November 4, 2025

How is the US-China trade truce shaping the dry bulk markets?

Iron Ore & Steel: Iron ore prices react to trade optimism, defying weak fundamentals

- Iron ore prices have surged over the past week, buoyed by optimism about trade talks between China and the US, shrugging off weak fundamentals. The most-traded iron ore contract on DCE, January 2026, rose 3.28% w/w to 802.50 yuan/t ($112.87/t) on 30 October. Meanwhile, the SGX TSI 62% Fe second-month contract dropped slightly on 30 October due to the absence of a comprehensive deal following the Trump-Xi meeting, but remained up 2.20% w/w to $106.50/t at the time of writing.

- Global seaborne iron ore exports remain robust compared to seasonal norms, reaching 34.40 Mt in the week ending 26 September, higher than the year-ago level of 32 Mt and the five-year average of 31.10 Mt. Brazilian shipments reached a two-month high of 9.45 Mt following below seasonal average rainfall, while Australian loadings still rose 2% y/y, despite FMG exports dropping to a two-month low on maintenance works.

- While BHP’s overall exports held steady at 5.40 Mt, its Jimblebar Fines continue to fall out of favour amid protracted contract negotiations with Chinese buyers. Kpler data show that shipments of the grade, under boycott by CMRG-led buyers since September, dropped to just 0.72 Mt last week, the second-lowest in seven months. Forward indicators suggest Jimblebar Fines may remain below 0.80 Mt for a third straight week, a run last seen during March 2024.

- Elsewhere in Australia, Mount Gibson has confirmed the closure of its Koolan Island operation following a rockfall on 16 October, although no injuries or deaths were reported. Initially scheduled to be shut down around September 2026, the Koolan Island operations have long struggled with depleting reserves, shipping only 2.61 Mt of iron ore in the fiscal year ending June 2025, down from 4.11 Mt a year earlier. The decision to end the operations appears timely, as expected lower iron ore prices after Simandou’s commissioning will add more earnings pressure on the project, which has much higher unit costs than the top miners in Australia.

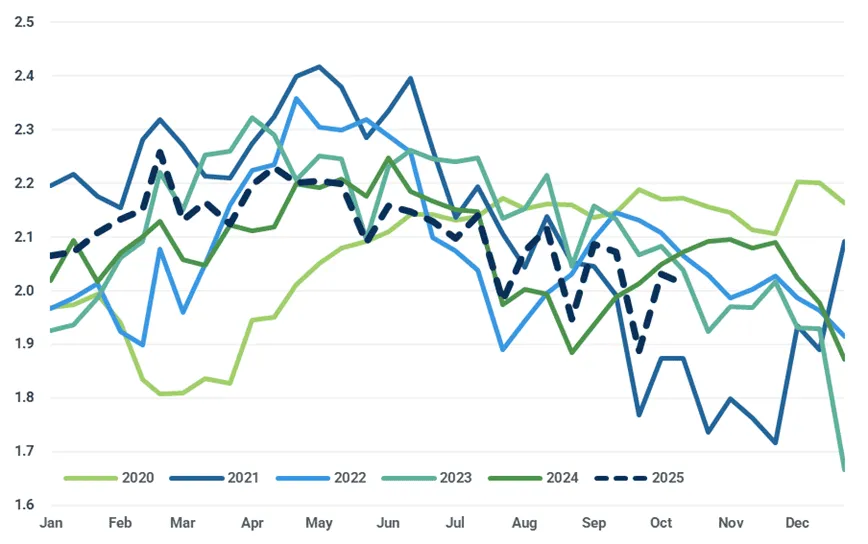

- On the demand front, China’s seaborne iron ore imports totalled 25 Mt last week, slightly below the five-year average of 25.20 Mt. The seasonal decline in domestic steel production continues, with output by CISA member mills averaging 2.01 Mt in the ten days 11 to 20 October, dropping 2.85% m/m and 2.80% y/y. Stockpiles at port increased for a fourth consecutive week, with the inventories of iron ore lump reaching their highest level since March, reflecting tepid demand for high-grade feedstocks and pushing lump premiums to an 11-month low.

Crude steel production by CISA member mills (Mt)

Source: CISA, Kpler Insight

Coal: European coal prices strengthen as oversupply eases

- European coal prices rose as excess supply eased amid higher Asia-Pacific shipments. South Korea is due to receive about 1 Mt of coal from Colombia next month, according to Kpler projections. This will displace Russian supply, which has recently increased its share in South Korea’s import mix.

- German coal burn remained below 2024 levels in October owing to strong renewable performance, but output exceeded seasonal levels on low renewable days, suggesting coal generation may have room to grow in the coming months.

Germany coal-fired generation (GW)

Source: Entso-E

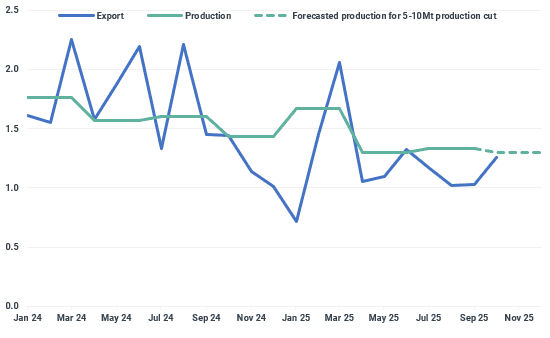

- Glencore raised its 2025 thermal coal production guidance to 92–97 Mt, up from 90–96 Mt. The company expects stronger output from Australian operations and improved logistics at Cerrejón in Colombia. Shipments from Cerrejón are now aligned with production after a period during which exports were below output.

Puerto Bolivar shipments vs Cerrejón production (Mt)

Source: Glencore, Kpler

- China’s thermal power generation dropped 5.4% y/y in September, ending four months of growth as cooler weather reduced power use and hydropower output recovered. The Daqin railway completed its annual maintenance ahead of schedule on 25 October, lifting daily transport capacity above 1.2 Mt.

- China’s metallurgical coal import appetite is strengthening, with most grades reaching new highs this year and cumulative gains of 30–100 yuan/t since October. Efforts to cut down supply are boosting demand for met coal imports, which are projected to reach a multi-month high according to Kpler data.

Grains & Oilseeds: US-China trade meeting leads to Chinese soybean commitment

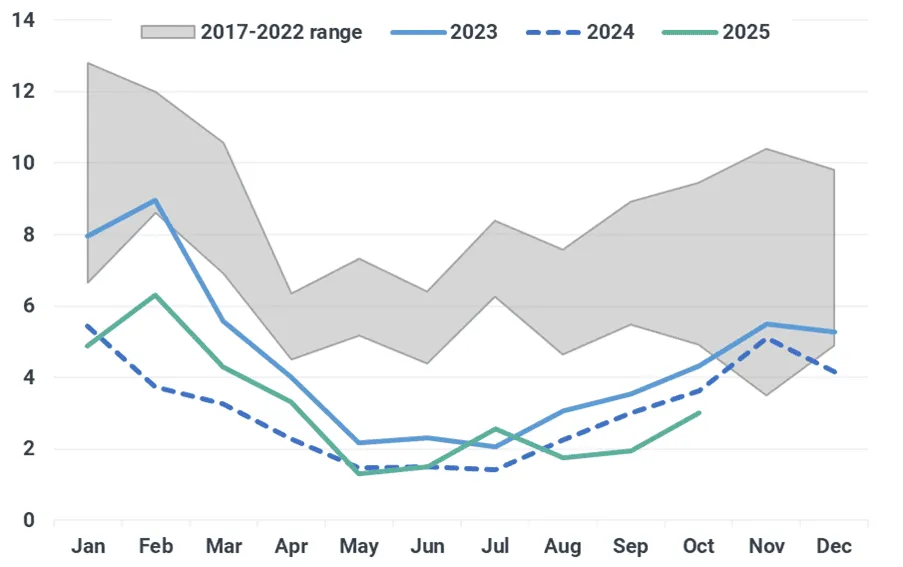

- Soybean futures rallied early in the week as US-China trade sentiment improved. The market was optimistic that a deal would be reached in the meeting between the two presidents, and Chinese companies had started purchasing US soybeans, according to reports early in the week. A few hours after the meeting had been adjourned, US Treasury Secretary Scott Bessent announced that China has agreed to purchase 12 Mt of soybeans this season, with sales occurring now until January. Additionally, Bessent said that China should purchase at least 25 Mt of soybeans annually for the next three years. Bessent also stated that the US has signed trade agreements with other countries in Southeast Asia and the rest of the world, totalling 19 Mt of soybean exports, but did not provide a timeframe regarding this.

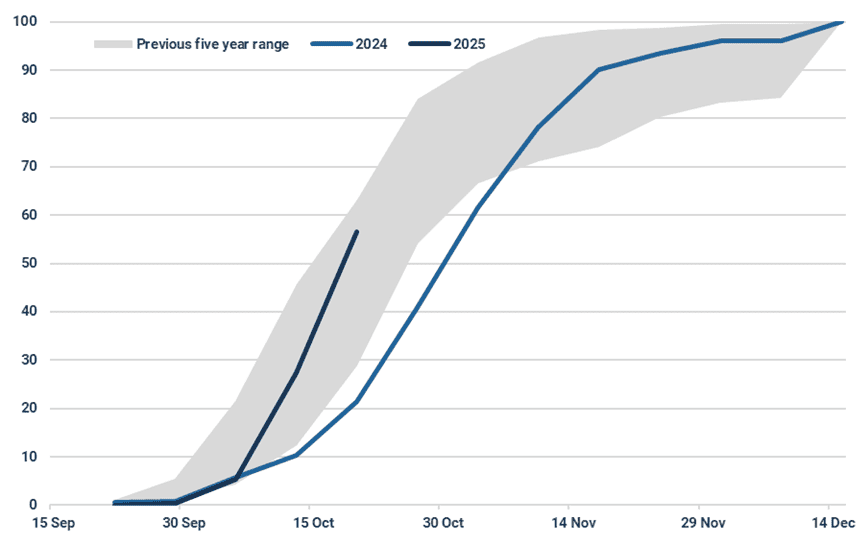

Chinese imports of US soybeans (Mt)

Source: GTT

- Following the strong appreciation in CBOT soybeans, CBOT soybean meal has been lifted to highs not seen since March despite reduced US exports for October. In contrast, CBOT soybean oil has drifted lower, weighed by the precipitous decline seen in Malaysian palm oil. Also, the soybean oil market is waiting for an outcome regarding the reallocation of renewable fuel that had not been blended under the Small Refinery Exemptions. As a result, oilshare has dropped to its lowest since June.

CBOT Dec-25 oilshare and board crush

Source: CBOT, MarketView

- Soybean planting in Brazil reached 34% complete by 25 Oct, in line with last year’s pace but slightly behind the five-year average. Current weather conditions remain favourable for planting of the soybean crop across all key regions. In Argentina, planting of the corn crop is 34% complete by 22 Oct, ahead of both last year and the historical average. Agronomically, there are reports of some dryness in the north and wet conditions in the south, but the vast majority of the Argentine corn crop is developing under favourable moisture conditions. Planting of the soybean crop should begin in the coming weeks.

- The European Commission (EC) tweaked EU corn yield slightly lower to 6.8 t/ha as the crop struggled to recover from drought conditions seen across several key producing member states in the lead up to harvest. For the winter wheat planting campaign, conditions are broadly favourable across western and central Europe but there are challenges in the east. Planting of the French winter wheat crop was 57% complete by 20 Oct, up 14 percentage points from the five-year average. French wheat exports remain stronger y/y following firmer demand from Morocco, which has suffered a consecutive year of poor production due to drought conditions.

French winter wheat planting progression (% complete)

Source: FranceAgriMer

- The EC has proposed that the European Union Deforestation Regulation (EUDR) would be delayed to the end of 2026 for small companies and a six-month grace period at the start of 2026 for all other companies. During the grace period, companies that do not conform with EUDR would not be penalised and would instead be advised on how to conform. This contrasts with the previous proposal in September to delay implementation by another year for all companies. The European Parliament is due to meet next week which may lead to further detail regarding EUDR. The EC has until mid-December to agree on its implementation.

- ICYMI: Kpler hosted its monthly Grains webinar for October, Navigating agricultural markets without USDA data: Trading though the government shutdown. The next webinar is scheduled for 18 Nov.

Minor Bulks: More aluminium smelters face power supply issues

- The future of the Tomago aluminium smelter (capacity: 0.60 Mtpa) in New South Wales, majority-owned by Rio Tinto (51.55% interest), has come under fresh scrutiny following the operator’s admission on 28 October that it has yet to secure a viable long-term energy solution beyond 2028. The development echoes challenges at Bell Bay Aluminium in Tasmania (capacity: 0.19 Mtpa, 100% Rio Tinto-owned), which remains without a power supply agreement for operations after 2025, despite 18 months of negotiations. Combined with the risk of closure at the Mozal smelter in Mozambique after March 2026 due to the difficulties of obtaining an affordable electricity supply, these cases highlight the growing global risks facing the aluminium industry, where rising energy costs threaten the commercial viability of power-intensive smelting operations. As a result, the global aluminium supply-demand balance is expected to tighten further.

- Meanwhile, oversupply concerns continue to weigh heavily on the alumina market. The most actively traded SHFE contract, January 2026, closed down 0.78% w/w at 2,816 yuan/t ($396.06/t) on 30 October. Despite minor supply disruptions, including brief production curbs in northern China linked to anti-pollution efforts, abundant inventories and high operating rates have suppressed any price recovery.

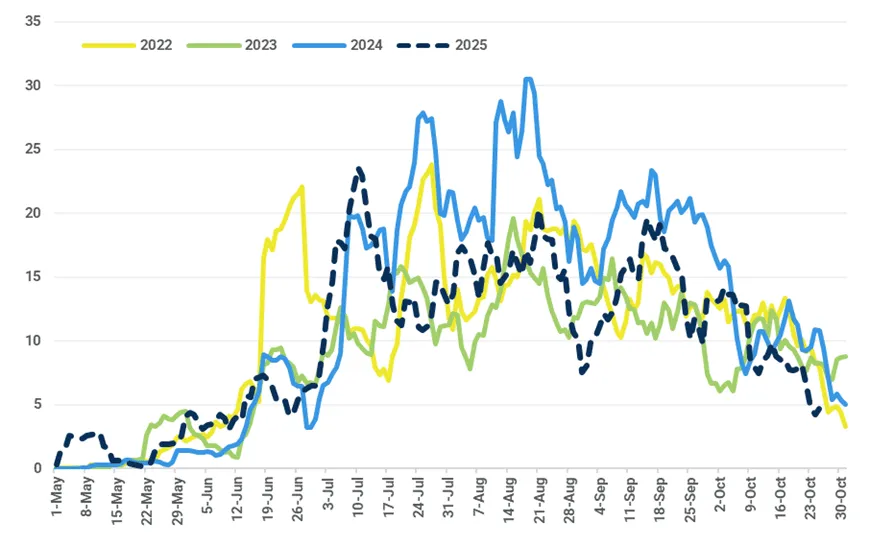

- Bauxite supply also remains ample. Port inventories in China are sitting at multi-year highs, while Guinean exports are expected to accelerate into November. Precipitation levels in Boké, Guinea’s bauxite mining heartland, have declined sharply in recent weeks, signalling the imminent end of the rainy season and paving the way for stronger outbound flows.

10-day moving average precipitation in Boké, Guinea (Mt)

Source: Meteostat, Kpler Insight

Dry Bulk Freight: Suspended US-China port fees mean lower fleet inefficiencies

- Neither the US nor China will be implementing reciprocal port fees as both countries agreed to a one-year truce, following the US-China meeting in South Korea on 30 October. Chinese port fees on US-linked tonnage would have resulted in increased fleet inefficiencies in terms of ballast voyage and port durations, as owners redeploy tonnage to avoid paying extra charges. Following the suspension, the overall effect of this will be a relief of pressure on vessel supply in the market.

- Vessel waiting times at Chinese ports, as implied by several market reports, will likely follow a downturn with rising Pacific ballast supply across fleet segments.

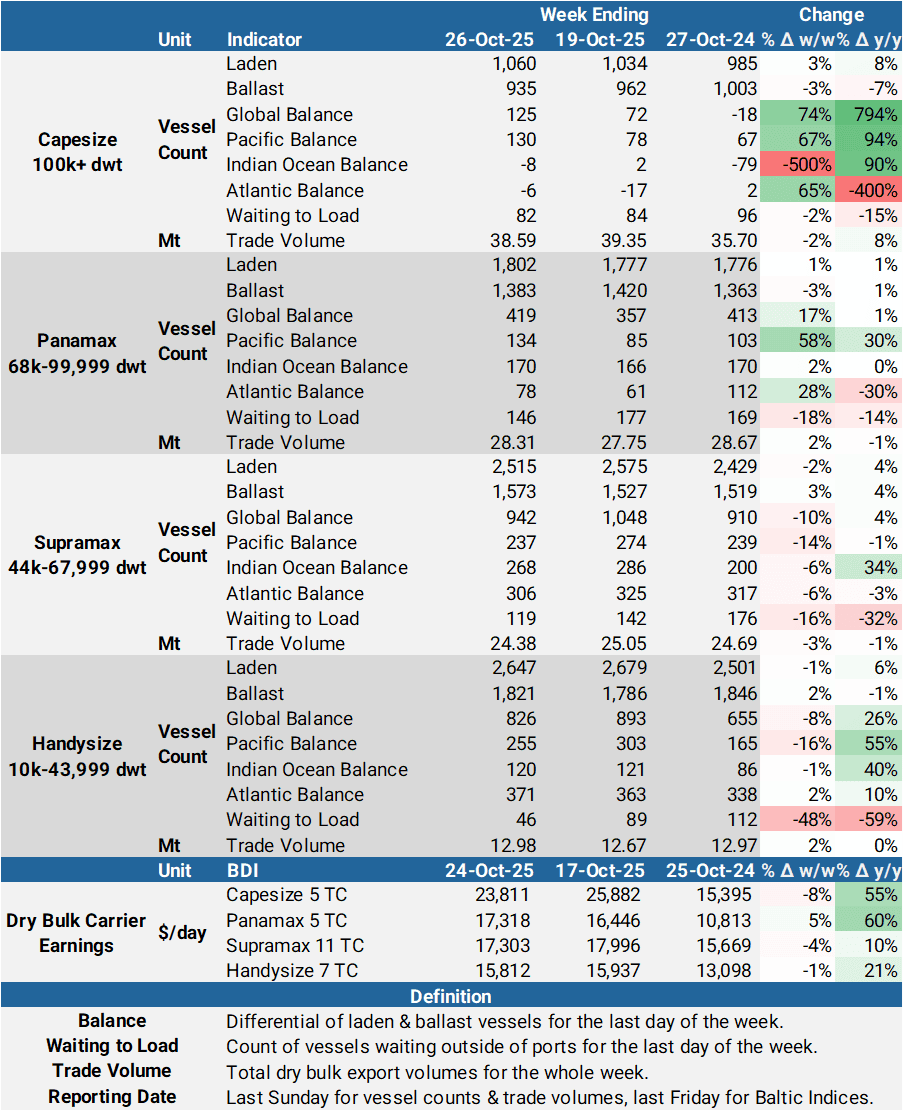

- The Capesize 5 TC average retreated to $24,428/day on 30 October (down $939/day w/w), driven by the decline in the Pacific round-voyage rate to $24,250/day (down $4,509/day w/w). An upturn in ballast supply in the Pacific and lower bunker prices also saw the Capesize W.Australia-China iron ore spot voyage rates drop to $9.52/t (down $0.89/t w/w). We expect regional ballast supply to thin in the short term, with firmer fronthaul demand from post-monsoon Guinean bauxite and Brazilian iron ore shipments pulling some tonnage out of the Pacific basin.

- Weakness across both Atlantic and Pacific rates drove the Panamax 5 TC average earnings from a multi-week high of $17,319/day on 23 October to $16,643/day. Weather disruption on the East Coast of Australia delayed vessels scheduled to load coal at Australian ports, where lineups point to lower exports during the week following 27 October. However, we do not expect meaningful support to Panamax earnings from recently higher port congestion, with elevated Pacific Panamax ballast supply of 786 vessels (up 8% both on the week and a year-ago) negating any supply tightness.

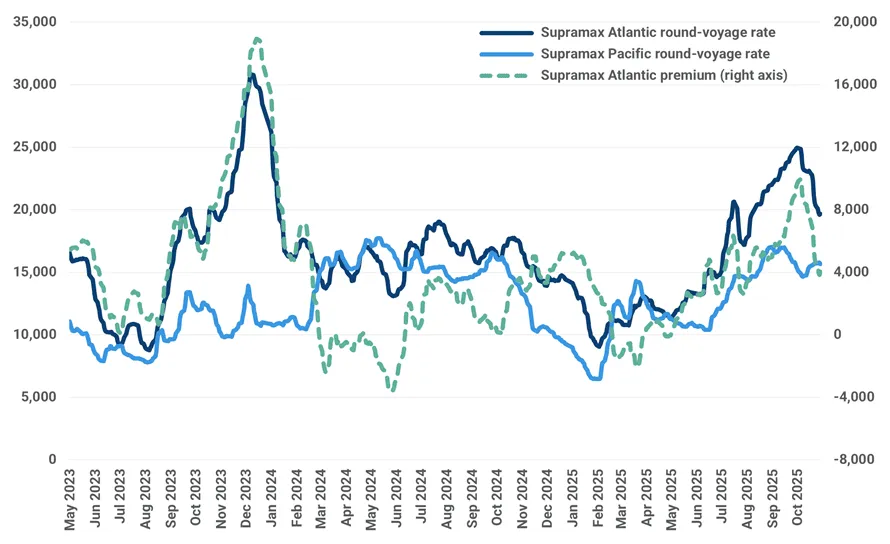

- The Supramax 11 TC average dropped to a multi-week low of $16,890/day, down $533/day w/w due to softer rates on both basins. North Atlantic demand lacks the seasonal push in fronthaul US soybean shipments, leading to downward pressure on US Gulf routes. We expect the Supramax Atlantic RV (average S4A & S4B) premium to the Pacific equivalent to retreat sharply from the current $4,025/day and be lower than November 2024’s average of $3,747/day. Token Chinese purchases of US soybeans are too small and come too late to move the dial for the fourth quarter freight market significantly. With weak Atlantic earnings discouraging vessels from switching basins, we expect more Supramaxes competing for Indonesian coal shipments during the seasonal Chinese pre-winter coal stockpiling.

- Additionally, the Handysize 7 TC average earnings retreated to a multi-week low of $15,382/day, down $465/day w/w, driven by softer Atlantic earnings.

Counter-seasonal to previous years, Supramax Atlantic earnings declined sharply ($/day)

Source: Baltic Exchange

Key Dry Bulk Market Developments

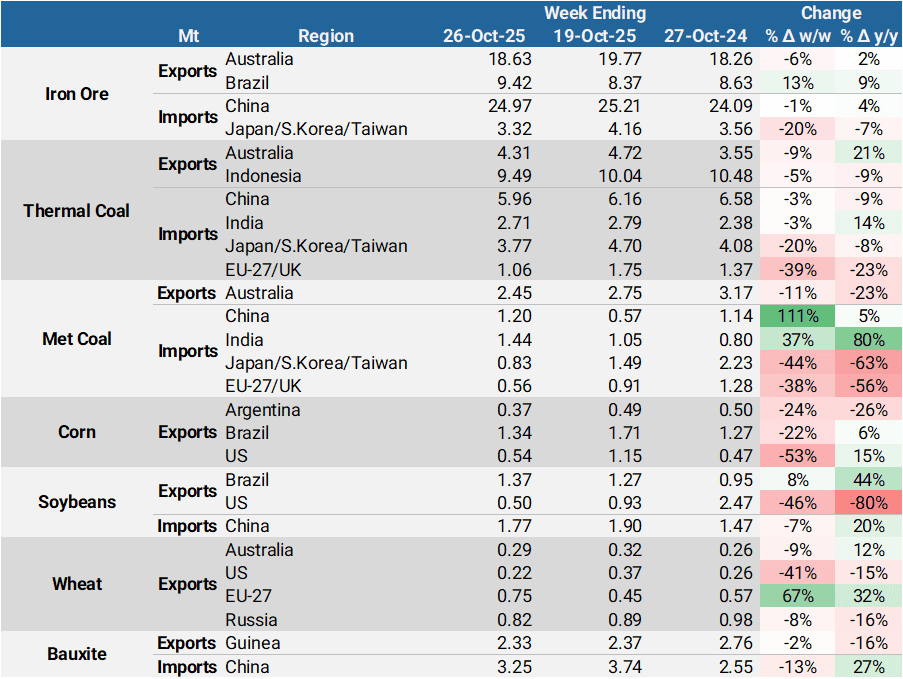

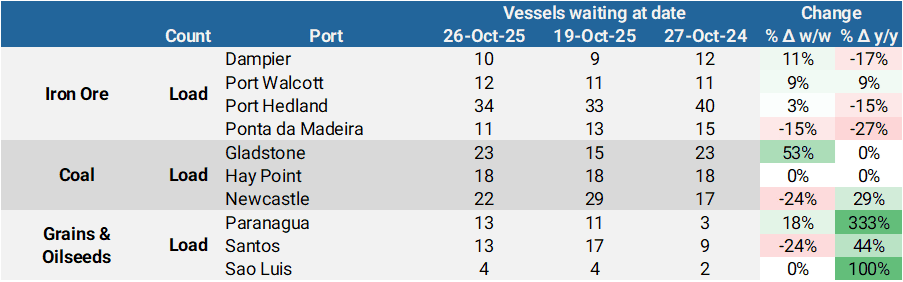

Dry Bulk Commodity Flows

Source: Kpler

Dry Bulk Port Congestion

Source: Kpler

Dry Bulk Freight Metrics

Source: Kpler, Baltic Exchange

New: Kpler Dry Bulks Insight is here

Gain instant clarity on dry bulk flows, rates and fundamentals with real-time AIS tracking and proprietary supply-demand models. Our experts deliver weekly reports, monthly commodity deep-dives and exclusive webinars spotting emerging trends and market imbalances. Ready to navigate shifts with precision and confidence?

See why the most successful traders and shipping experts use Kpler

Request a demo

Ready to navigate dry bulk shifts with precision and confidence?

Request trial access