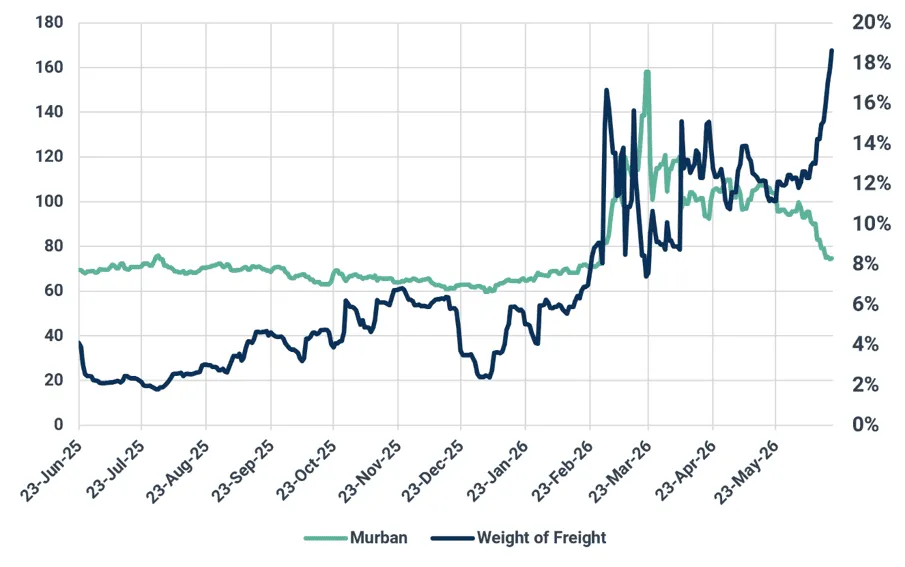

High freight limits exports from the Mideast Gulf

Freight rates for crude exports from the Mideast Gulf (MEG) to Asia remain elevated amid uncertainty surrounding the US-Iran agreement. Crucially, these high rates contrast with falling crude differentials from the region, a divergence that pushed VLCC freight to 19% of the value of Murban at the end of last week. That exceeds the previous record of 17% set at the start of the conflict.

Market and trading calls

- MEG-China VLCC freight: Bullish over the next 2-4 weeks. Owner caution and limited willing tonnage entering the Gulf should keep rates elevated even as Hormuz transits recover.

- Prompt Gulf crude differentials: Bearish. Freight costs have reached 19% of Murban value, the highest level on record, reducing refiners’ willingness to pay higher FOB premiums.

- Atlantic Basin VLCC freight: Constructive. Vessel repositioning toward the Gulf and continued owner reluctance to ballast west should tighten Atlantic availability.

- Owner earnings: Bullish. Owners already positioned in the Gulf retain pricing power while uncertainty persists.

- Risk to view: A sustained period of uninterrupted Hormuz transits and clear security guarantees could accelerate freight normalization.

MEG-China VLCC freight as % of Murban

Source: Kpler, Baltic Exchange, Argus Media

A lack of understanding in the Memorandum of Understanding

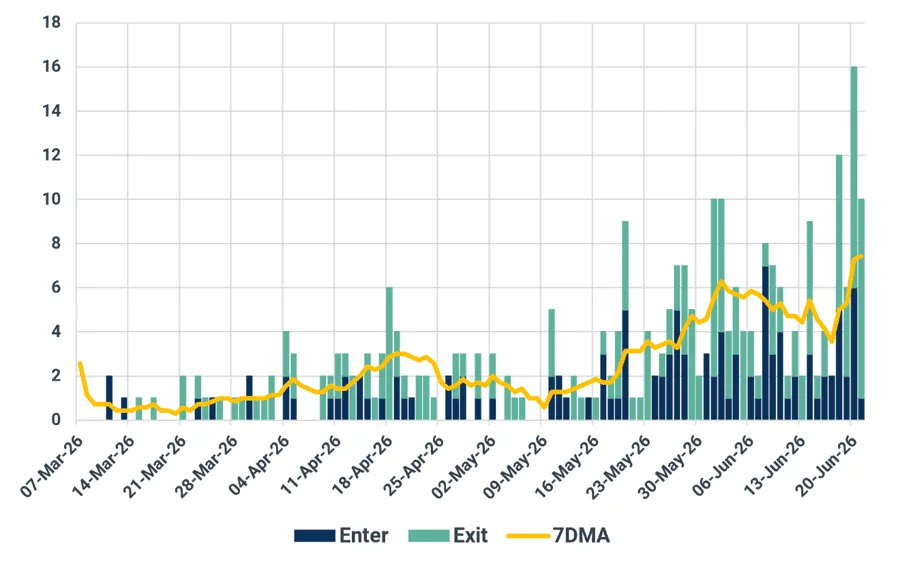

Following the signing of the MoU between the US and Iran last week, under which Iran agreed to allow transits through the Strait of Hormuz to resume unimpeded, the number of tankers entering and exiting the MEG climbed to 17 on 20 June, up from just two a week earlier. However, the increase came shortly before Iran announced the Strait was closed again, reinforcing uncertainty. As expected, outbound vessels account for the majority of transits so far.

Strait of Hormuz non-Iranian linked tanker transits

Source: Kpler

As discussed in last week’s update, the agreement was only the first step toward reopening. The first four weeks remain critical for rebuilding owner confidence. The renewed uncertainty surrounding the status of the Strait has delayed that process.

With little clarity on whether transits are safe, most owners remain hesitant. As a result, transits remain limited and freight remains elevated, broadly in line with our expectations. Tonnage outside the MEG continues to build, yet the number of vessels willing to enter remains comparatively low. Availability outside the Strait is not the constraint; owner willingness to bring vessels into the Gulf remains the bottleneck.

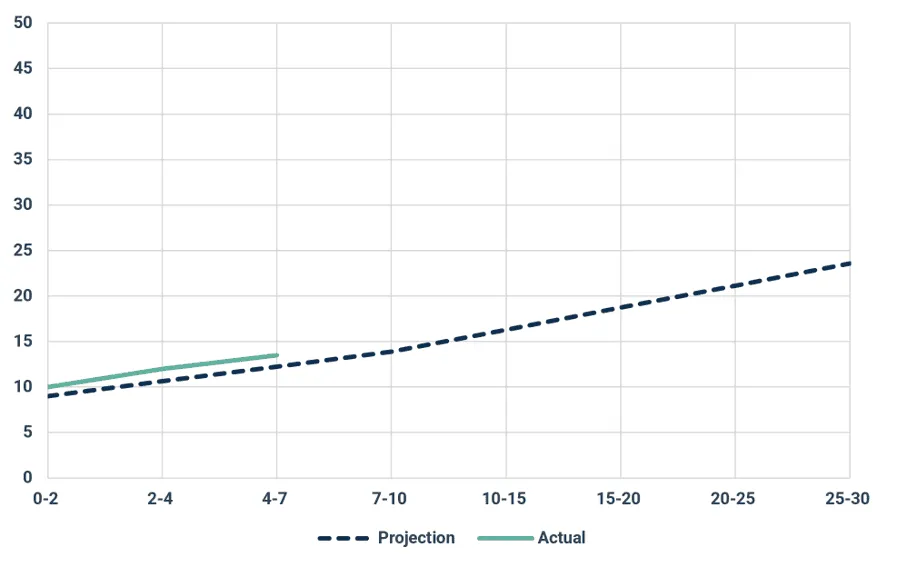

Transits rise in line with expectations

Since the MoU was signed on 18 June, 12 VLCCs have entered the MEG. Five have carried sanctioned-linked cargoes within the previous 12 months. All seven of the non-Iranian-linked vessels can be linked to Sinokor, which controls nearly 130 VLCCs and therefore retains significant negotiating leverage in the market. Consequently, while more VLCCs are entering the Gulf, the shift has not materially improved charterers’ negotiating position.

Strait of Hormuz Tanker Transits vs Prediction (MR+) (Day 1= 18 June 2026)

Source: Kpler

These dislocations are a normal feature of the reopening phase. Exporters were always expected to return ahead of a full recovery in vessel availability. After more than 100 days of uncertainty and repeated disruptions, owner caution remains justified.

We remain bullish on MEG-China VLCC freight through early July. Vessel availability inside the Gulf remains the primary constraint rather than cargo demand, and owner confidence is recovering more slowly than exporter readiness. Whether Hormuz reopening progresses gradually or accelerates, freight should remain supported. Continued uncertainty restricts vessel supply, while faster normalization would increase tanker demand through higher transit volumes.

The key downside risk is a rapid normalization in owner behaviour that brings a larger share of the waiting fleet back into the Gulf faster than cargo demand expands.

See why the most successful traders and shipping experts use Kpler