After the deal: Transits could near 50% of pre-war levels in 30 days

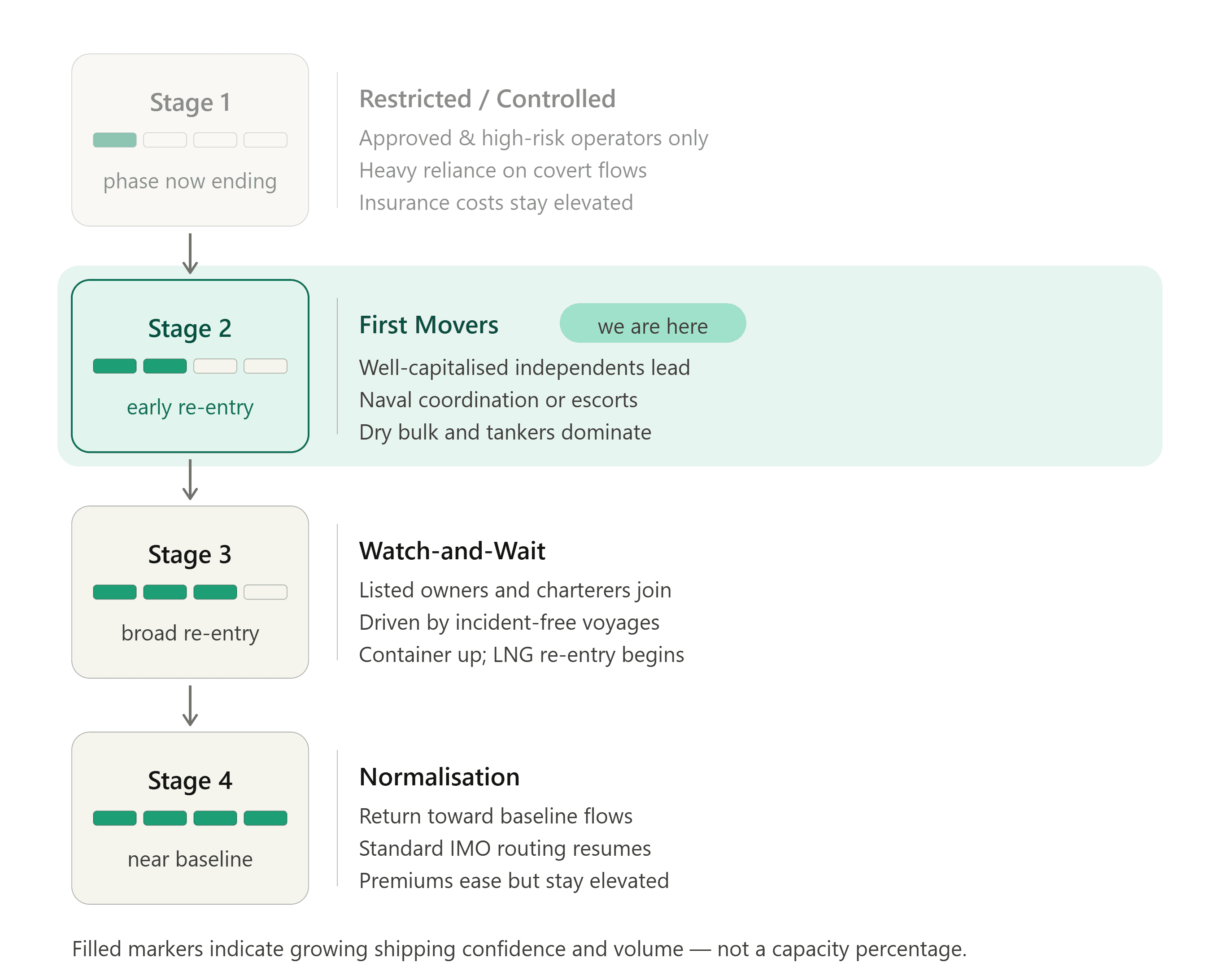

A weekend agreement between Washington and Tehran has, on paper, outlined a re-opening of the Strait of Hormuz on 19 June. This would shift the status from the Restricted/Controlled phase and into the First-Mover phase of our reopening framework. But several core terms of the deal remain ambiguous - whether the Strait has been mined, whether Iran retains de facto operational control, and how transit tolls will be set and collected. Until these are resolved, a rapid return of commercial shipping is far from assured. Below we set out how the vessel backlog within the Mideast Gulf clears, present a fast-return path and our base case for re-entry, and explain why the recovery may be stop-start rather than linear.

Market & Trading Calls

- The agreement nudges Hormuz from Stage 1 (Restricted/Controlled) into Stage 2 (First Movers), but unresolved terms cap how quickly vessels actually re-enter.

- The first visible move is a one-off backlog release - laden vessels exiting - rather than a durable step-up in throughput.

- In a fast-return scenario, we present the maximum shipping capacity available which is only constricted by the number of vessels in range of the Mideast Gulf (MEG).

- In our base case, the return of shipping capacity in the MEG is staggered and the climb is gradual from 15 per day to 40 per day over the first month, assuming there are no setbacks. This compared with pre-war levels of 90-100 for bulk commodity carriers.

- Reopening faces disruptions. Incidents, slow-moving insurance and disputes over implementation point to plateaus and occasional reversals.

Strait of Hormuz vessel transits (days from start of peace agreement)

Source: Kpler

The starting point: a backlog, not a clean slate

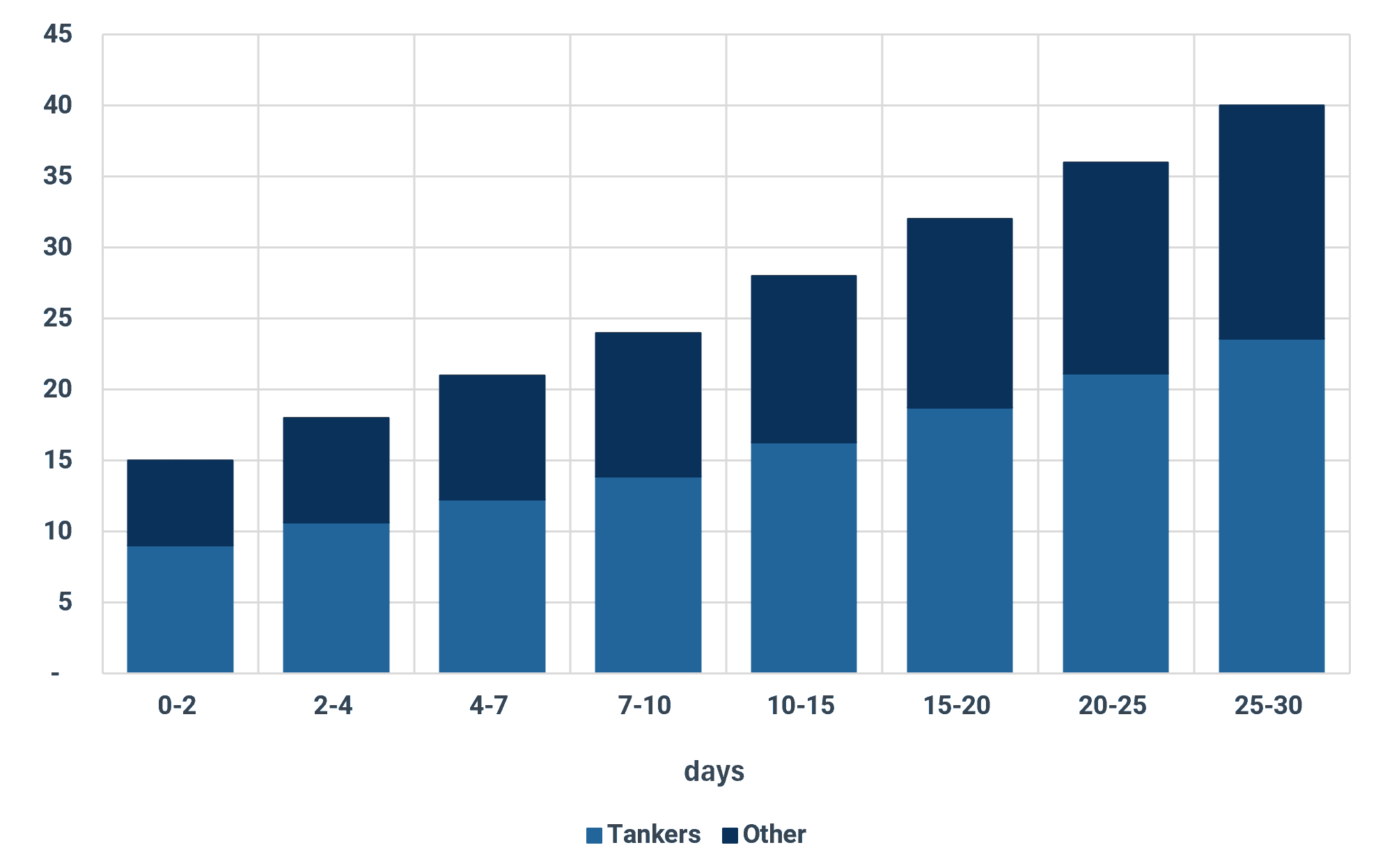

After more than 100 days of disruption, the Strait does not reopen onto normal trade; it reopens onto a backlog. Laden vessels trapped inside the Gulf that were unable to exit will be the first to exit. How quickly these clear, and in what order, will shape the first weeks of the recovery, and is easily mistaken for the underlying pace of normalisation. Laden vessels already inside the Gulf will be the quickest to move: they are loaded, committed, and need only safe passage and acceptable war-risk cover to sail. Their exit produces the first, and largest, visible jump in transits. Our base case assumes the backlog of 118 laden tankers (MR or larger) could be cleared in 10-15 days.

Laden backlog –Count of laden tankers to exit the Mideast Gulf (=>MR)

Source: Kpler

Vessels re-entering: two scenarios

The key analytical point is that the backlog release is a one-off. It can make the first fortnight look like a rapid recovery, but it draws down a stock of delayed vessels and cargo rather than reflecting a sustainable lift in flows. The true pace of re-entry will be the speed at which vessels re-enter the Mideast Gulf, and that is where our two scenarios diverge. However, the large backlog means the number of vessels able to enter will likely be limited in the first few weeks under our base case scenario as exiting vessels take priority.

Stages of a return in Hormuz transits

Scenario 1: Fast return

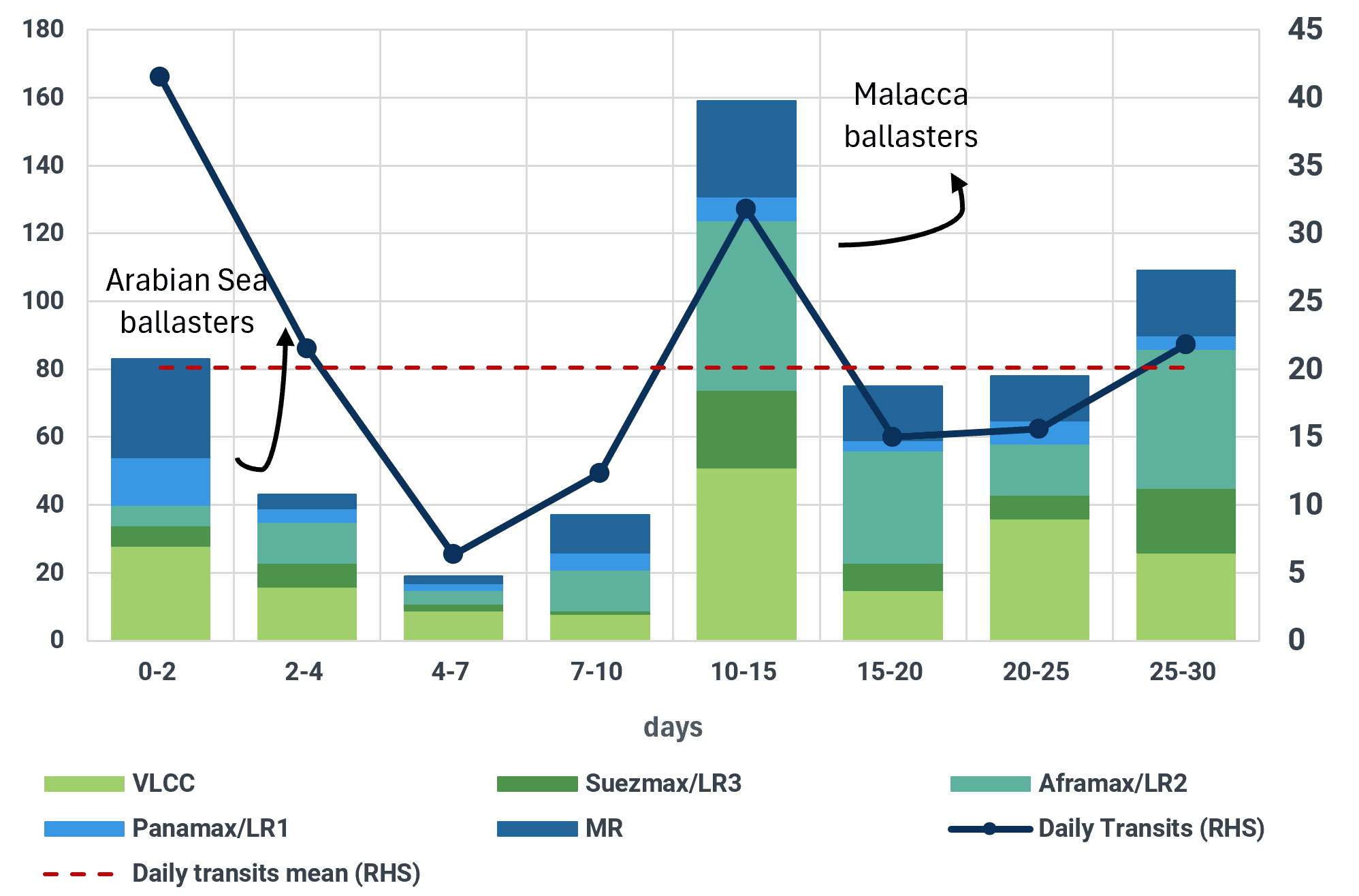

Our fast-return path is a theoretical maximum supply of vessels able to arrive in the Mideast Gulf based on their current position outside the region. This assumes the deal is honoured cleanly: the Strait is confirmed clear and safe to navigate, Iran does not impose conditions on movement, and a credible security presence reassures operators. As a result, this assumes a return to maximum transits immediately. Average tanker transits (entry and exit) pre-war were between 50-60. This scenario would see periods in which levels exceed pre-war levels. Considering the ongoing risk and potential constraints, we consider this scenario unlikely.

Empty tankers available to enter Mideast Gulf by days to port (11 knots) (days from start of peace agreement)

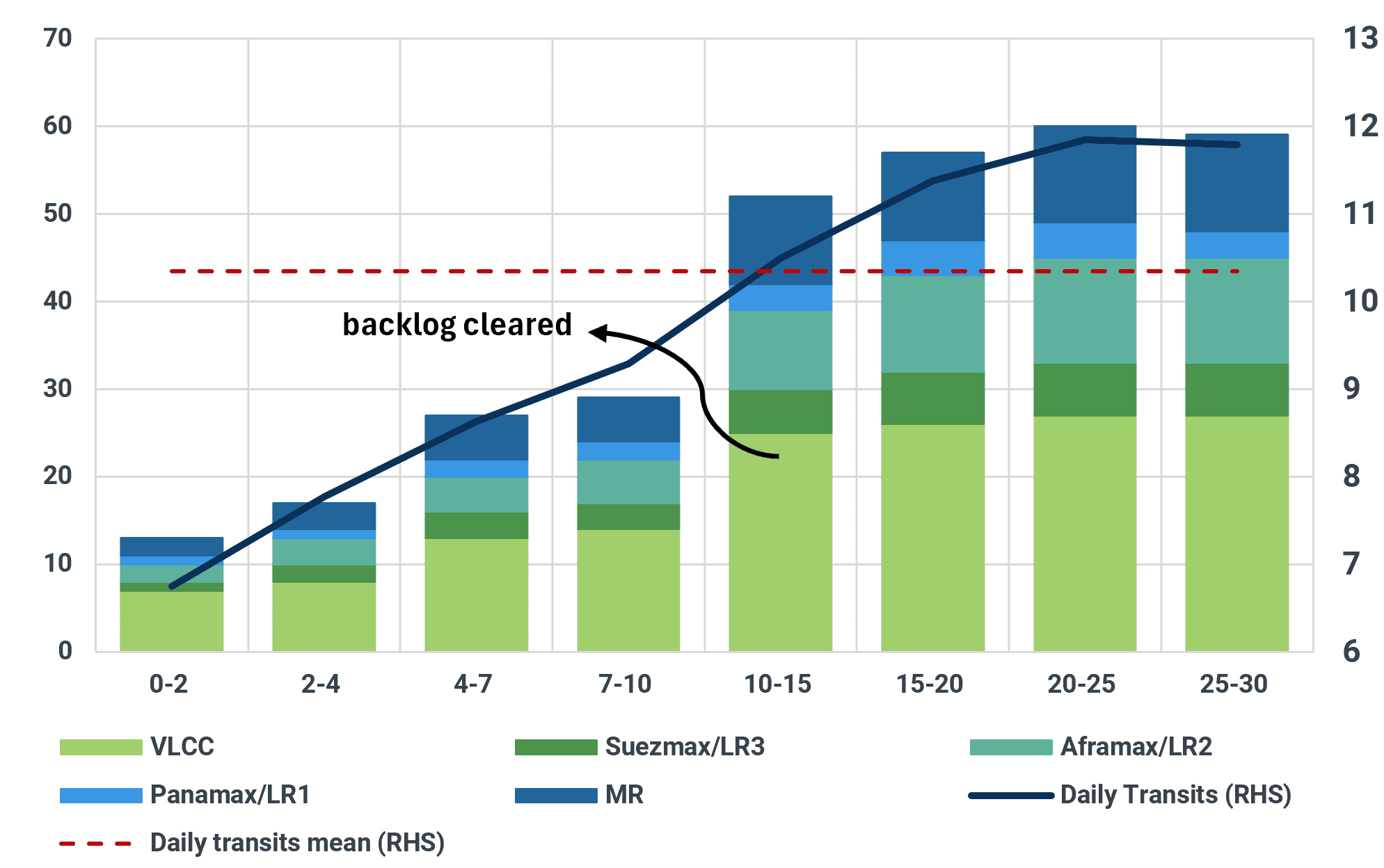

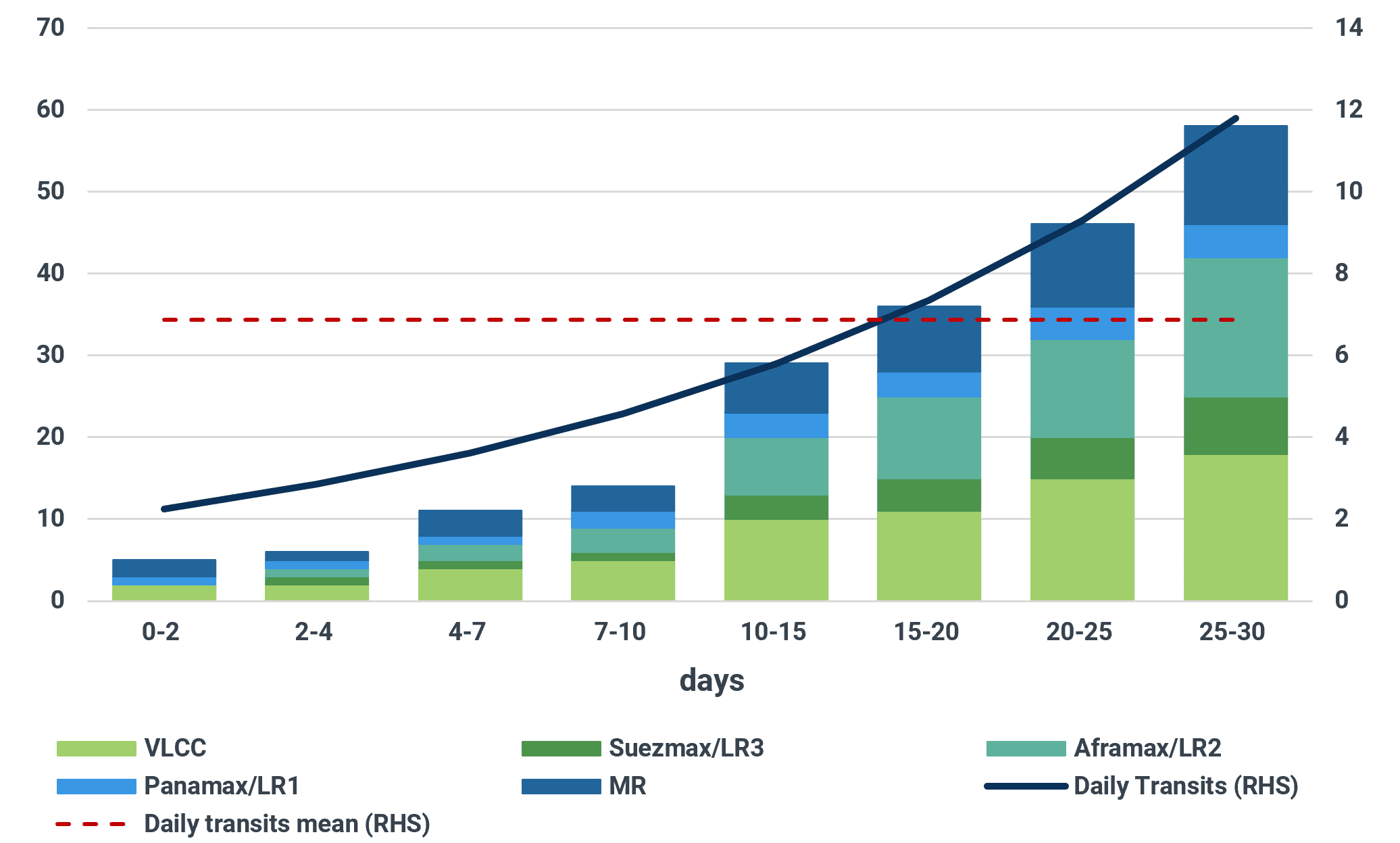

Scenario 2: Slow return (Base Case)

This scenario takes the deal at less than face value, because several of its terms are unresolved and each one bears directly on whether owners sail. However, our case assumes the deal holds and the return of vessels reflects ongoing market caution and vessels availability, rather than any assumed disruption.

The first-mover principle still holds and is in fact reinforced after more than 100 days of disruption. Many will prefer to wait and see how the deal holds before committing tonnage, and the market is understandably sceptical. As we noted through the April and May period, reduced kinetic activity did not translate into a meaningful recovery in flows; progress stalled even as the fighting eased. In the base case we expect re-entry to be staggered with transits rising from 15 per day to around 40 per day by the end of the first month with tankers accounting for around 60%. At the end of the first 30 days, the number of tankers entering the Gulf could rise to 12/day, which remains around 50% below pre-war levels.

Base case - Tankers entering MEG by class* (days from start of peace agreement)

*Excluding dark shuttle tankers from Mideast Gulf to Gulf of Oman

Why reopening may not be linear

Re-opening comes with numerous risk to these scenarios. The mechanics of this recovery point to a stop-start path with plateaus and the occasional reversal, for several reasons:

- Terms of the deal are reneged – A major risk to the re-opening is both side reneges on an aspect of the deal. The most likely could be ongoing skirmishes between Israel and Hezbollah. Iran is likely to use any breach of the terms of the deal as justification to re-assert control of the Strait.

- Is the Strait mined? If mines were laid, clearance operations could run for weeks or longer, and a single incident would reset confidence and war-risk pricing across the whole corridor. Indeed, a single seizure, gunboat incident or mine strike can stall progress.

- Insurance lags security - cover adjusts on a track record, not an announcement, so the financial conditions for re-entry trail the security picture by weeks. Freight rates will need to remain high to cover these costs.

- Does Iran retain de facto control? If access remains conditional upon approval processes or mandatory routing through Iranian waters then it remains very unlikely that most other countries in the region will engage.

- How are tolls set and collected? If transit charges flow to the IRGC, a US-designated entity, owners and their P&I clubs face a sanctions and compliance problem that better security alone cannot solve. Until the mechanism is clarified and demonstrably compliant, many owners will simply stay out.

- Implementation disputes - the most ambiguous terms (how tolls are collected, who polices the Strait, what role Iran retains) are exactly the points most likely to be disputed in practice, and disagreement over them can pause or reverse progress between stages.

- Vessel-class divergence - because tankers and dry bulk return well ahead of container and LNG, headline capacity figures will mask a very uneven recovery beneath the surface.

Each transition - First Movers to Watch-and-Wait, Watch-and-Wait to Normalisation - requires operators to clear a fresh confidence threshold, and any of the factors above can knock them back below it. The realistic expectation is therefore a stepwise recovery punctuated by stalls, with the unresolved terms of the deal the single most likely source of delay.

See why the most successful traders and shipping experts use Kpler