Why Iran’s oil production will rebound faster than its neighbours

Iran's oil production is poised to rebound faster than neighbouring producers following the US-Iran MoU. Unlike regional producers, Iran only needs access to buyers with the blockade lifted and sanctions waived. Ships are not a bottleneck and wells are not damaged. In fact, production may come back stronger than pre-war levels in the short-term.

Market & Trading Calls

- Bearish medium sour crude differentials: Iranian crude exports are likely to recover faster than other Gulf producers, increasing availability of medium sour barrels into China, and other markets depending on the waiver.

- Bullish Iranian crude diffs: Sanctions waivers covering newly loaded cargoes will accelerate demand beyond China if banking transactions are made possible.

- Bearish Dubai: Depending on the scope of the sanctions waivers, new buyers could emerge, reducing prompt demand for competing Middle Eastern medium sour crude.

- Bearish Russian medium sour grades diffs: Depending on the scope of the sanctions waivers, greater Iranian availability could partly displace Indian demand, redirecting buying interest towards ESPO and Urals.

- Watch banking sanctions closely: Export waivers alone are unlikely to materially expand Iran's customer base without parallel easing of payment restrictions.

Key Takeaways

- Iran's oil production is poised to rebound faster than neighbouring producers following the US-Iran memorandum of understanding (MoU).

- The effective lifting of the maritime blockade is sufficient to restart exports and support a rapid recovery in production and loadings.

- Unlike other Persian Gulf exporters, Iran does not depend on a full restoration of tanker confidence or regional security conditions to resume shipments.

- Limited upstream damage and extensive experience managing well shut-ins should allow Iranian production to recover above pre-war levels quickly.

- The ultimate impact on global crude markets will depend on the scope of any US sanctions waivers, particularly those covering financial transactions.

Iran only needs the blockade to be lifted to boost production and exports

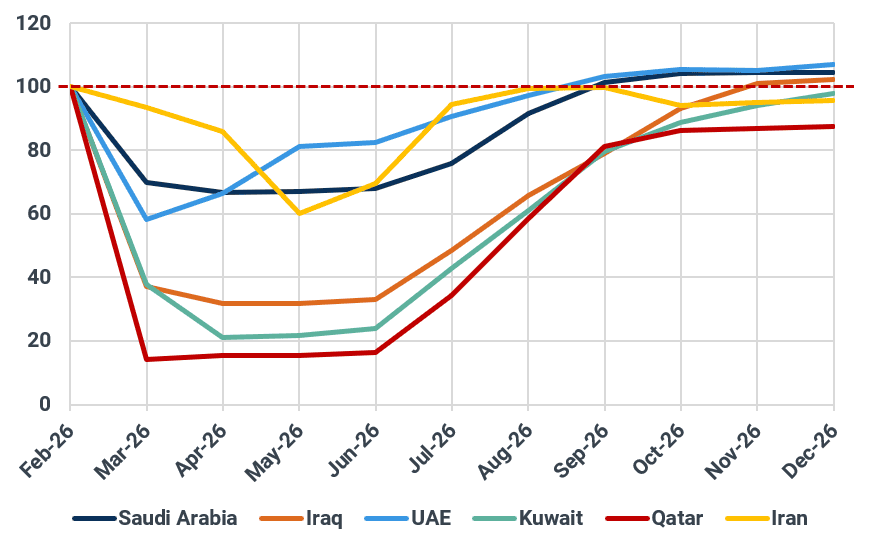

Iran's oil production is set to recover faster than the rest of the Gulf once the Strait of Hormuz reopens. While neighbouring producers remain dependent on the return of tanker traffic and shipping confidence, Iran only needs access to export routes to restore flows. We estimate Iranian crude production could rise to 3.5 mbd by August, exceeding the 3.3–3.4 mbd levels observed before the conflict.

Recent vessel movements suggest the maritime blockade imposed on Iranian exports has already been relaxed. Since reports emerged that Washington was considering early concessions ahead of the formal signing of a US-Iran MoU, several laden tankers have departed the Gulf of Oman and entered the Arabian Sea, crossing what had previously been the effective blockade line.

The removal of the blockade alone is sufficient to trigger a recovery in Iranian production. Unlike other Gulf producers, Iran is not waiting for security guarantees around the Strait of Hormuz. The threat to shipping originated from Iran itself, giving Tehran greater confidence in the safety of its own export routes. Moreover, the National Iranian Oil Company (NIOC) has long relied on dark fleet operations and therefore remains less dependent on conventional tanker markets than its regional competitors.

Oil production (February 2026 = 100)

Source: Kpler. This assumes the MoU converts into a comprehensive deal or that the negotiations are extended into 2027

Iran already has enough ships waiting to load

Operationally, Iran is also better positioned to resume exports quickly. We currently identify approximately 35 mb of available ballast capacity across 21 tankers that have historically transported Iranian crude and refined products. These vessels are already present in the Persian Gulf or the Gulf of Oman, reducing the logistical bottlenecks facing other exporters. While NIOC is unlikely to immediately maximise loadings, exports should begin to accelerate within days as ballast vessels return to Kharg Island.

Upstream damage is limited and NIOC has extensive experience in managing output

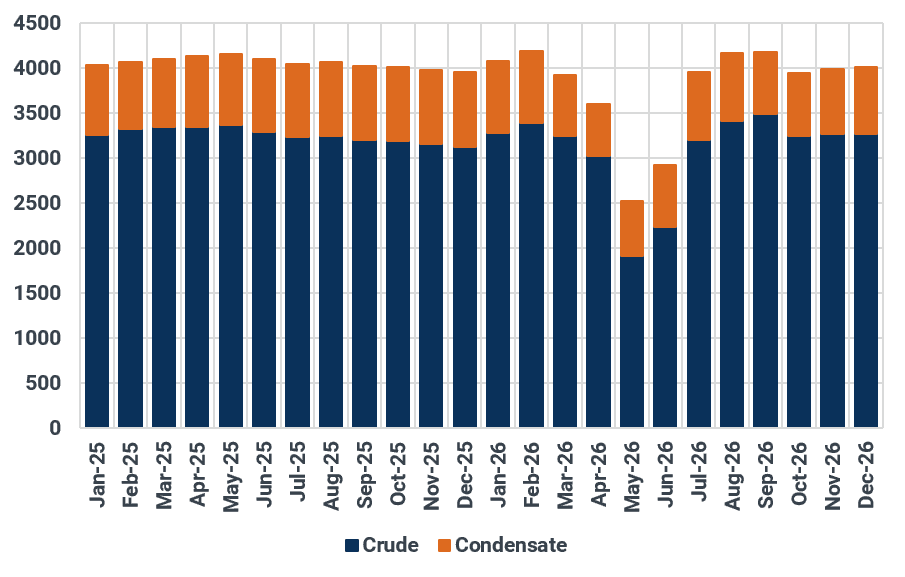

Upstream constraints are equally limited. Iranian crude production is estimated to have fallen by as much as 1.3 mbd during the blockade due to the inability to export rather than any damage to producing assets. Most Iranian reservoirs are carbonate formations with relatively low asphaltene content, reducing the risk of formation damage during temporary shut-ins. Given that wells have remained offline for less than two months, pressure build-up may even support stronger initial production rates as output is restored.

Iranian oil production, kbd

Source: Kpler

Sanctions relief could trigger interest from non-Chinese buyers

Beyond unleashing 72 mbbls of oil that was stranded in the blockade area up until Monday – roughly equivalent to ~$5.6bn at current prices – the next catalyst is sanctions relief. The MoU mentions Washington will issue waivers covering Iranian oil and petrochemical exports during the negotiation period. At minimum, these waivers could apply to cargoes loaded before the MoU enters force. A more significant outcome would be the inclusion of newly loaded cargoes, allowing Iran to market additional barrels without immediate sanctions risk.

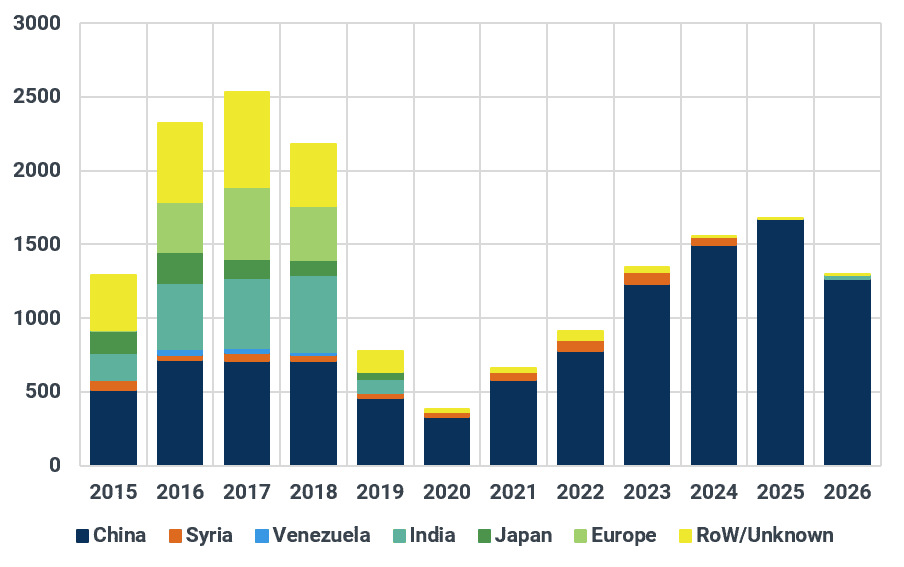

The key question is whether banking restrictions are eased alongside export waivers. The March waiver generated limited participation from non-Chinese buyers, with only three cargoes purchased by Indian refiners. Most other buyers remained on the sidelines due to payment restrictions and reputational concerns associated with trading Iranian crude during an active conflict.

Should financial sanctions also be relaxed, the pool of potential buyers would expand materially. Beyond India, refiners in Japan, South Korea, and the Mediterranean could re-enter the market. In that scenario, Iranian crude discounts would decrease and medium sour crude differentials would come under pressure. India’s attitude will also drive the next direction for Russian oil diffs (pressured down if India buys more from Iran). However, a floor would be found for grades such as ESPO and Urals as Chinese refiners would substitute away from discounted Iranian barrels.

Iran oil exports by destination, kbd

Source: Kpler

The broader conclusion is clear: Iran's recovery is constrained by market access rather than upstream capacity or tanker availability. With that constraint now being removed, Iranian production and exports are likely to rebound faster than those of its regional peers.

See why the most successful traders and shipping experts use Kpler