Weather-related seasonality of crude supply comes to the fore

The market is reacting swiftly to the gradual reopening of the Strait of Hormuz and the potential for unsanctioned Iranian crude to lengthen balances further. As we enter the summer period of seasonally-higher demand, the market is increasingly subject to seasonal supply shocks that are weather-related. The problems and risks are likely to amplify into the future.

Key Takeaways

- Direction: Bullish on prompt heavy sour crude as a 7.5-magnitude earthquake in Venezuela threatens Lake Maracaibo infrastructure.

- Risk Alert: Monitor Canadian heavy differentials; 14 new lightning-ignited wildfires in Mackenzie County, Alberta, present immediate risks to regional crude output.

Immediate heavy crude supply is at risk following earthquakes in Venezuela and fresh wildfires in Alberta, Canada.

Venezuela was struck by consecutive 7.2 and 7.5-magnitude earthquakes located 23 km southeast of Yumare. While the most severe structural damage is centered in Caracas, seismic waves reached Lake Maracaibo, the historic epicenter of Venezuela’s oil production situated 500 km away. Although state-owned PdV has yet to confirm the extent of the damage, the intensity of the quakes suggests a high probability of infrastructure disruption. In a market already navigating uncertain heavy sour flows, any seismic damage to critical production or export facilities will drastically re-price availability in the Atlantic Basin.

While the market is generally oversupplied on a spot basis, the wider market positioning suggests there are upside price risks, especially in the face of significant or prolonged supply outages. Venezuela’s supply has grown by some 330kbd since the start of the war, and has been a key source in rebalancing the crude market.

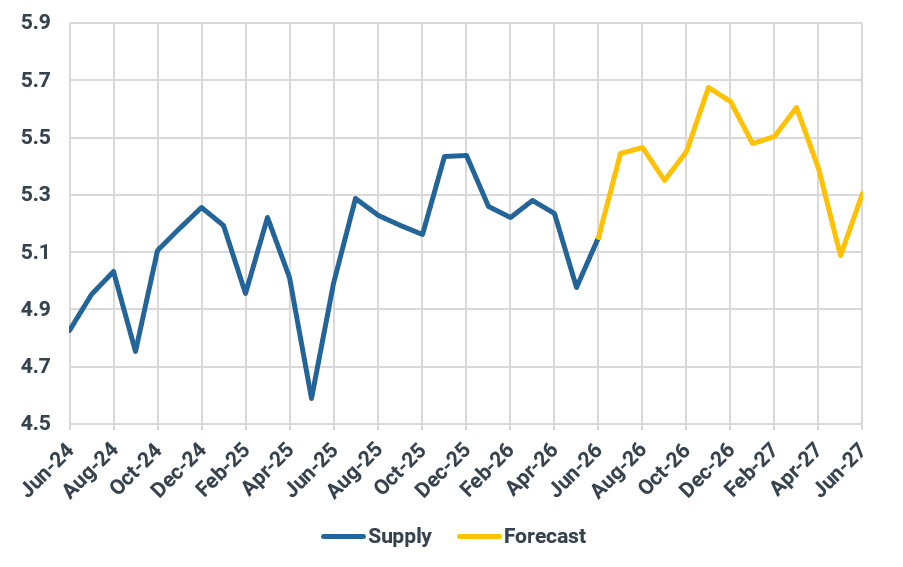

Simultaneously, extreme weather is returning to Western Canada. A severe heatwave in northwestern Alberta has triggered 14 new lightning-ignited wildfires in Mackenzie County, with five already classified as out of control. With the town of High Level placed under a "very high" fire danger rating, Canadian heavy crude operations face imminent curtailment risks. Any substantial shut-ins will aggressively tighten regional balances and provide immediate upside to heavy sour differentials. Since 2023, Canada has lost a peak of around 330kbd of supply to wildfires for around 2 weeks. The severity of this could get worse into the future.

Seasonal nature of Canada's crude oil supply, Mbd

Source: Kpler

An important factor is how cold winters in the US and Canada also pose large supply risks, as evidenced by the past few years.

The US has had supply knocked out by summer hurricanes, but crucially lost a peak of 1.1 Mbd of production in the winter of 2021 for three weeks due to winter storms and freeze offs. More recently, US January production dropped by 410kbd due to winter storm Fern in North Dakota.

The effects are also present on the downstream angle, though are perhaps less extreme in terms of offline capacity. A European heatwave is already hitting parts of German infrastructure. Low water levels on the Rhine are affecting barge traffic for refined products.

Refineries are engineered for high internal temperatures, but rising external temperature extremes are now a systemic risk, affecting everything from reaction control and utility reliability to product blending and storage stability. From strained cooling systems and unstable CDUs to rising quality risks and labour slowdowns, high temperatures are eroding efficiency and reliability.

All in all, the weather and geological risks to supply are becoming more acute, with market positioning and balances determining their effects on price. Any further outages in the Americas, could cause some upside price risk, despite the overwhelmingly bearish market tone currently.

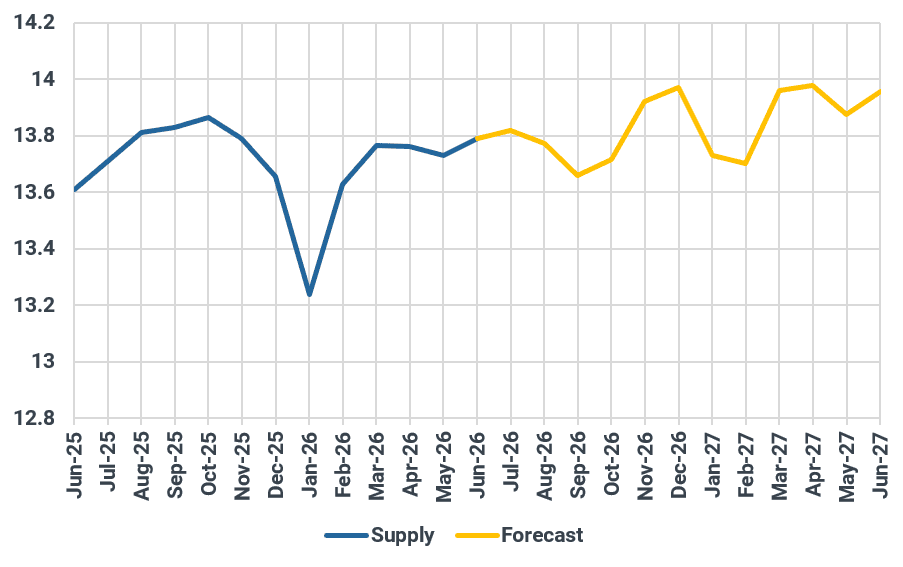

US crude oil supply profile and forecast, Mbd

Source: Kpler

See why the most successful traders and shipping experts use Kpler

![[UPDATE] Middle Eastern supply recovery postponed to early 2027](https://cdn.prod.website-files.com/65059ad784ac02253c62356c/6a69e80d78fefee5dd2f73d6_pipe_line_conection_in_oil_refinery_2_optimized_350.jpeg)