Returning Persian Gulf barrels risk a short-term supply glut

The collapse in the Dubai market was already underway before the US and Iran signed a draft MoU on Friday, with market attention rapidly turning to the risk of imminent oversupply. Shaky grounds indeed.

Key Takeaways:

- The reopening of the Strait of Hormuz (SoH) could immediately release 93 mb of stranded non-Iranian crude. While ballast tankers will take time to enter the Strait, producers are expected to continue relying on STS operations to move cargoes out of the Persian Gulf for the time being.

- ADNOC has issued its third sell tender for the month of June, after reportedly selling at least 40 mb of June- to August-loading crude in the previous two rounds under similar lifting arrangements.

- Middle Eastern producers are likely to require refiners to fulfil their term-contract commitments, limiting their appetite for additional spot cargoes.

- Refinery throughput in Asia ex-China has already recovered to almost 90% of pre-war levels, leaving limited room for further gains, while inventory replenishment demand is likely to take time to materialize.

- China remains a key variable in the emerging oversupply outlook. However, a large-scale increase in crude buying appears unlikely unless Beijing relaxes restrictions on product exports and/or proceeds with another round of SPR replenishment.

The reopening of the Hormuz Strait could unleash some 93 mb of stranded non-Iranian barrels from the Persian Gulf, while producers are expected to continue supplying cargoes through less visible channels. On top of this, the lifting of the US blockade on Iranian crude could release a further 72 mb of Iranian cargoes currently held west of Chabahar, while any eventual sanction waivers could facilitate Iranian exports beyond current levels.

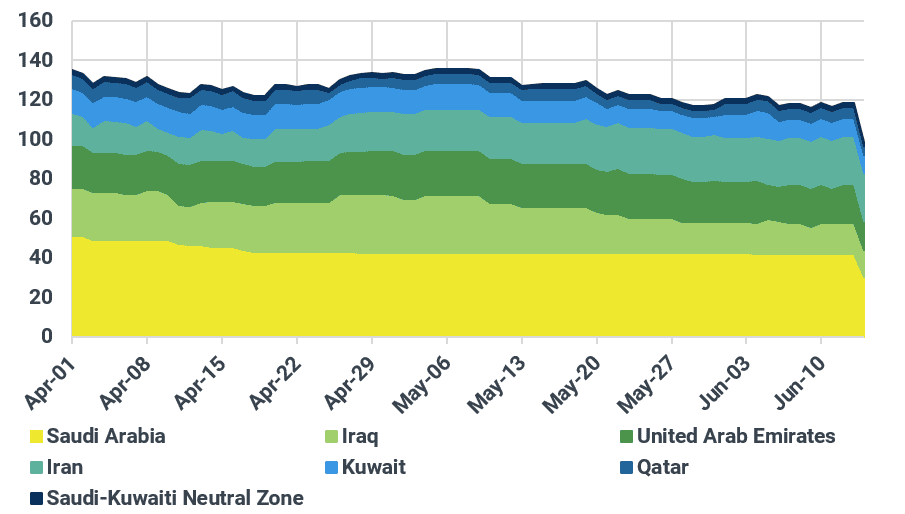

Kpler estimates that once the Strait reopens, laden vessels already inside the Gulf will be the quickest to depart, as they are loaded, committed, and require only safe passage and sufficient war-risk coverage to sail. Provided there are no restrictions from the Iranian side, the backlog could be cleared within roughly 10–15 days. Of these cargoes, 42.5 mb are Saudi, 18.4 mb are UAE-origin, and 15 mb are Iraqi.

Crude/co on water in Persian Gulf by origin, mb

Source: Kpler

While it remains unclear how quickly and under what conditions Iran will reopen the waterway—for instance, whether access will remain conditional, whether transit fees will be imposed, or whether Iran will reopen the entire Strait or only the corridor through its territorial waters—traffic is likely to be slow to ramp up in the initial stages. Against this backdrop, regional oil producers are expected to continue relying on STS operations to move cargoes out of the Persian Gulf.

Kpler data shows that crude oil loaded from the Gulf of Oman after undergoing STS operations surged to 2 mbd so far in June, compared with 772 kbd in May and only 303 kbd in April. Most of these cargoes are likely UAE-origin, with the remainder comprising Kuwaiti and Iraqi barrels.

This week, ADNOC issued its third sell tender of the month, offering June- to July-loading Upper Zakum, Das and Umm Lulu crude. Buyers were given the option to lift cargoes from terminals inside the Persian Gulf, from storage facilities in Fujairah, or via STS operations. This suggests that the current two-leg shipping arrangement is expected to remain in place for at least another six weeks.

In the previous two tenders, ADNOC reportedly sold at least 40 mb of June- to August-loading crude under similar lifting terms, with Chinese, South Korean, Japanese and Indian refiners accounting for the bulk of purchases.

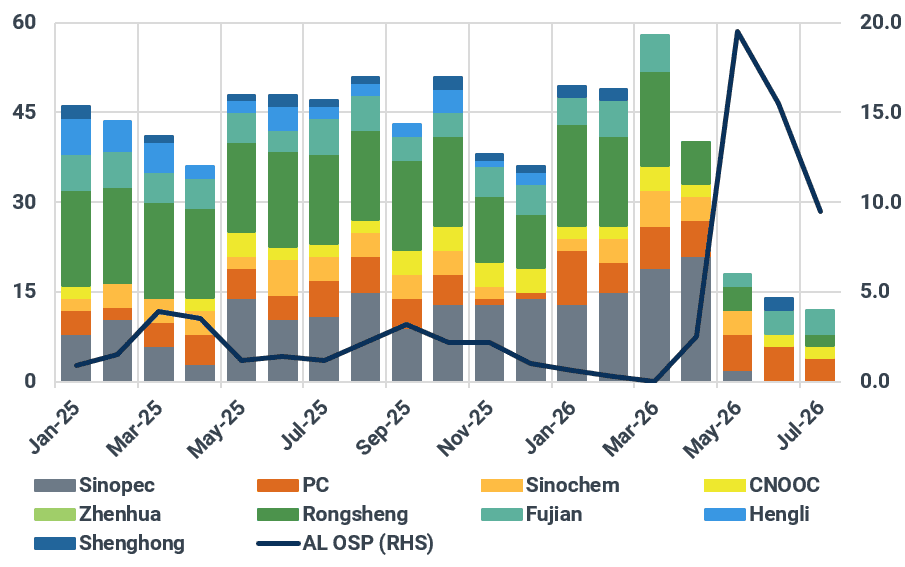

Assuming no further disruptions from Iran to the reopening of the Hormuz Strait, at least 153 mb of non-Iranian supplies from the Persian Gulf are expected to reach the market between June and August, assuming ADNOC awards another 20 mb through its latest tender. As oil production gradually ramps up and more ballast vessels enter the Strait, producers are expected to require term buyers to fulfil their contractual commitments and lift larger volumes from July-loading onward. Chinese refiners, for instance, requested only 12 mb of July-loading Saudi crude, compared with an average of 44 mb in 2025.

That said, with refiners bound by term contracts, their appetite for spot cargoes is likely to remain capped, particularly for prompt-loading barrels, as most have already secured feedstock requirements for August arrivals and, in some cases, part of their September arrivals.

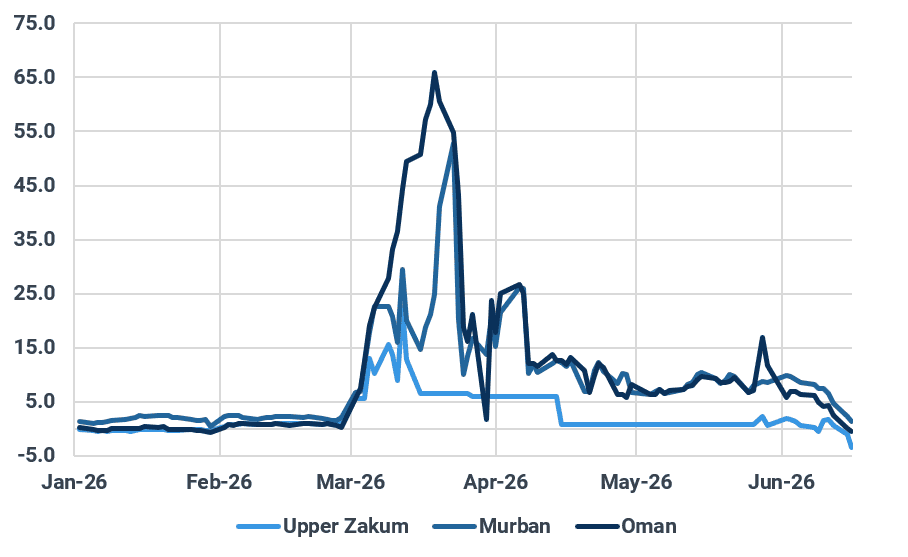

As a result, the Dubai M1-M3 spread narrowed to $1.6/bbl on Tuesday, down from around $6/bbl just last week and an average of $7.4/bbl in May, according to Argus data. Upper Zakum differentials fell to -$3.5/bbl against Dubai swaps, their lowest level since at least 2021, while Murban premiums dropped to $1.4/bbl from an average of $8.2/bbl last month and are now below the $2.1/bbl recorded in February.

Diffs of Upper Zakum, Murban and Oman against Dubai, $/bbl

Source: Kpler

The sudden increase in Persian Gulf crude supply raises concerns over whether demand recovery can keep pace. Our estimates suggest that refinery runs in Asia ex-China have recovered to around 90% of pre-war levels in June and are expected to rise only marginally to 93% by August.

That said, product cracks remain robust on the back of peak summer demand and a slow recovery in Middle Eastern refined product exports. Against this backdrop, Asian refiners (ex-China) retain incentives to further increase oil processing, potentially boosting crude buying demand by 1 mbd to reach their pre-war levels.

Indeed, countries will need to refill depleted inventories, with ex-China stockpiles in Asia-Pacific having drawn by 78 mb over March-May. However, as replenishment decisions take time and replacement volumes are likely to return only gradually at some 150 kbd—judging by the restocking patterns seen in 2022-2023—this demand is unlikely to translate into immediate buying capable of easing the imminent oversupply.

That leaves the question of China, where refinery crude intake remains 2.6 mbd below pre-war levels while onshore crude inventory remains largely untouched. As discussed in previous reports, the absence of Chinese buying demand has been a key factor in maintaining a relatively balanced market and preventing oil prices from rising even further.

Refining margins are expected to improve significantly if crude prices remain around $80/bbl, easing some of the financial pressure on refiners. However, this may not be sufficient to incentivise a meaningful increase in crude procurement or refinery runs, given that domestic gasoline and diesel inventories remain elevated.

Unless Beijing relaxes restrictions on product exports and/or proceeds with another round of SPR refilling, which some market participants said had been planned prior to the war, Chinese refiners are unlikely to have strong incentives to buy crude in large volumes, especially in light of the recent slide in flat prices, as we are yet to see a floor. Moreover, as discussed above, Middle Eastern producers are expected to require Chinese buyers to fulfil their term commitments, further limiting appetite for spot cargoes.

That said, a sharp correction in prompt Dubai prices appears inevitable, even as oil flows through the Strait of Hormuz resume only gradually. Meanwhile, if the US proceeds with its previously planned SPR releases, still-elevated exports from the West of Suez would coincide with the return of Persian Gulf supplies, further weighing on the Dubai market and raising the risk of a brief move into contango.

Saudi crude allocations to China, mb; Arab Light OSPs (vs Oman/Dubai avg), $/bbl

Source: Saudi Aramco, Kpler

Market insights you can trust

Kpler delivers unbiased, expert-driven intelligence that helps you stay ahead of supply, demand, and market shifts.

Trade smarter. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler

![[UPDATE] Middle Eastern supply recovery postponed to early 2027](https://cdn.prod.website-files.com/65059ad784ac02253c62356c/6a69e80d78fefee5dd2f73d6_pipe_line_conection_in_oil_refinery_2_optimized_350.jpeg)