QatarEnergy loads onto first LNG tanker from outside of the Gulf as Hormuz risk premium unwinds

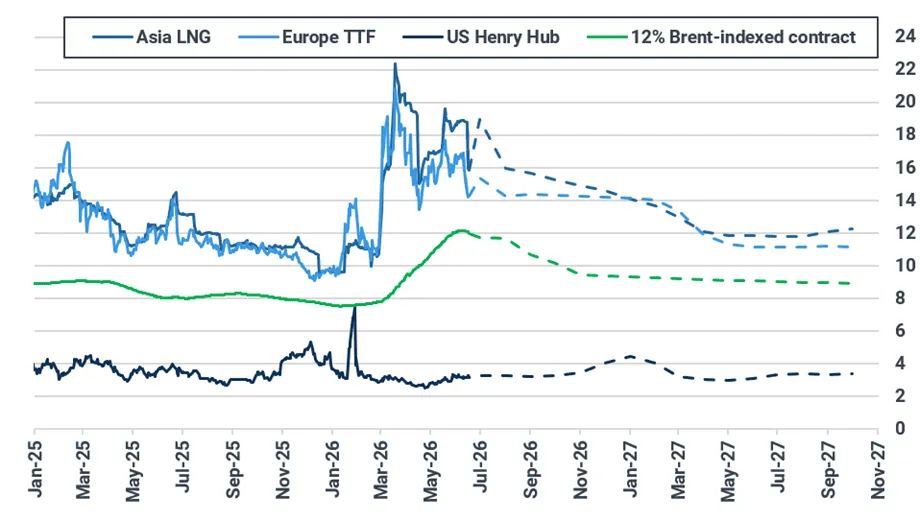

TTF is expected to edge lower next week, weighed down by potential peace deal developments, recovering TurkStream flows, warmer temperatures, and strong renewables limiting gas burn. Asian LNG is set to remain stable as tight prompt fundamentals — strong Chinese demand, active Thai buying, and South Korean nuclear outages — offset the easing of the Hormuz risk premium, widening the Asia-TTF spread slightly. Henry Hub is expected to remain rangebound, with recovering LNG feed gas deliveries offset by weak weather-driven demand and rising domestic gas production.

Market & Trading Calls

European TTF front-month price outlook: Slightly bearish, with potential peace deal developments and more Qatari loadings likely to weigh on prices. Fundamentals will also put downward pressure on TTF, with warmer temperatures and strong renewable generation to limit gas burn. Recovering TurkStream flows will also keep pipeline supply ample. Storage injections are expected to remain robust, with the balance-of-summer summer/winter spread having narrowed to just €1.1/MWh and could tighten further if bearish momentum materializes.

Asian LNG front-month price outlook: Stable, as the remote signing of a US-Iran agreement and easing Hormuz disruption concerns have removed much of the geopolitical risk premium. While Kpler is observing signs of QatarEnergy commencing loadings—supporting the prospect of up to 2.9 mt of additional Qatari LNG supply during June-September above our June LNG monthly base case—we expect the recovery in flows to be gradual rather than immediate. Continued uncertainty surrounding negotiations throughout the 60-day implementation period should preserve some residual risk premium, while stronger Chinese LNG demand, active Thai buying, and South Korean nuclear outages keep prompt fundamentals relatively tight ahead of the peak summer season.

Asian LNG – TTF spread outlook: set to widen slightly, as Asian LNG is expected to remain stable while TTF decreases. Asian LNG maintained a $1.58/MMBtu premium over TTF on 17 June (-$0.43/MMBtu w/w).

US Henry Hub front-month price outlook: Stable, as mixed fundamentals keep prices rangebound. Despite the completion of maintenance at several LNG export projects bringing increased LNG feed gas deliveries, weak temperature-driven demand and stable production will limit gains. Additionally, minor gains are likely to be met with profit-taking, further curtailing potential upside.

Key natural gas and LNG front-month prices ($/MMBtu)

Source: ICE, NYMEX. Brent-indexed price represents 12% slope of 90-day moving average of Brent contract.

Asian LNG-TTF front-month spread ($/MMBtu)

Source: ICE, Kpler Insight

Europe: Potential Hormuz re-opening , higher temperatures, strong renewable generation and recovering Turkstream flows to instil bearish pressure on TTF.

The European TTF front-month contract fell w/w to $14.24/MMBtu on 17 June, down 15.8% from $16.91/MMBtu on 10 June. A potential geopolitical breakthrough was reached after a MoU was signed between the US and Iran, paving the way for a potential peace deal in the Middle East. This was followed by an 8.8% d/d decrease in TTF on 15 June – the largest drop in two months. On the fundamentals side, local distribution consumption remained similar to year-ago levels and gas-fired generation remained weak amidst strong renewable generation, while LNG imports rose w/w.

Looking ahead, Kpler Insight maintains a slightly bearish outlook for the TTF front-month contract. Geopolitics continue to drive price movements, as bearish pressure is expected ahead of US and Iranian negotiation teams meeting in Geneva this Friday and possible developments regarding a durable peace deal. The possibility of more Qatari loadings is also set to add further downward pressure, with the Al Hamla being the first QatarEnergy vessel to re-enter the Middle East Gulf since before the war began. On the fundamentals side, the bearish tone is set to remain. Warmer temperatures are expected in southern and western Europe, and strong renewable generation will limit gas-fired demand.

On the supply side, EU net pipeline imports increased by 5.5% w/w to an estimated 3.1 bcm, primarily driven by the return of Russian flows (+0.3 bcm) as TurkStream volumes recovered after scheduled maintenance. Flows from all other suppliers remained strong. Looking ahead, Kpler Insight expects net pipeline imports into the EU to remain stable w/w, supported by robust flows across most major exporters. Gassco's maintenance schedule remains largely unchanged for next week, keeping Norwegian flows robust.

Daily Russian pipeline exports (bcm)

Source: Kpler European Gas, Kpler Insight.

Gassco daily unavailability (mcm/d)

Source: Kpler European Gas, GASSCO.

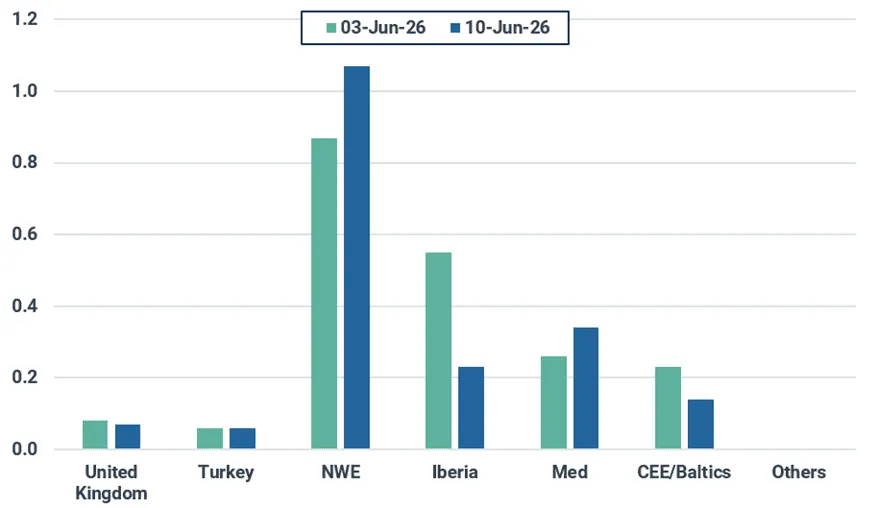

EU-27 LNG imports fell by 6.8% w/w to 1.9 mt, driven by a drop in imports into Iberia and the CEE/Baltics despite an uptick in NWE and the Med. Looking ahead, LNG imports are expected to slightly fall w/w, as scheduled outages continue at some French and Spanish terminals. Meanwhile, the NWE DES–TTF spread was reportedly trading in negative territory last week on the back of expectations of a faster Qatari ramp-up, thus keeping Europe competitive for flexible LNG cargoes, despite the steady rate of diversions away from Europe to Asia (six so far in June).

It is important to mention that near-record US LNG export volumes are expected to reach European markets in two weeks, adding bearish pressure alongside Qatar's gradual production recovery.

European weekly LNG imports by region (mt)

Source: Kpler Insight. Data represents week commencing 03/06 and 10/06. NWE=FR, BEL, NL, GER. Iberia=ESP, POR. Med=ITA, HVR, GRE. Baltics/CEE=FI, LT, POL. Others=SWE, MT.

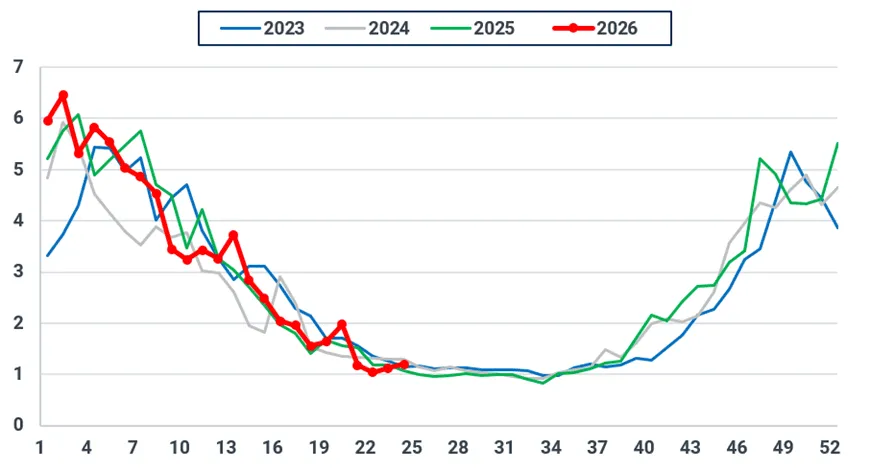

Regarding demand, aggregate local distribution consumption across 16 EU countries increased by 7% w/w to an estimated 1.2 bcm, in line with our previous expectations. The gain was driven by slightly colder temperatures across parts of Europe, falling to seasonal levels by the end of last week. Looking ahead, Kpler Insight expects a slight decrease in local distribution demand, as temperatures are forecast to increase above seasonal averages, particularly in Western and Southern Europe where a heatwave is expected.

EU-16 weekly consumption in the local distribution sector (bcm)

Source: ENTSOG, ENAGAS, Eustream, AGCM, Kpler Insight. The EU-16 perimeter includes AT, BE, DE, CZ, FR, HU, GR, IT, NL, LU, PL, PT, RO, SL, SK, and ES.

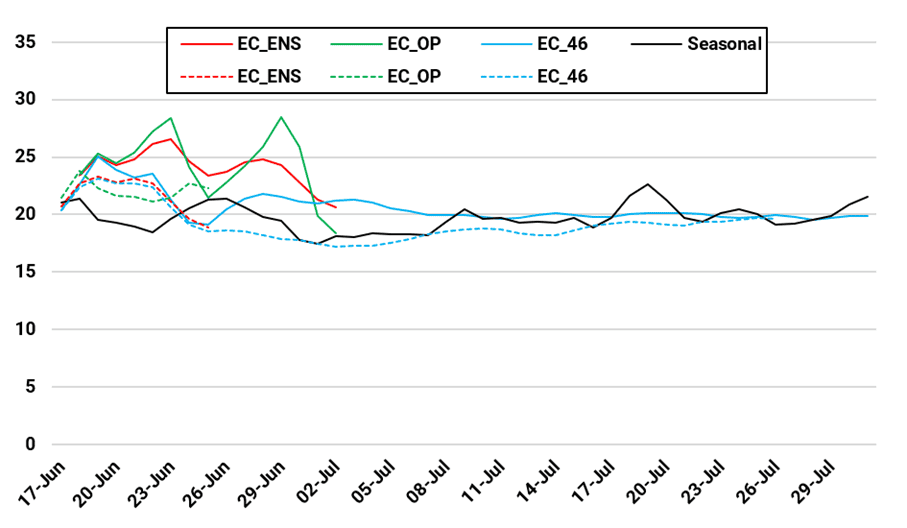

Average forecast temperatures for NWE, excluding the UK (°C)

Source: Kpler Insight. Run comparison 18/06 (solid) vs. 11/06 (dotted), 00:00 UTC. Seasonal is a five-year average. NWE includes BE, NL, FR, DE

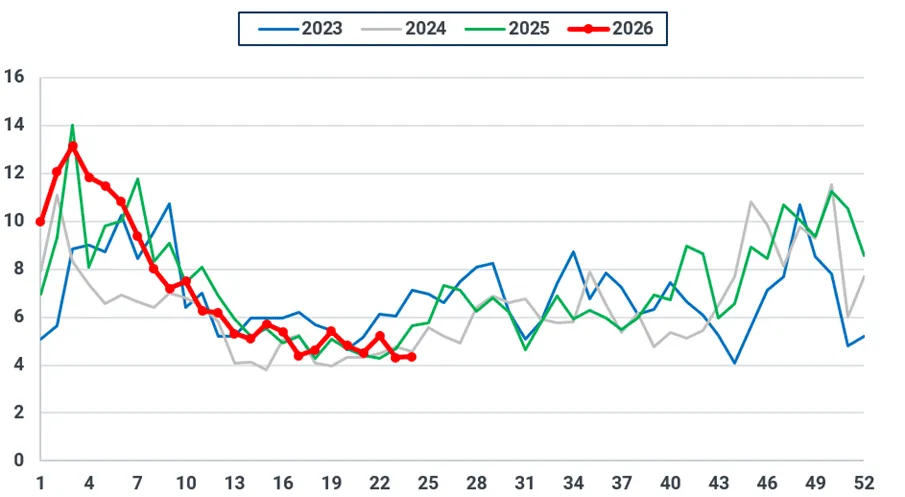

In the power sector, EU-25 gas-fired generation was relatively stable w/w, increasing by just 1% to an estimated 4.4 TWh. While solar generation dipped from the record levels reached in the previous week, solar output still remained well above seasonal averages, especially in south and southeastern Europe. Wind generation recovered as well, while overall power demand only slightly increased by 2% w/w. Looking ahead, Kpler Insight expects gas-fired generation to modestly decline, as wind generation is expected to continue recovering in NWE, while solar generation is forecast to remain strong across Europe as temperatures rise.

EU-25 weekly gas-fired generation (TWh)

Source: Kpler Power, Kpler Insight.

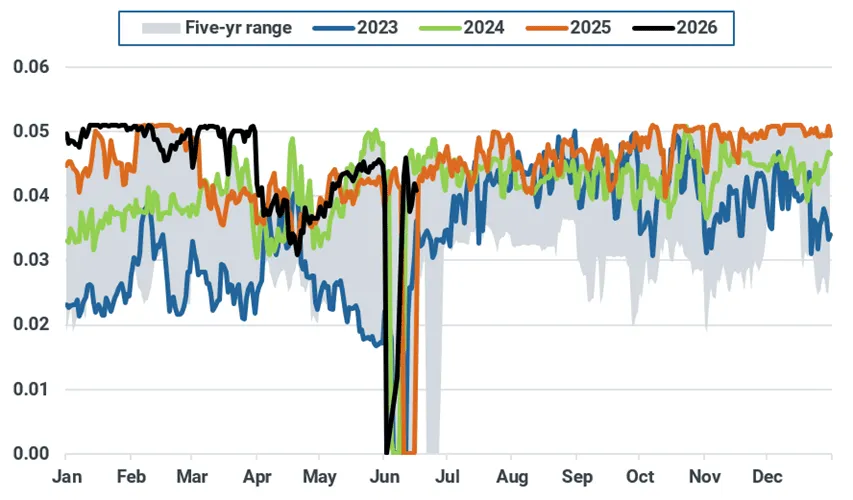

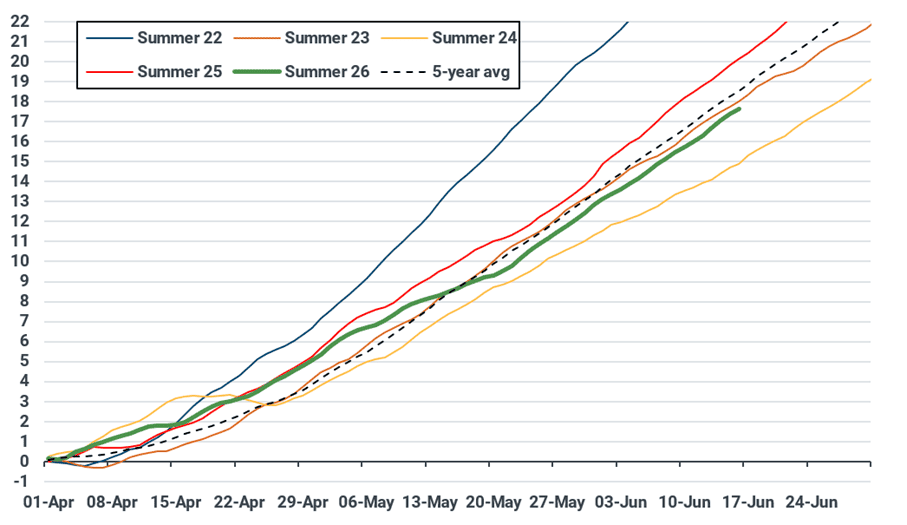

EU-27 underground gas storage levels rose to 45.3% as of 16 June, 2.2% higher w/w. Injections over the past week remained in line with the five-year average and broadly even with 2025 levels. Nevertheless, net cumulative injections remain 0.9 bcm below the five-year average, reaching 17.7 bcm (see chart below). It was worth noting that Dutch fill levels have now surpassed Belgian facilities by 0.2 pp, despite ending winter at just 4.6% full (compared to 25.5% for Belgium). While net cumulative Dutch injections have been strong, those in Belgian have been relatively flat from the start of April. This was likely due lower-than-average LNG imports into Zeebrugge since May and stronger Belgian gas-fired generation, due a particularly deep nuclear maintenance schedule this year.

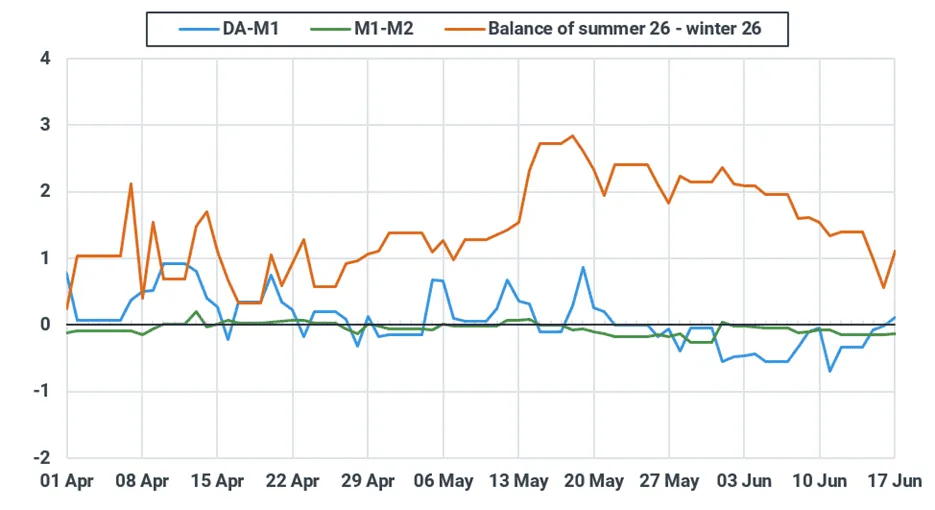

Looking ahead, Kpler Insight expects injection activity to remain robust as temperatures rise and gas-fired generation remains weak. While the balance of summer/winter spread is still at a premium (and thus not incentivising injections), a declining trend has been emerging, with the spread falling to €0.6/MWh on 16 June, owing to a pronounced decline in the July TTF contract. The spread is now trading at a €1.1/MWh premium and could continue narrowing if additional bearish pressure weighs on the market.

EU-27 net cumulative UGS injections since 1 April (bcm)

Source: GIE, Kpler Insight. Latest data as of 16 June 2026.

Selected TTF contract spreads (€/MWh)

Source: Kpler Insight, Argus, EEX. DA = day-ahead; M1 = Month ahead; M2 = Two month ahead.S

Croatian gas transmission operator Plinacro has completed the Zabok–Lucko pipeline, one of four interconnected gas pipelines needed to fully utilize the expanded capacity of Croatia's Krk LNG terminal. The FSRU's annual send-out capacity was increased from 3.9 to 6.1 bcm last year, but pipeline bottlenecks prevented limited offtake. With the Zlobin–Bosiljevo pipeline commissioned in March 2025 and the remaining lines expected to follow this year, completion of the network will enable transmission of up to 1.5 bcm per year to Slovenia and 3.5 bcm per year toHungary, supporting Croatia's ambitions to become a regional gas hub.

Want the complete report?

The full report is available within Insight and contains:

- Market & Trading Calls

- Europe: Potential Hormuz re-opening , higher temperatures, strong renewable generation and recovering Turkstream flows to instil bearish pressure on TTF.

- Asia: Geopolitical premium fades on hopes of a Hormuz reopening, but weak Chinese gas production limits downside

- Henry Hub prices rangebound on below-average temperature outlooks, rising domestic gas production

- Global LNG supply: First ballast QatarEnergy vessel arrives in Middle East Gulf, starts loading at Ras Laffan

Trade smarter. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler