Gulf grains under fire: Hormuz, rerouting, and why Iran is better placed than it looks

The closure of the Strait of Hormuz has forced a rapid reshaping of grain supply chains across the Gulf, but the headline story is one of adaptation rather than collapse. Saudi Arabia and the UAE have rerouted effectively, with Red Sea ports absorbing the Saudi pivot and Fujairah stepping in as the UAE's sole grain gateway. Iran, the region's largest buyer, is in the most resilient position of all. Corn imports were front-loaded before the conflict began, and a domestic wheat harvest now underway reduces import needs for the coming months. The real test arrives in July, when Brazil's corn export season resumes and Chabahar's ability to scale will determine how comfortably Iran manages the second half of the year. Saudi Arabia's decision to buy only for Red Sea delivery through August signals that Riyadh is planning its supply chains around a continued closure rather than waiting for the strait to reopen.

Gulf importers saw arrivals fall sharply as Hormuz disruption took hold

The Gulf crisis disrupted grain flows across much of the region between March and May 2026. Several countries saw arrivals drop sharply or go to zero at the height of the disruption. For most Gulf states (countries with coastline in the Mideast Gulf), grain imports flow almost exclusively through Gulf-facing ports such as Jebel Ali, Bandar Imam Khomeini, Shuwaikh and Umm Qasr, all of which sit behind the strait. Saudi Arabia's Red Sea facing ports have served as a lifeline. Iran and UAE have kept their imports flowing through rerouting, albeit at a slower pace.

Gulf region grain imports dipped in April before a partial May recovery (kt)

Source: Kpler

UAE saw the sharpest pivot

Gulf-side ports, which accounted for virtually all UAE grain arrivals in January and February 2026, went to zero in March and April as vessels were diverted away from Hormuz. Fujairah, located on the Sea of Oman and accessible without transiting the strait, absorbed the entire import volume during this period, surging to 307 kt in April. May figures are preliminary, and vessels currently indicating Jebel Ali as their destination are likely to divert to Fujairah while the strait remains closed.

UAE grain arrivals have pivoted from Jebel Ali to Fujairah (kt)

Source: Kpler

Saudi Arabia's Red Sea ports absorbed the Hormuz disruption without a break in supply

The bulk of Saudi Arabia's grain import capacity sits on the Red Sea, not the Gulf. King Abdulaziz Port in Dammam, the main Gulf-side terminal, handled 557 kt in January but dropped to 119 kt by April as Gulf routing became untenable. Red Sea ports absorbed the extra volume without much issue. Yanbu Commercial, Jeddah, King Abdullah and Jizan collectively handled over 1,500 kt in April, up from around 1,200 kt in January, keeping total monthly arrivals broadly stable. May data is preliminary but points to the Gulf share falling below 1% as rerouting becomes near-total.

Saudi Arabia's Red Sea facing ports have served as a lifeline, providing a reference point for how established alternative routing can function at scale. The Kingdom has continued buying grain through the disruption and in its most recent wheat tender specified Red Sea delivery only, with Dammam conspicuously absent. Shipments are contracted for June to August, a signal that Riyadh is planning its forward purchases on the assumption that Hormuz remains closed for the coming months.

Saudi grain imports have shifted almost entirely to Red Sea ports

Source: Kpler

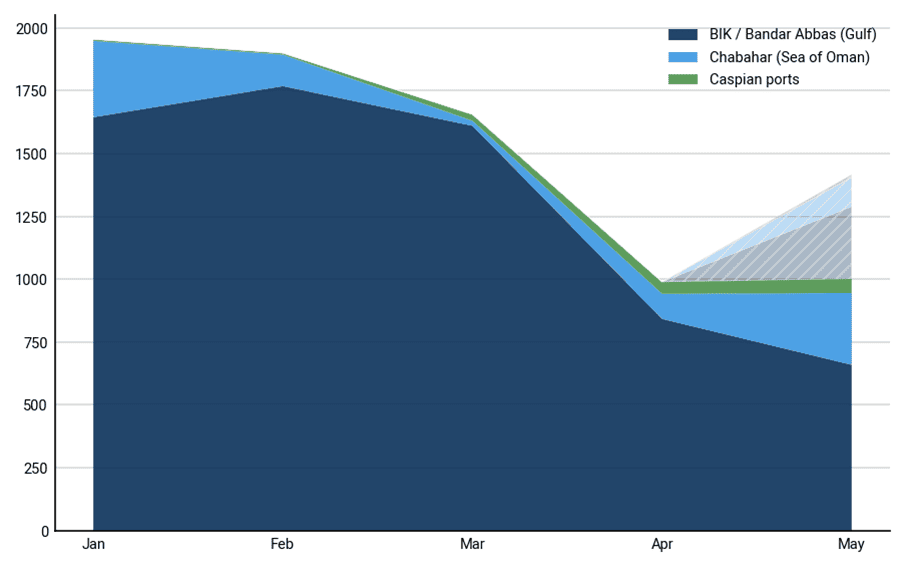

Iran reroutes through Chabahar as BIK volumes slow, corn stocks provide a buffer

Iran is the largest grain importer in the region by volume but also the least food insecure. Wheat purchases fluctuate sharply by harvest year, ranging from 1.4 Mt in TY2024 to 7.1 Mt in TY2021, reflecting its domestic production rather than structural reliance on imports.

On the port side, BIK peaked at 1,768 kt in February and began falling through March and April. April volumes were still substantial, but much of that reflects cargoes already inside the Gulf before the conflict began rather than new arrivals navigating a disrupted strait. The rerouting to Chabahar, Iran's deep-water port on the Sea of Oman, is now showing in the data. Chabahar is scheduled to handle 402 kt in May, its highest monthly figure of the year. Caspian port volumes have also been rising month on month, though they remain small in absolute terms at around 70 kt in May.

On corn, Iran had been running notably high import volumes in the six to eight months before the conflict began. A group of Brazilian corn vessels that had gathered outside BIK at the outbreak of the conflict has since discharged, adding to what was already a heavily loaded import pipeline. Brazil's corn export season also enters its seasonal lull from May to July, reducing the pressure of new arrivals over the coming months.

Iran is also currently harvesting its domestic wheat crop. The harvest is expected to come in lower y/y, but domestic production still covers at least 60% of the country's annual wheat consumption, meaning wheat imports are not a near-term necessity. With corn imports front-loaded and wheat needs met largely from the domestic crop, Iran's grain supply position is the most resilient of the countries affected by the disruption over the next few months.

Iran's Gulf port arrivals have fallen while Chabahar and Caspian flows rise (kt)

Source: Kpler

The summer buying season will test whether rerouted supply chains can hold

Saudi Arabia's June-August tender is the market's clearest implicit forecast on Hormuz. Riyadh specified Red Sea delivery only and left Dammam out, which means the Kingdom is preparing for a longer closure. If the strait remains closed when that delivery window closes, the next tender will push further out and begin to settle the question of whether Gulf-side port infrastructure is being written off for the medium term.

For UAE, Fujairah has absorbed the diversion from Gulf-side ports without visible strain so far. The test is whether it can sustain elevated throughput across the summer buying season, when monthly grain volumes historically run higher. With vessels currently bound for Jebel Ali expected to divert to Fujairah, the port is effectively the UAE's sole grain gateway for as long as the strait stays closed.

For Iran, the pressure point arrives in July when Brazil's corn export season resumes. Chabahar handled an encouraging volume in May but is still running at a fraction of BIK's pre-conflict throughput. The coming months will show whether the port can absorb a step-change in arrivals or whether Iran will need to lean harder on Caspian routing. But Iran enters the summer in a stronger position than the port data alone suggests. Corn imports were front-loaded before the conflict began, and the domestic wheat harvest is now underway. A siege is only as effective as the hunger it creates. For the next few months, Iran's fields are doing the defending.

This article was written by an AI using data from the Kpler MCP, cargo and S&D APIs, then reviewed and edited by an analyst. Estimated analyst contribution: 30%.

See why the most successful traders and shipping experts use Kpler

.jpg)