporting infrastructure are expected to take months rather than weeks. A clear pattern has also emerged: refineries are repeatedly struck before repairs can be completed, extending outages and delaying restarts. As a result, Kpler does not expect a meaningful recovery in refinery runs before Q4. Unless attacks on energy infrastructure ease materially as part of a broader ceasefire or truce, downside risks to the outlook remain elevated.

See why the most successful traders and shipping experts use Kpler