Despite a 60-day sanctions waiver, Iranian oil will mainly flow to China

Following the signing of the US–Iran deal on June 18th, OFAC announced on Sunday that Iranian oil sales would be permitted until 21 August, aligned with the MoU timeline.

Market & Trading Implications:

- China will remain the primary buyer of Iranian crude, though the upside in Chinese buying will depend on pricing and refiners' outlook for crude demand.

- Non-Chinese buyers are unlikely to take Iranian crude in meaningful volumes, as most refiners have already fulfilled their procurement requirements for August-arrival cargoes, while the 60-day window may prove too short to complete internal compliance reviews and regulatory procedures.

- Should the waiver be extended beyond 60 days, we would expect demand to emerge from refiners in India, Japan, South Korea, and the Mediterranean.

- In a fully unsanctioned Iranian oil scenario, we estimate a $7–10/bbl reduction to our current NSD price forecast, implying a $70–80/bbl range over the next 12 months.

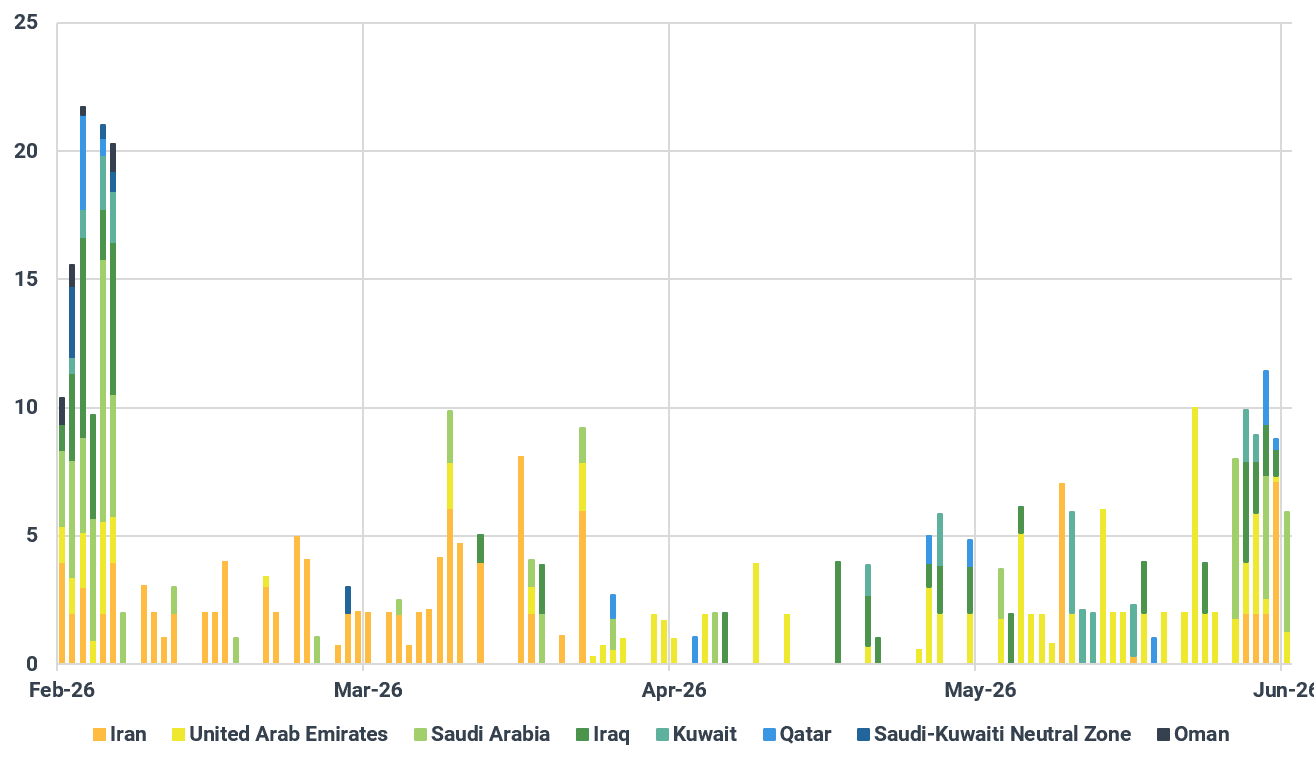

Iranian crude and condensate exports trended at roughly 1.7 Mbd prior to the war and fell to near zero in May and the first half of June following the US naval blockade imposed in mid-April. Since the blockade has been lifted, at least one Iranian crude-laden tanker has transited the Strait of Hormuz each day between 18 - 22 June.

Strait of Hormuz crude transits, Mbbls

Source: Kpler

Following the announced US–Iran Memorandum of Understanding (MoU), OFAC's General License now permits sales of Iranian-origin crude oil, petrochemical products, and petroleum products for a two-month window.

Iranian oil supply set for a sharp recovery

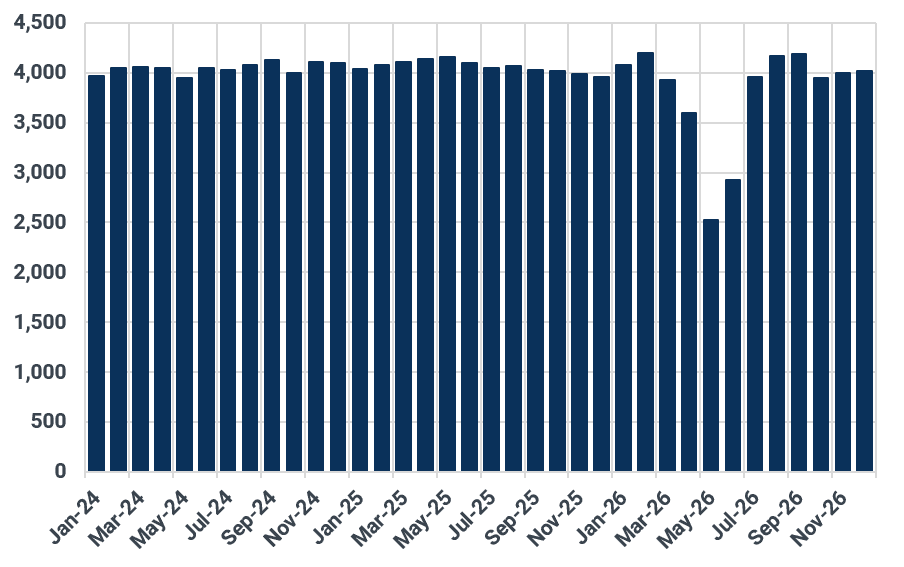

On the crude oil side, we expect the combination of blockade removal and sanctions relief to drive a steep recovery in Iranian production. Supply is estimated to have fallen by as much as 1.3 Mbd during the blockade, a consequence of the inability to export rather than damage to producing assets (condensate production at South Pars largely back by now). In this new environment, we could see a swift rebound in crude and condensate output: from 2.9 Mbd in June to 4.0 Mbd in July and 4.2 Mbd by August. Should waivers be extended beyond August, supply could be pushed closer to 4.4–4.5 Mbd, with Iranian crude exports rising from the pre-war levels of 1.7 Mbd to around 2.0 Mbd, considering historical records and available capacity.

Iranian crude and condensate supply forecast, kbd

Source: Kpler

Beyond ramping up production, Iran will prioritize drawing down oil inventories and maximizing exports — particularly within the window before the US implements new restrictions on August 21st. Even where buyers cannot be found immediately, Iran could move these cargoes out of the Gulf and store the oil offshore in Asia as a hedge against a renewed naval blockade choking off exports.

China remains the primary buyer

We do not expect a broad set of new buyers to emerge within this timeframe. Western buyers, both US and European ones, would face lengthy regulatory procedures covering compliance checks, credit lines, due diligence, and banking infrastructure, which would almost certainly not be completed within the 60-day window. When accounting for transit times from Iran of approximately 40–45 days alongside associated operational lead times, the full supply chain loop is unlikely to close before the waiver expires.

Market insights you can trust

Kpler delivers unbiased, expert-driven intelligence that helps you stay ahead of supply, demand, and market shifts.

Trade smarter. Request access to Kpler today.

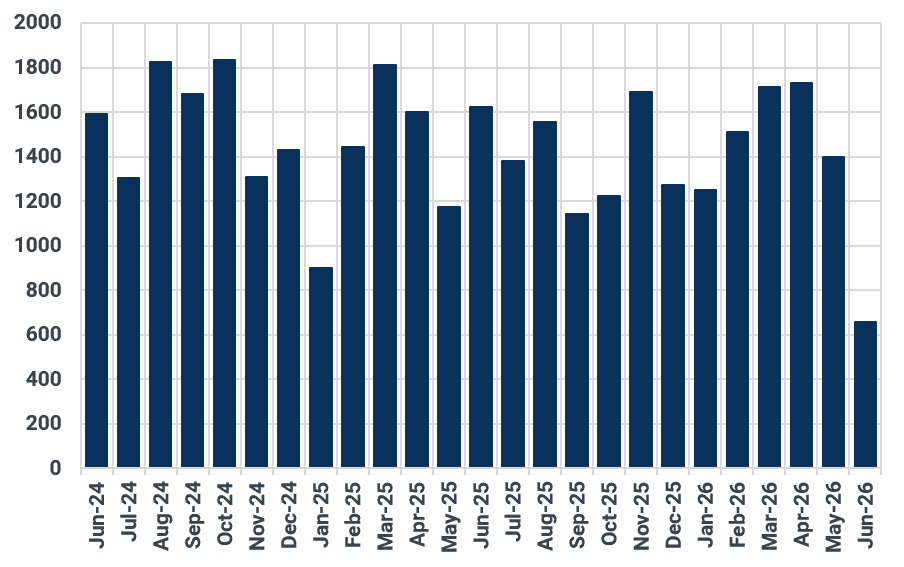

Chinese imports of Iranian crude, kbd

Source: Kpler

While China should remain the primary destination, principally independent refiners, and potentially state-owned enterprises if prices are sufficiently attractive, we do not expect the sanctions waiver to immediately trigger a surge in Chinese buying. Iranian sellers are mulling raising prices following the sanctions waiver, narrowing the differential to compliant barrels and reducing their competitiveness given the complexity of procurement. At the same time, subdued crude demand is expected to persist in China, capping overall appetite for feedstocks. We estimate Chinese crude demand fell by nearly 3 Mbd between February and June, with only a modest recovery expected — from 12.6 Mbd in June to 13.6 Mbd in August.

India to favor Russian and Middle Eastern crude over Iranian barrels

In what remains a highly uncertain and fluid environment, we do not expect the waiver to prompt India to purchase meaningful volumes of Iranian crude. This is consistent with India's behavior during the last temporary US waiver on Iranian oil, when Indian refiners bought only two cargoes and did not engage in incremental purchasing due to a range of operational and commercial constraints. With Indian refiners finalizing procurement for late-August and September, they are relying on Russian and Middle Eastern barrels (Saudi Arabia, UAE) as well as some Venezuelan volumes as things stand.

The US–Iran interim deal allows for negotiations to extend beyond the initial 60-day period, which could in turn lead to a further extension of the sanctions waivers. In that case, India would likely move more aggressively to fill any gap, given that its refineries were largely configured to process Iranian crude. The combination of shorter sailing distances and elevated freight rates makes Iranian barrels structurally more attractive than longer-haul alternatives. Beyond economics, there is a political dimension: stepping up Iranian imports would allow India to demonstrate — again — that it is distancing itself from sanctioned Russian oil in favour of non-sanctioned Middle Eastern and Iranian supply.

An extended waiver could bring new buyers into the market

Should Iranian oil remain unsanctioned after these two months, we would expect increased interest from non-Chinese buyers. India would likely be the first to re-engage, followed by refiners in Japan, South Korea, and the Mediterranean. Iranian crude sitting in floating storage will likely prove attractive to Asian buyers once the 60-day waiver lapses, and should weigh on prompt spreads — particularly the M1/M2 Brent and Dubai structures. At the same time, Iranian crude would command higher prices and medium sour crude differentials more broadly would come under pressure.

Market insights you can trust

Kpler delivers unbiased, expert-driven intelligence that helps you stay ahead of supply, demand, and market shifts.

Trade smarter. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler