Markets in Motion: Where can Europe secure jet fuel to replace the Mideast Gulf?

Flashpoint: Markets in Motion

Europe has few straightforward options to replace lost jet fuel flows from the Middle East following disruption in the Strait of Hormuz. With Asian markets pulling cargoes eastward and export restrictions tightening supply, attention is shifting to the Atlantic Basin – particularly the US Gulf Coast and West Africa – though available volumes are unlikely to fully offset the shortfall.

Key takeaways

- Eastern barrels are increasingly unavailable as strong Asian pricing and export restrictions in China and potentially South Korea divert cargoes away from Europe.

- Indian supply remains a potential relief valve but EU sanctions exposure linked to Russian crude runs at Jamnagar continues to deter buyers.

- The Atlantic Basin – primarily the US Gulf Coast and West Africa – is the most realistic replacement source, though logistical constraints and limited spare export capacity mean volumes will fall short of replacing Middle Eastern supply.

The effective closure of the Strait of Hormuz cuts off nearly 21% of total global seaborne jet supply and reduces European imports by almost 300kbd, 247kbd of which would typically go to North West Europe (NWE). Replacing these volumes will be extremely challenging not least because the typical backup for supply, countries such as South Korea and China are instituting export limitations in order to protect their own domestic markets as over 50% of crude that flows past the Strait of Hormuz goes to East Asia. This is leading to wild swings in the Singapore market and causing vessels already loaded to divert away from Europe in order to capture value.

Cargoes from India, and the Jamnagar refinery specifically, would typically be crucial in times of supply tightness but this has been complicated by a number of factors already this year. EU sanctions under Article 3ma – prohibiting the import of oil products derived from Russian crude - has meant that buyers in the NWE jet fuel market have stayed away from handling these cargoes due to perceived sanctions exposure as Jamnagar has kept buying Urals but claiming to only run it in the Domestic Tarif Area (DTA) section of its refinery which does not export.

India receiving a waiver from the US to keep buying Russian crude, reduces the possibility of an export ban, but complicates exports even further if it is run in the Special Economic Zone (SEZ) section of the refinery which exports oil products. A relaxing of the EU rules, or specific exemptions, would enable this route to meaningful reduce the supply pressure in Europe and the longer the conflict goes on the more there will be calls for changes or clarifications to these rules.

Elsewhere in the MEG, only Petrorabigh and the Samref refineries in the Red Sea export jet fuel production in a region is heavily skewed towards diesel production, with jet fuel only making up only 6.4% of middle distillate exports in 2025. The Duqm and Sohar refineries in Oman are still operating but potentially at lower rates and its port has been attacked already in the conflict, but total jet exports were only 50kbd in 2025 including from third-party storage.

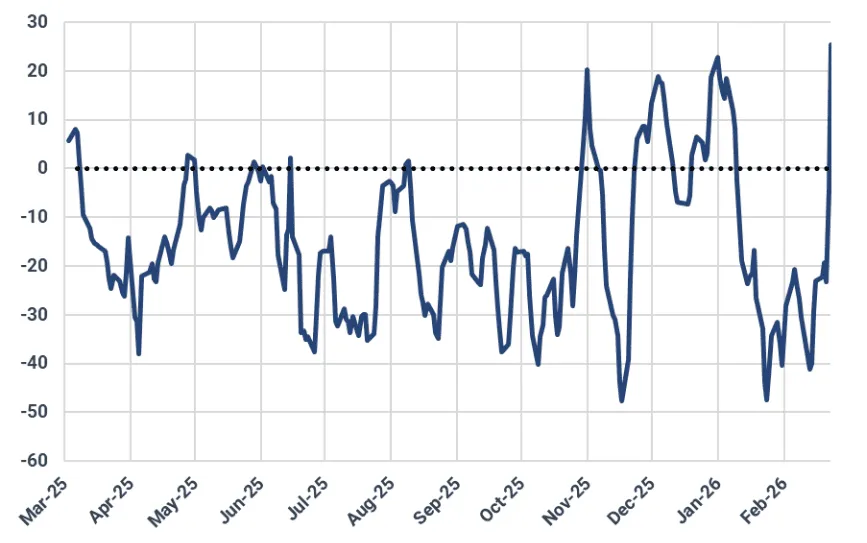

With supply from East pricing extremely strongly and exporting countries at risk of turning off the tap, the Atlantic Basin presents the best options to for resupply, but the question here is capacity. The arbitrage from the US Gulf Coast to NWE is open on paper, but overall exports rarely exceed 1 Mt in a month although in January exports hit an all-time high of 307kbd. The constraints for potential NWE buyers here are demand from Latin America, especially termed volume, slight differences in specification and infrastructural limitations. The US Atlantic Coast is largely supplied from within the US, with some flow from Canada, and hence the reaction in the US has been significantly weaker. We anticipate more exports to come in March from the USGC. helping to offset the lost cargoes from the AG.

USGC - UKC Jet arb M1 delivered 3DMA ($/t)

Source: Kpler using Argus Media prices

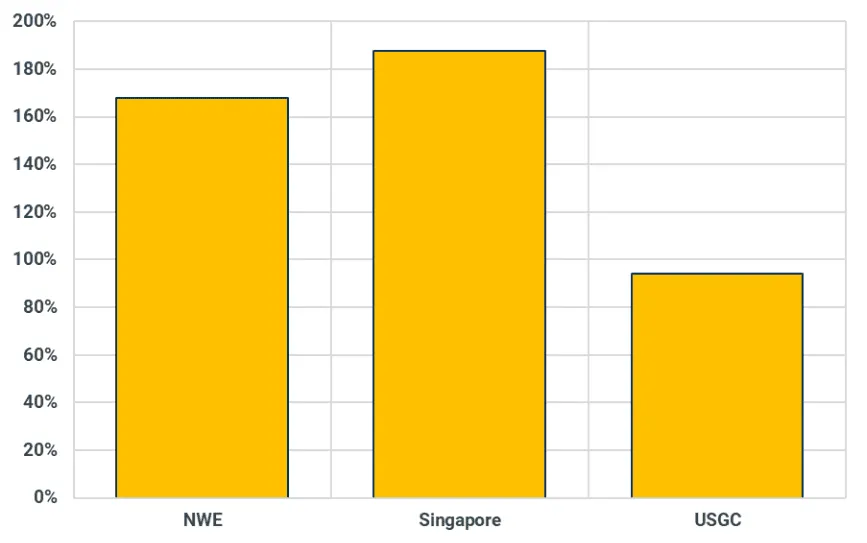

Regional benchmark jet fuel cracks, 27/02 versus 06/03 (% increase)

Source: Argus Media Prices

The USGC will not fully offset the missing the volume but with West Africa effectively a net long region in 2024 thanks to the Dangote refinery there is another supply point that can be tapped. Dangote exported around 89kbd of jet fuel in 2025. This structural length means that even if a policy of first supplying the domestic Nigerian market were enacted, exports would still materialize, especially as the refinery returns from maintenance.

Greater production within NWE will be hampered by refinery commitments to diesel, including term tender obligations, and the fact that the regrade – the spread between gasoil and jet – has already been strong for much of this year, limiting how much incremental jet fuel can be pushed out. Crude import supply will also be a concern. Even if refiners are able to increase jet output, defined locations of demand, specialist logistics and tank infrastructure mean it is no simple endeavor to move these volumes to where they are needed.

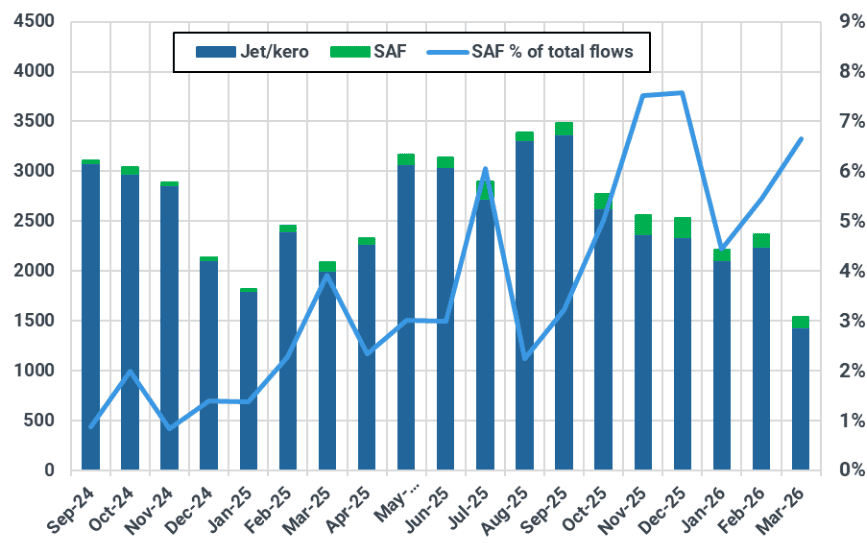

Sustainable aviation fuel (SAF), while growing in terms of importance with mandates of 2% in effect in the EU and the UK, still only makes up a small proportion of total flows (around 6%). Cargoes are mostly coming from Asia, where a lack of mandates generally leaves them surplus to requirements. While loadings may well continue or even increase to NWE, the small-scale of the flow, and the expense of SAF, will mean that its impact will still be minimal on overall balances.

EU-27+UK jet/kero and SAF total imports (kt, LHS) and SAF % of imports (%, RHS)

Source: Kpler

As a result, even with incremental barrels from the US and West Africa, Europe is unlikely to fully replace lost Middle Eastern supply in the near term, leaving the market reliant on higher prices and longer trade routes to rebalance flows.

Market insights you can actually trust

Kpler delivers unbiased, expert-driven intelligence that helps you to track critical crude oil market developments for your own analysis. Our precise forecasting empowers smarter trading and risk management decisions. In times of conflict and geopolitical uncertainty, our real-time data keeps you ahead of supply disruptions and price volatility.

Unbiased. Data-driven. Essential. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler