Second tranche of Chinese export quotas to offer little relief to Asian product markets

China's second refined product export quota tranche keeps pace with last year on paper, but increased outflows are unlikely. With Beijing prioritizing domestic supply security, margins deeply negative across the refining complex, and inventories sufficient to sustain current run rates well into 2027, the path of least resistance is run cuts — not exports. EoS CPP supply remains structurally tight until the margin and geopolitical picture clears.

- China's 13 Mt second export quota tranche matches last year's pace, but various pressures mean export volumes won’t.

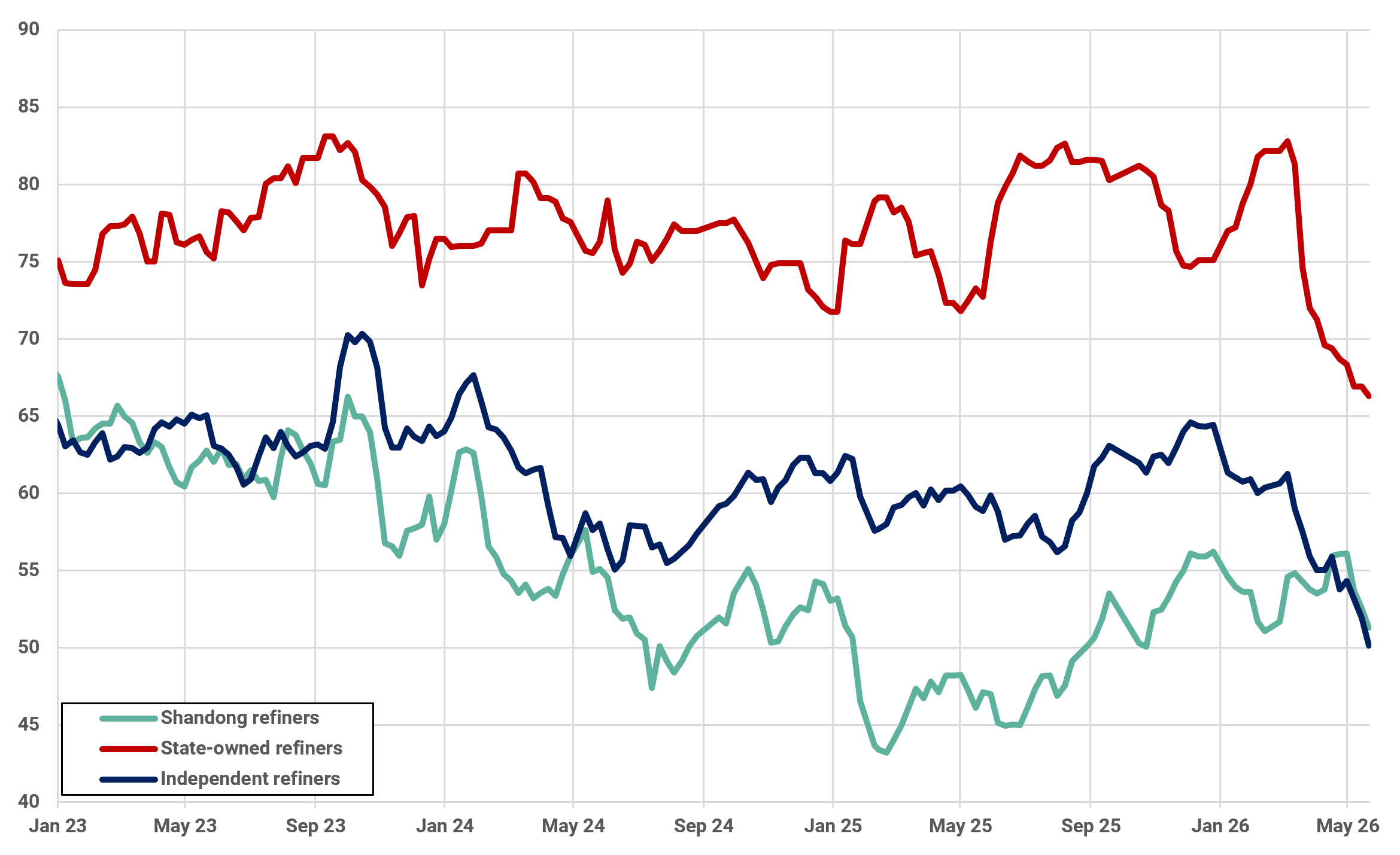

- Beijing has handed refiners a run-cut lifeline, and they are taking it.

- Chinese export suppression to keep EoS products supply tight: at least until margins improve and the geopolitical picture clears.

China has issued a second tranche of refined product export quotas totaling around 13 Mt, though allocation by refiner remains unconfirmed. The award brings cumulative CPP quota issuance for the year to approximately 32 Mt — broadly in line with last year's 31.8 Mt — but the timing is notably late. Second-batch awards have historically landed between April and May; the delay into June reflects a year in which Chinese oil product exports have run well below typical averages, as the ongoing US-Iran conflict has compelled Beijing to prioritize domestic supply security over outbound flows, with only modest volumes reaching Southeast Asian buyers.

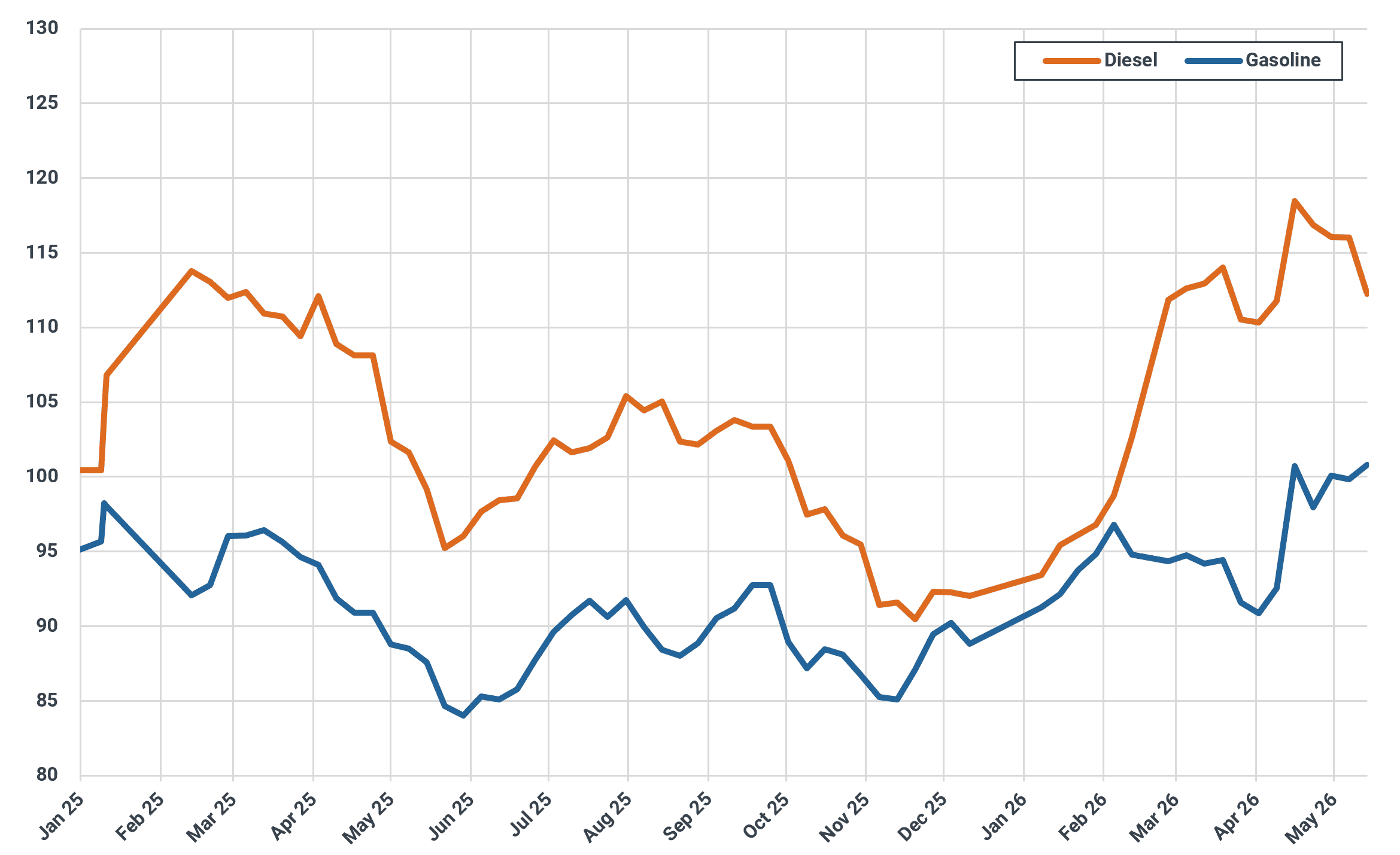

Chinese gasoline and diesel commercial inventories* (Mbbls)

*Inventory data comprises sales company stocks, commercial stocks, and independent refinery stocks

Source: Mysteel Oilchem

Commercial gasoline and diesel stocks have been building steadily, with ullage constraints emerging in parts of the country; yet the quota award does little to suggest Beijing intends to use exports as the primary relief mechanism. The delay reflects a deliberate priority: Beijing's overriding concern since the conflict escalated has been domestic supply security, with export market obligations a distant second. Chinese crude imports are likely to hover around 7 Mbd through July, implying modest crude inventory drawdowns of around 1 Mbd over the period. Against that backdrop, reading this second tranche as anything more than a routine, administrative top-up is difficult to justify.

The more consequential policy decision came separately: Beijing has quietly allowed refiners to cut output to 80% of year-ago levels — a meaningful concession given that margins have turned deeply negative. Shandong independent refiners are operating at around -$6/bbl, while state-owned refiners face losses closer to -$18/bbl (Mysteel OilChem). With the economics of running hard actively destructive, the path of least resistance is run cuts rather than exports – a trend already visible since late February, when utilization began a sustained slide to multi-year lows.

Chinese refiner run rate (%)

Source: Mysteel OilChem

See why the most successful traders and shipping experts use Kpler