Cometh the time, Cometh the optimisation: The barrel bends toward jet

Refiners are doing exactly what tight jet fuel markets would suggest: producing more jet fuel. What began as a scramble to replace disrupted Middle Eastern jet fuel supplies has evolved into a global refinery optimisation cycle. Strong margins disrupted trade flows and supply security concerns have triggered a broad-based shift toward kerosene production across Europe, the US and parts of Asia. The latest production data confirms that yield optimisation is translating into meaningful supply gains, helping offset supply disruptions and alleviating pressure on global jet fuel balances.

Europe: The Data Confirms the Shift

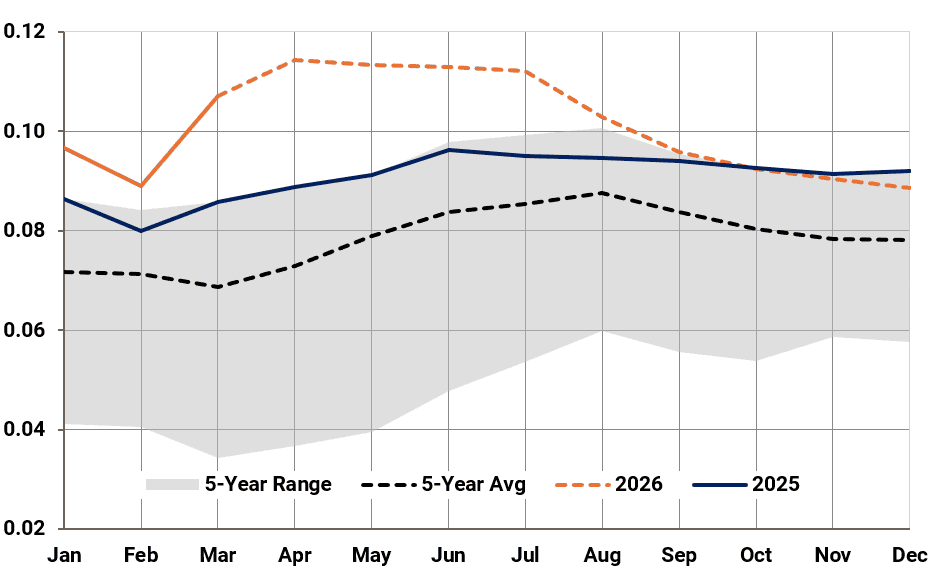

The disruption of Middle Eastern product flows through the Strait of Hormuz exposed Europe's structural dependence on imported jet fuel and created a strong incentive for refiners to maximise kerosene recovery. In previous reports, highlighting how operators could widen kerosene cut points, increase hydrocracker severity and redirect feedstocks toward middle distillates. The latest production data suggests that optimisation measures have translated into a meaningful increase in supply as Europe continue to rebalance it jet fuel supplies.

March jet fuel production increased by around 200 kbd y/y, while refinery yields rose by approximately 2.1 percentage points y/y and 1.8 percentage points m/m. The increase was broad-based across the continent, evident in France, Italy, Spain, the UK, Germany and Greece. More importantly, the data exceeded expectations. As highlighted in Kpler's Supply & Demand outlook (May Refined Product Balances), we projected European jet fuel production growth of around 160 kbd y/y through yield optimisation. Actual growth came in closer to 200 kbd y/y, confirming that refiners have been able to shift yields more aggressively.

Europe: Jet/Kero - Refinery Yield (%)

Source: Kpler

The trend is expected to persist through the summer. We forecast European jet fuel yields to remain around 2 percentage points above last year's levels through August, generating approximately 225 kbd of additional supply despite refinery throughput remaining largely flat y/y. In other words, the increase is being driven primarily by optimisation rather than higher crude runs.

A Global Yield Shift

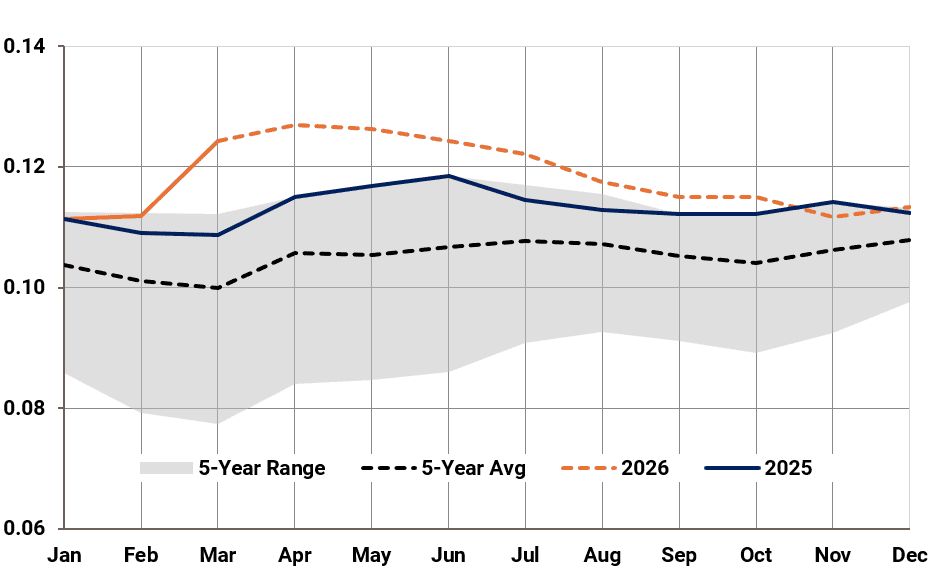

Europe may be leading the response, but it is far from alone. US refiners increased jet fuel yields by around 1.6 percentage points y/y in March (EIA), generating roughly 310 kbd of additional production. Of this increase, around 60 kbd stemmed from higher crude throughput, while approximately 250 kbd came from yield optimisation and product slate adjustments.

US: Jet/Kero - Refinery Yield (%)

Source: Kpler

Nigeria's Dangote refinery has also emerged as an important contributor. Following the resolution of operational issues earlier this year, the refinery has increasingly prioritised jet fuel production, reflected in exports, with yields approaching 22% as material is redirected away from the gasoline and gasoil pools.

South Korean refiners have followed a similar path, with March jet fuel yields rising by around 1 percentage point y/y. Current economics suggest these elevated yields will be maintained through the peak summer travel season. In Japan, March yield improvements were more modest, but further optimisation is expected over Q3, with jet fuel yields projected to increase by around 1 percentage point between March and August.

Not all regions are following the same path. China's jet fuel yield is expected to decline by around 0.3 percentage points this year (March-August) as export restrictions and Beijing's push to prioritise domestic gasoline and diesel production limit refinery flexibility. Similarly, India's jet fuel yield was lower by around 1 percentage point y/y in March and April, as refiners shifted production toward gasoline and gasoil amid stronger domestic fuel demand, export taxes and government efforts to maximise local fuel availability.

Taken together, the available reported data suggests that the global refining system is increasingly responding to the same market signal: maximize jet fuel production wherever operational flexibility exists. What began as a scramble to replace disrupted Middle Eastern supply has evolved into a broader rebalancing of the barrel.

Yield optimisation, however, remains a zero-sum game. The barrel can be reshaped, but not expanded much. Although refiners can unlock modest incremental volumes through deeper conversion. The shift toward jet fuel has not come without trade-offs. Every incremental jet barrel typically comes at the expense of Gasoil, gasoline, or other competing product streams, a trade-off already visible in tighter gasoline balances across parts of the Atlantic Basin as refiners prioritise higher-value middle distillates.

Conclusion

The common question now is: how much further can refiners go? While jet fuel yields are likely to remain elevated through the summer, the scope for further optimisation is becoming increasingly limited. Most operators have already captured the easiest gains, while jet fuel specifications, hydro processing capacity and refinery configuration architecture constrain further yield shifts. Moreover, as refiners begin positioning for winter diesel production from late Q3 onwards, processing capacity and blending components will gradually be redirected toward diesel, reducing the industry's ability to continue bending the barrel toward jet fuel. For now, however, strong margins and supply security concerns should keep refiners operating in jet-max mode across most major refining centres. The barrel is bending toward jet fuel, and the latest data suggests it will continue doing so through the peak summer travel season, keeping momentum on margins, as road fuel supply takes a back seat.

See why the most successful traders and shipping experts use Kpler