Key agricultural commodities and aluminium fall as the US-Iran conflict risks a dangerous new phase

The iron ore market remains caught between resilient supply growth and subdued demand, keeping prices under pressure. Thermal coal demand is benefiting from summer consumption in the Northern Hemisphere. Ahead of the release of the June WASDE report, the development of the US corn and soybean crops remains broadly favourable. Aluminium prices eased on macroeconomic concerns, while alumina rallied on concerns about supply disruptions in China and Guinea. Freight markets are rebalancing, with Capesize rates falling sharply as Pacific vessel supply rises while Panamax, Supramax and Handysize segments remain comparatively resilient.

Iron Ore & Steel: Strong supply and weak steel fundamentals keep iron ore prices under pressure

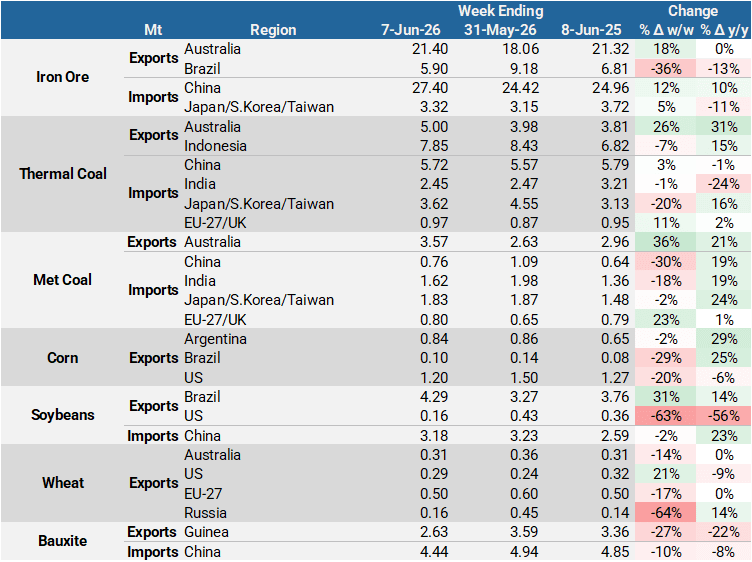

- Global seaborne iron ore exports totalled 33Mt in the week ending 7 June, down 5% y/y but still above the five-year average of 32.60Mt. The market continued to be supported by strong Australian shipments, which reached the second-highest level in nearly two years at 21.40Mt, as some miners expedited loadings in the final weeks of the quarter for reporting purposes.

- BHP’s exports surged to 6.93Mt, the highest level in a year. In addition to the usual fiscal year-end push, the increase may also reflect efforts to front-load shipments ahead of a potential port workers’ strike later this month. BHP has warned that the industrial action could cost more than $120 million per day, implying potential shipment losses of over 1Mt per day.

- In the Middle East, while there has still been no iron ore entering the Gulf since the outbreak of the US/Israel-Iran war, more signs of a gradual recovery in iron ore trade are emerging. Vale’s Sohar facilities received their first cargo since early March last week, totalling 0.17Mt, with a further 0.20Mt expected this week. Anglo American’s Minas-Rio operations in Brazil have also shipped to Sohar since the start of May. Some of this may have been ore previously intended for Bahrain.

- On the demand side, Chinese seaborne iron ore imports rose to a four-month high of 27.50Mt, supported by improving port throughput as congestion eased from May peaks. However, steel output remains subdued, with the latest data showing that daily production by CISA member mills declined 4.06% y/y to 2.01Mt in the last ten days of May. As a result, iron ore inventories at Chinese ports resumed w/w growth last week after several weeks of gradual destocking.

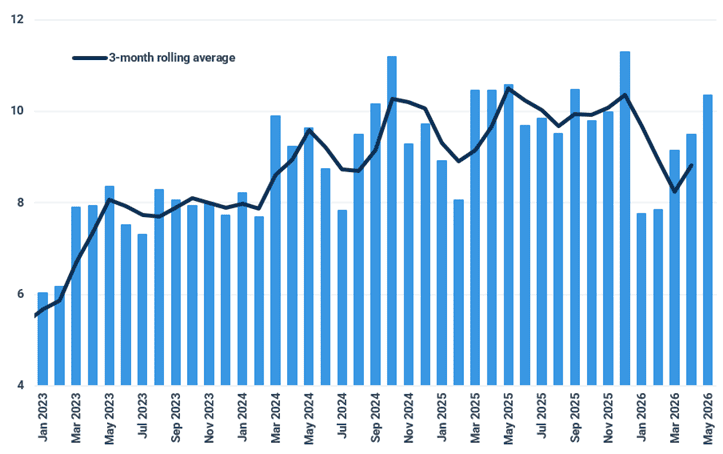

- Steel exports have again been a relatively bright spot. Customs data show that exports reached a year-to-date high of 10.34Mt in May, though they are still 2.24% below the year-ago level. The resilience of exports likely reflects producers adapting to the new export licensing regime introduced in January, soft domestic demand and the absence of Iranian steel from the export market. However, growing trade barriers, limited access to Gulf markets and Iran’s decision to lift its export ban on slab and flat steel from June are likely to constrain further growth.

- Iron ore prices remained under pressure during the week. Strong seaborne supply growth, subdued Chinese steel demand and elevated metallurgical coal and coke prices continued to weigh on sentiment. The most traded DCE contract, September 2026, edged down 0.39% w/w to 764 yuan/t on 11 June, while the SGX 62% Fe July contract closed flat w/w at $101.50/t.

China’s steel exports reached a year-to-date high in May (Mt)

Source: China Customs, Kpler Insight

Coal: Thermal coal trade strengthens as summer demand rises

- Global seaborne thermal coal exports rose 14% y/y to 19.60 Mt in the week ending 7 June, marking the second-highest weekly volume so far in 2026. The increase was primarily driven by stronger seasonal demand across key importing markets as the Northern Hemisphere summer is closer.

- Export performance varied significantly among major suppliers. Shipments from Australia and Russia strengthened sharply, while Indonesian exports fell to a seven-week low of 7.97Mt as delays in export approvals and certificate-of-origin processing at several ports might have affected export efficiency. The development follows Indonesia’s decision to gradually channel commodity exports, including coal, through state-owned enterprises, with Danantara Strategic Investments (DSI) overseeing transactions during the June–August transition period.

- South African exports also weakened significantly. Seaborne thermal coal shipments fell to 0.84Mt, the lowest level since August 2025, reflecting softer demand from Indian sponge iron producers. Logistics disruptions compounded the weakness, with a day of rail suspension between Iswepe and Wildrand following a derailment reducing deliveries to export terminals. Looking ahead into the coming days, a fresh train derailment involving 17 wagons near Richards Bay on 8 June may pose new challenges to exports. Although stockpiles at RBCT remain healthy, the latest incident may still delay some shipments.

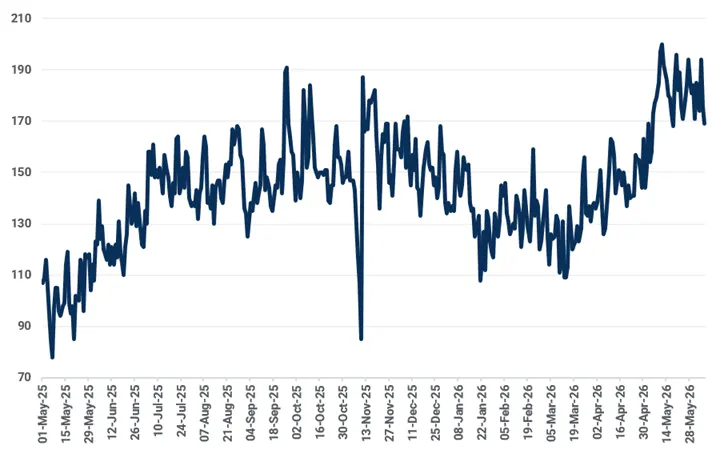

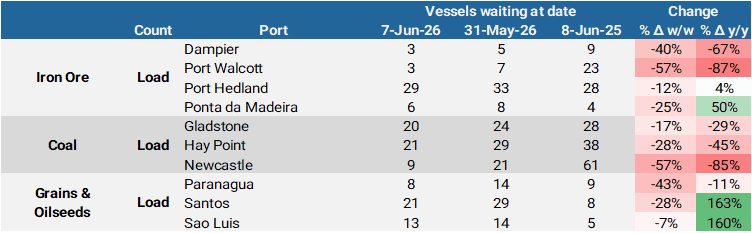

- On the demand front, global seaborne thermal coal imports edged up 1.20% y/y to 18.20Mt in the week ending 7 June.Chinese imports climbed to a four-month high of 5.72Mt ahead of the summer peak demand season. However, elevated inventories and port congestion may constrain further near-term growth. Coal vessels waiting to discharge at Chinese ports remained around 170 in early June, compared with approximately 120 a year earlier.

- In metallurgical coal, global seaborne imports rose 18% to 6.50Mt against a low base a year earlier. Indian imports eased to a five-week low of 1.62Mt as monsoon rains began to weigh on construction activity and steel demand. Chinese imports also moderated after reaching year-to-date highs in the previous fortnight. While safety inspections following the fatal mine accident on 22 May continue to constrain domestic metallurgical coal supply more than thermal coal production in China, weakening steel output is likely to limit further import growth.

Coal vessels waiting to discharge at Chinese ports (Mt)

Source: Kpler

Grains & Oilseeds: Grain markets take a breath ahead of the USDA WASDE report

- The cascade seen across several key agricultural commodities on the Chicago Board of Trade (CBOT) stabilised as the market awaited the release of the June World Agricultural Supply and Demand Estimates (WASDE) report. For the week ending 2 June, funds had reduced their net long position for CBOT corn by 90,422 lots, the largest w/w reduction since May 2025. In addition to the precipitous decline in CBOT wheat, the corn market had come under pressure following reports of favourable yields in Mato Grosso as the safrinha corn harvest gets underway in Brazil. Also, several cases of the New World screwworm have been detected in cattle across Texas, which threatens corn demand for US animal feed.

Net position for CBOT corn by managed money (k lots)

Source: CFTC

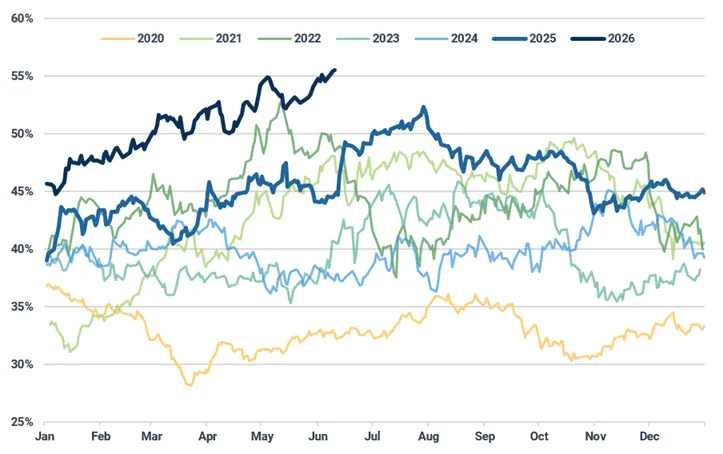

- Though CBOT soybean meal had also felt the pressure from funds liquidating long positions during the latter half of last week, support for soybean oil has remained robust. Nearby CBOT soybean oil share has reached a record high of 55.5%. Despite the weakening of CBOT soybeans, the nearby board crush has sloped lower, after exceeding $4/bu at the beginning of the month. Nonetheless, soybean crush margins remain historically high, and US demand is likely to remain at a record pace as crushers push towards maximum utilisation.

CBOT soybean oilshare (nearby, %)

Source: MarketView

- The development of the US corn and soybean crops remains broadly favourable. By 7 June, 86% of the US corn crop had emerged, in line with the 5-year average. For soybeans, 79% had emerged, ahead of the 5-year average by 8 percentage points. For both crops, the percentage rated in good or excellent condition is close to last year's. Though rainfall was excessive in parts of the Midwest, the weather has been favourable for crop development, given its current vegetative stage. Following ample rainfall, current soil moisture reserves will offer a supportive buffer should dry conditions emerge, alleviating drought risk.

- Planting of Argentine wheat was 32% complete by 3 June, surpassing the pace of previous years due to favourable soil moisture conditions. After rainfall during May had been short of historical levels, the beginning of June saw the arrival of much-needed showers. This has partially alleviated dryness concerns as limited rainfall has been forecast for the latter half of the month. For soybeans, harvest was 92% complete by 3 June, while the corn harvest was 41% complete. Though planting is still several months away, the recent softening of urea prices has been influencing spring planting decisions for Argentina, and could see fewer corn acres lost y/y.

- While the fertiliser market has been softening, the movement of fertiliser-laden vessels via the Strait of Hormuz remains limited. Since the beginning of June, 5 vessels have exited the Middle East Gulf (MEG). As the number of loadings within the region has stagnated, this has seen the number of fertiliser-laden vessels decline to its lowest level since mid-March. For grain trade, the number of cargoes transiting the Strait of Hormuz is also minimal, with only 6 vessels having entered the MEG since the start of the month, all of which were destined for Iran.

Minor Bulks: Aluminium prices ease on inflation fears while alumina surges

- Aluminium prices have retreated as escalating tensions in the Middle East fuelled concerns that higher energy costs could reignite inflationary pressures and complicate the Federal Reserve’s monetary policy outlook. The three-month LME aluminium contract fell 4.70% w/w to $3,494/t at the time of writing on 11 June, while both the US Midwest premium and the European P1020 premium pulled back from their recent record highs.

- China’s exports of aluminium and aluminium products rose 16% y/y to 0.63Mt in May, the highest level since late 2024. The increase suggests Chinese producers are continuing to exploit favourable export arbitrage opportunities created by supply disruptions in the Middle East. However, the scope for further export growth may be limited unless international prices surge again, as China's aluminium capacity is already constrained by the 45Mtpa ceiling and domestic inventories continue to decline.

- Alumina prices moved in the opposite direction, rising on renewed supply concerns despite fundamentally oversupplied market conditions. Environmental inspections in China’s Shanxi Province could directly affect 2Mtpa of refining capacity, while uncertainty persists over potential bauxite export restrictions expected from the Guinean government later this month. Against this backdrop, the most traded alumina contract on SHFE, September 2026, surged 5.04% w/w to 2,899 yuan/t on 11 June.

- GCC alumina imports finished at 0.09Mt in the week ending 7 June, with the majority of volumes still discharged at Sohar. Notably, the Supramax Luna Li was confirmed to have discharged alumina at Jebel Ali in late May, becoming the latest alumina vessel to successfully transit the Strait of Hormuz since the conflict began. The Black Berry is expected to discharge a cargo of alumina at Jebel Ali in the coming days.

Aluminium and alumina prices have again diverged ($/t)

Source: MarketView, Kpler Insight

Dry Bulk Freight: Capesize earnings plunge as vessel supply rises in the Pacific

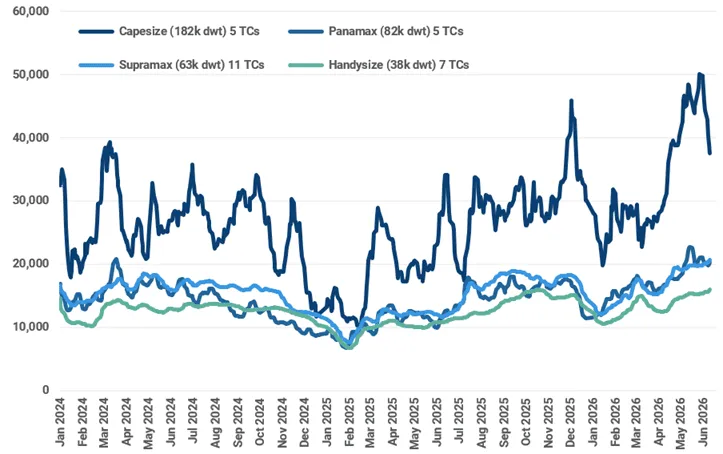

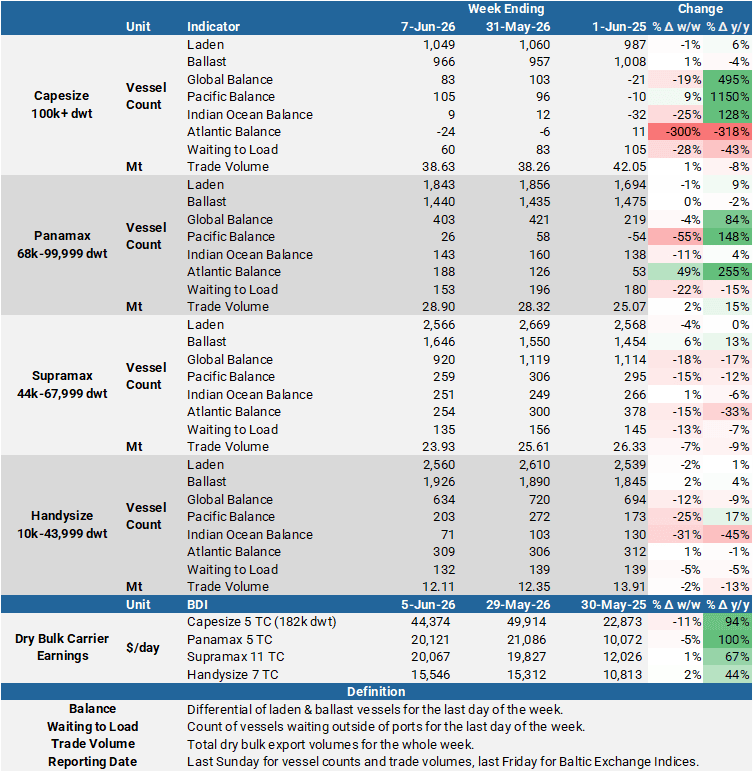

- The slide in Capesize earnings was expected. The 5 TC average is down by $8,156/day w/w to its lowest point since April at $37,551/day. Earnings had surged ahead of the rest of the dry freight market to unsustainably high levels, and a pushback from charterers was likely. With Singapore International Ferrous Week next week, the number of active players in the market is likely to be reduced, and further declines in fronthaul earnings, which only fell by 5% w/w, are likely in the short term.

- The Capesize Pacific round-voyage rate plunged by $16,691/day (-39%) w/w to $26,363/day. We maintain the view that the Capesize Atlantic earnings premium vs the Pacific, $19,375/day at the time of writing, is unsustainably high. However, with the discharging of bauxite and iron ore cargoes lifting the ballaster count in the Pacific to a year-to-date high of more than 470 ships, while supply has tightened in the Atlantic, it is likely to remain elevated in the short term. High bunker prices discourage speculative ballasting, and the seasonal slowdown in West African bauxite exports has cut one of the demand drivers taking ballasting vessels out of the Pacific and to the Atlantic.

- Declines in the Capesize sector were not reflected across the rest of the dry bulk freight market. In sharp contrast, average earnings for Panamax vessels were almost unchanged w/w at $20,255/day, while the Supramax and Handysize TC averages climbed by $625/day and $514/day, to $20,645/day and $16,022/day, respectively.

- High ballaster availability is weighing on Pacific Panamax earnings and countering a seasonal ramp-up in coal chartering activity. This trend is likely to persist as more ships come open after discharging Brazilian soybeans in China. The round-voyage rate dropped by almost $2,000/day w/w to $20,156/day, while the Atlantic market firmed. A similar trend was observable in the Supramax and Handysize markets, where rates out of the US Gulf and South America firmed, but Indonesian coal routes struggled to achieve sustained upward momentum. However, an ample supply of geared ballasters in the Atlantic is likely to cap the upside potential for earnings.

- With fighting in the Middle East intensifying over the past week, including several attacks on merchant shipping, dry bulk trade through the Strait of Hormuz has slowed to a trickle. A return to normal shipping in the region is a long way off. Just 12 ships transited in the seven days to 10 June, down from 13 the previous week, and 23 the week before. Most of these were dark transits, but two vessels took the IMO route through the middle of the Strait. Three ships carrying fertiliser exited the Middle East Gulf, while the most common cargo amongst those ships entering the region was grains and oilseeds.

Capesize earnings in decline, but smaller vessel markets prove more resilient ($/day)

Source: Baltic Exchange

Key Dry Bulk Market Developments

Dry Bulk Commodity Flows

Source: Kpler

Dry Bulk Port Congestion

Source: Kpler

Dry Bulk Freight Metrics

Source: Kpler, Baltic Exchange

Market insights you can trust

Kpler delivers unbiased, expert-driven intelligence that helps you stay ahead of supply, demand, and market shifts.

Trade smarter. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler