Iran begins exporting crude from Jask, bypassing the Strait of Hormuz

Executive Summary

Atlantic Basin: The Atlantic Basin has now fully recovered from the impacts of recent hurricanes, however Mexico’s internal woes are pushing multi-month high volumes of crude to the export markets. Meanwhile, Nigeria has switched to an all-Nigerian slate and even its term US WTI barrels are not finding their way to the Dangote refinery.

Europe and FSU: After pressured operations at Libya’s Zawia refinery drove a record high in product imports last month, news emerged this week that the plant has come back online. In the meantime, the resumption of Libyan oil supply has enabled crude exports to rebound from 450 kbd in September to 640 kbd over H1 October, weighing on CPC Blend differentials.

Middle East and Asia: Iran’s oil exports quickly rebounded after a brief slowdown while the first-ever crude load from its Jask terminal, bypassing the Strait of Hormuz, marks a significant development. Meanwhile, Iraq has improved its OPEC+ compliance. Light sweet crude differentials will face pressure due to refinery outages in Asia and rising US production.

Atlantic Basin: Dangote moves into ‘full Nigeria’ mode as it shuns US term barrels

The Nymex WTI futures contract has not been seesawing as much as Brent was, largely because the Libya oil embargo and the risks of other supply disruptions impacted it less, resulting a stagnant picture for time spreads. The WTI M1-M2 spread hovered around $0.50/bbl at the beginning of October, it remains there at the time of writing as well. On the other hand, there have been developments within US benchmarks, most notably the premium of WTI Houston over Nymex WTI narrowed back to $1/bbl, well below the 2024 to-date average of $1.65/bbl. Concurrently, the ICE Brent-WTI spread widened again above $4/bbl, effectively returning where it was in early September after mostly trending around $3/bbl over the past four weeks. In line with this, WTI Midland has become twice the cheapest grade in the BFOETM basket, the first time this has happened since the first decade of September, ending one of the longest streaks when WTI managed to avoid wielding an inferior differential to Brent.

WTI time spreads, $/bbl.

Source: Argus Media.

Mexican crude exports have recovered after Hurricane Milton, passing through the Yucatan peninsula, forced the country’s main export terminal to temporarily shut down. In fact, the pace of exports is the strongest since February 2024, averaging 975 kbd at the time of writing. This might very well be a consequence of Pemex’s downstream woes – whilst the Deer Park debacle that killed two contract workers has been widely discussed, an earlier incident at the 330 kbd Salina Cruz seems to have disrupted the Mexican NOC’s modus operandi. Salina Cruz registered the highest throughput rates in Mexico for several consecutive months, usually running around 65-70%, and the loss of those 230-240 kbd refinery runs could very well explain the 200 kbd m/m increase in the country’s crude exports. Pemex has been in the news recently as leaked internal documents indicate that the company’s new head of upstream Nestor Martinez ordered that upstream expenditures be cut by 20% in Q4 2024, aiming to save some $1.5 billion by doing so. Our expectation is for Mexican crude and condensate supply to dip to 1.8 Mbd by the end of the year, some 30 kbd lower than it is currently, exceeding the 5-6 kbd impact that Pemex’s internal documents seem to suggest.

Mexico's annual average crude and condensate supply in 2010-2026, kbd.

Source: Kpler.

Across the Atlantic, Dangote has now moved into a much-anticipated period of exclusively Nigerian feedstocks coming to the refinery, to the extent that even the one-year term deal that the company signed for regular monthly WTI deliveries now seems to be resold on the market. In September, there was not a single non-Nigerian cargo arriving to Dangote and October should continue that trend with no foreseeable cross-Atlantic deliveries. In a similar vein, the oft-quoted Tupi delivery from Brazil did not take place either, the cargo was resold even before it was loaded. It needs to be pointed out that the overall volumes coming to Dangote averaged around 200 kbd over the past two months, indicating lower overall throughput rates, with October deliveries sticking to a similar pace. The normalization of operations will become an overarching narrative for Nigeria’s key downstream asset – a refinery that was configured to run on Forcados and Escravos has at last moved to run exactly those grades. In September, the two medium sweet flagship grades of Nigeria accounted for 55% of all imports, with the rest filled up by Brass River, Okwuibome and Amenam. Attesting to Dangote’s breakthrough in secondary utilization, not a single grade from the abovementioned ones is lighter than 40° API.

Share of Nigerian grades imported to Dangote and total volume of imports, % and kbd.

Source: Kpler.

Higher domestic demand has failed to stop the decline in Nigerian differentials as both Forcados and Escravos slid some $2.5/bbl over the past two months, currently trending slightly above a $1/bbl premium to Dated on a free-on-board basis. As we have indicated previously, the Atlantic Basin is undergoing a wide-ranging recalibration of how medium-density barrels are priced and Nigerian barrels are no exception to that rule, every producer in the region has been adversely impacted by the continuous low buying activity. However, we believe the downside for Nigerian grades is very limited and most probably they would trend around similar levels as they do currently, mostly due to the Dangote effect. In contrast to this, we would expect Angolan grades to dip lower, with Dalia and Mostarda trading at discounts of -$1 and -$2/bbl vs Dated, respectively, whilst Cabinda is nearing Dated parity on a FOB basis. Angola’s loading programme for December sees 3 more cargoes than the 33 shipments in November, taking the total volume to 1.1 Mbd, up 50 kbd compared to the November plan. With Chinese demand for Angolan barrels relatively rangebound at 600 kbd and unlikely to edge higher than that anytime soon, further downward correction should be expected.

Angolan differentials vs Dated, $/bbl.

Source: Argus Media.

Europe and FSU: Libyan crude supply and refining capacity returns as outages are resolved

The most recent dispute between Libya’s rival eastern and western factions pressured the country’s production from usual levels of 1.2 Mbd to 880 kbd in August and 660 kbd in September. As a consequence, last month's exports fell to a mere 450 kbd, with most of these volumes departing from the Marsa al Hariga and Zueitina ports amid stable Sarir/Mesla output.

In late September, Naji Mohamed Issa Belqasem was approved as a new central bank governor, the nation’s eastern government lifted the force majeure order on 3 October. This enabled all fields and export terminals to resume in the following days, including production from the 300 kbd El Sharara field (which had been offline since early August). By 8 October, the Al Jurf, Bouri, Brega, Mellitah, and El Sharara fields were producing at full levels, with only output at Es Sider, Amna, Sirtica and Bu Attifel still pressured. After a two-month hiatus, exports of El Sharara have resumed, with the Diamondway departing the Zawia port on 16 October and bound to arrive in Le Havre on 24 October.

Libyan crude and condensate supply recovered to above 1 Mbd over the first week of October and drove a recovery in the country’s crude exports to 640 kbd over the first half of this month. The re-start of production prompted us to adapt our supply estimates higher, with this month’s output averaging 1 Mbd and expected to rise to 1.15-1.2 Mbd in November and December. Crude exports should reach average levels above 850 kbd in October before growing to normal levels of 1 Mbd next month. These estimates are corroborated by the October loading schedule, which has been revised to 888 kbd for this month.

Libya crude and condensate supply outlook, kbd

Source: Kpler

Recent developments have also seen operations return in Libya’s downstream sector. While in September technical maintenance was planned for CDU 1 at the country’s main refinery, the 120 kbd Zawia plant, CDU 2 also went offline last month due to an electrical fault. This halved the country’s refining capacity to only around 30-40 kbd in September and early October. On Tuesday, news emerged that Libya's Zawiya refinery was back online, enabling the resumption of product supply. Zawiya runs on light sweet crude, primarily from the El Sharara and El Feel fields, and produces mainly gasoline, diesel and residual fuel for domestic consumption. Pressured refinery runs drove a record high in product imports to the country at 310 kbd in September, made up of 135 kbd of gasoline 135 kbd of gasoil/diesel from Russia and the Med (Italy, Cyprus, Greece), 30 kbd of naphtha from Russia and 6 kbd of fuel oil from Europe.

Refined product imports to Libya, kbd

Source: Kpler

Despite tight supply caused by Kazakhstan's production cuts during ongoing maintenance at the Kashagan field, the return of Libyan barrels has caused CPC Blend differentials to trend lower. Over the past week, CPC Blend differentials trended at -$4.4/bbl against North Sea Dated, marking a $1 drop from last month's average. While Libyan exports to the Mediterranean remain low with only four shipments so far this month, they are expected to rise as production ramps up towards pre-blockade levels.

Meanwhile, CPC Blend shipments have stayed relatively strong, with key Mediterranean markets like Italy, Greece, and France continuing to receive higher volumes. Kazakhstan’s maintenance at the 465 kbd Kashagan field, which began on 7 October and is set to last 30 days, is part of its strategy to reduce production in line with OPEC+ quotas, curtailing Kazakhstan crude and condensate supply to 1.67 Mbd in October.

Middle East and Asia: Iran begins exporting crude from Jask, bypassing the Strait of Hormuz

Oil prices eased this week as the threat of an Israeli strike on Iranian oil facilities diminished, with Iran quickly resuming exports to 1.3 Mbd after a brief slowdown. The first-ever crude load from Iran's Jask terminal, bypassing the Strait of Hormuz, marked a significant development. Meanwhile, Saudi Arabia and the UAE have increased exports through alternate routes, while Iraq improved its OPEC+ compliance despite overstated claims of Kurdish output cuts. Light sweet crude differentials face pressure due to refinery outages in Asia and rising US production, which is set to reach new highs.

Oil prices have retreated this week as the likelihood of an Israeli strike on Iranian oil facilities diminishes. The US administration, China, and regional powers like Saudi Arabia and the UAE have reportedly intervened to prevent such an escalation. This aligns with our previous assessment following Iran’s missile launch on Israel, where we argued that retaliation on oil facilities – particularly export-focused installations – was unlikely.

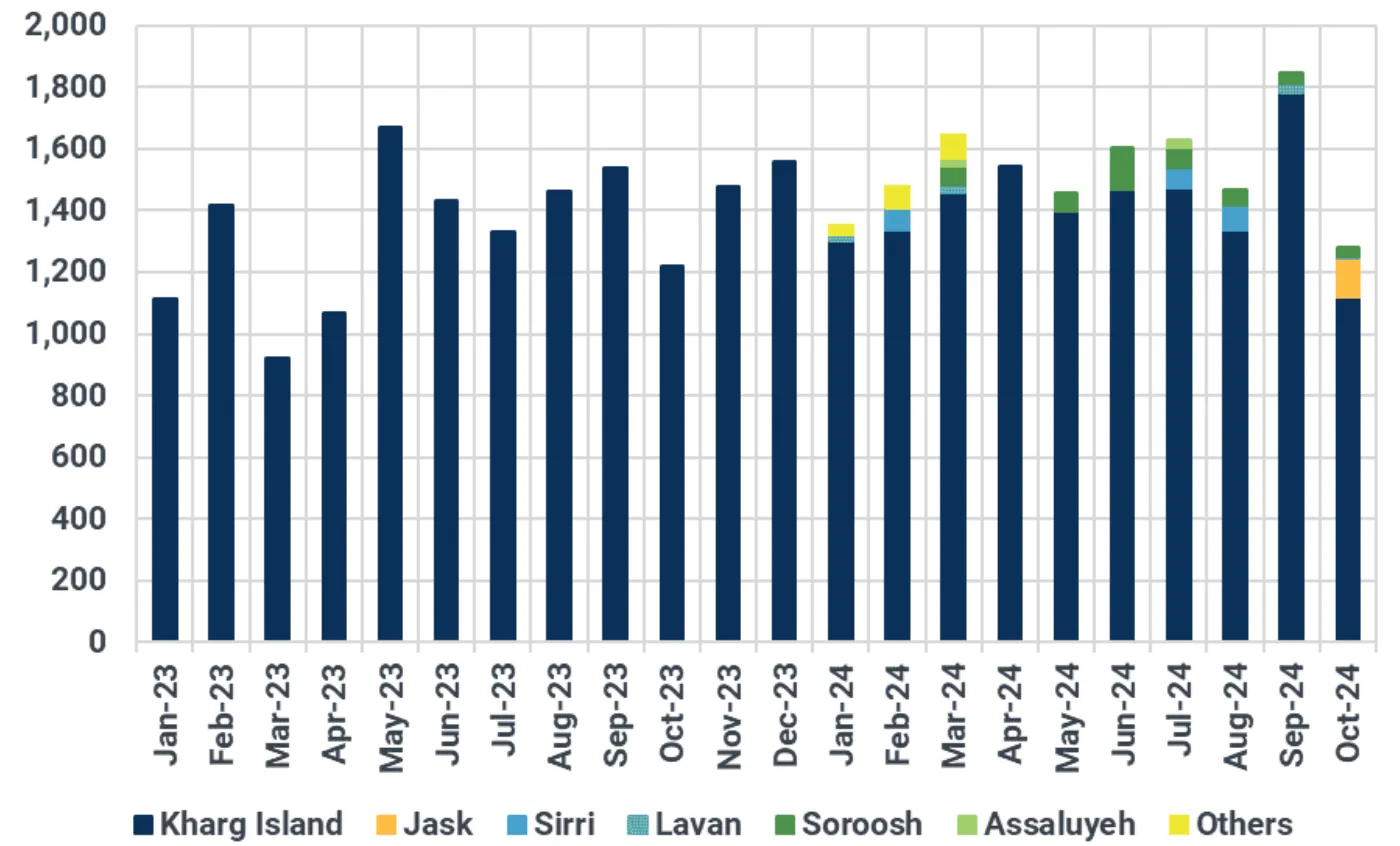

Iran’s oil exports, which had slowed at the beginning of October, possibly in anticipation of a potential Israeli attack, have since rebounded with activity returning to normal levels and exports back to 1.8 Mbd in the past week. Tehran likely received assurances that its oil installations would not be targeted, bolstering its confidence to increase exports. After a brief dip, Iran’s exports have picked up pace, and mtd loadings now average 1.4 Mbd. Although this remains below last month’s record of 1.85 Mbd under US sanctions, it is not far from the yearly average of 1.54 Mbd.

Iran oil exports by origin ports, kbd

Source: Kpler

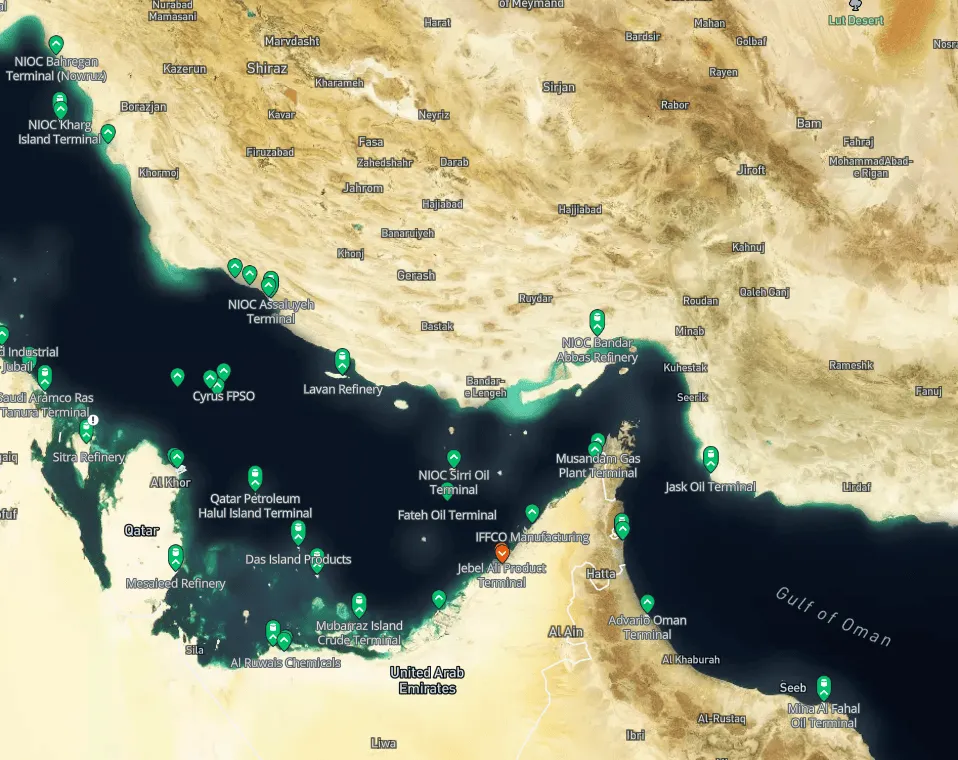

A notable development is the first-ever load from Jask, Iran’s newest oil terminal designed to bypass the Strait of Hormuz. The VLCC Dune loaded 2 Mbbls of crude from Jask in early October, which we estimate occurred on 2nd October , just one day after Iran’s strikes on Israel. While the terminal was inaugurated in 2021, it remains partially under construction. Currently, 10 operational storage tanks provide a total capacity of 5 Mbbls, with another 10 tanks expected to come online in the coming months, doubling storage capacity. Out of the terminal’s projected 1 Mbd pipeline capacity, which transports crude from the Goureh pumping station in the southwest to Jask in the southeast, we estimate only 500 kbd are operational.

Map of key oil terminals around the Mideast Gulf

Source: Mapbox, Kpler

Beyond Iran, Saudi Arabia and the UAE have also developed infrastructure to bypass the Strait of Hormuz. Saudi Aramco utilises the 5 Mbd East-West Petroline, exporting crude from the Red Sea port of Yanbu. Exports from Yanbu have risen from 572 kbd last year to 863 kbd ytd, enabling Saudi Arabia to avoid the Bab el Mandeb Strait and reduce risks from Houthi drone attacks. Similarly, the UAE uses the Habshan–Fujairah oil pipeline (ADCOP), with a capacity of 1.5 Mbd. Abu Dhabi's crude exports from Fujairah have increased from 813 kbd last year to 1.07 Mbd YTD.

Saudi and UAE crude exports bypassing the Strait of Hormuz, kbd

Source: Kpler

In Iraq, officials have insisted that compliance with OPEC+ cuts has improved, primarily due to a halving of Kurdish output. However, we believe this explanation is overstated. Reports from DNO and Gulf Keystone Petroleum, the two largest foreign operators in the region, show that production in Q3 was rising, including in September. DNO’s Tawke and Peshkabir fields produced a combined 84 kbd in Q3, up from 80 kbd in Q2, while GKP’s Shaykan field increased output from 44 kbd to 49 kbd. Thus, unless all other assets ceased operations in September, which seems unlikely, Kurdish output likely did not halve as claimed.

That said, southern Iraqi oil exports fell by 110 kbd m/m to 3.32 Mbd in September, despite a reduction in crude burn. Crude burn fell to just 46 kbd, down from around 100 kbd in the previous month, as Iraq increased imports of Iranian natural gas and enhanced power grid integration with Jordan and Turkey. We estimate Iraqi crude production stood at 3.99 Mbd, slightly below its OPEC+ quota of 4 Mbd. This marks the first time Iraqi output has fallen below the 4 Mbd threshold since May 2021. The increased compliance provides some support to the Asian medium sour market, which would have otherwise weakened due to rising Russian and Saudi exports.

However, light sweet crude differentials are likely to come under pressure in the coming weeks. Petron’s 80 kbd Port Dickson refinery in Malaysia has entered unscheduled maintenance for eight weeks, reducing demand for light sweet grades such as Murban and Gabon’s Rabi. Additionally, the refinery may resell some of its crude in storage, further pressuring differentials. On the supply side, the upcoming start of Shell’s Whale project in the Gulf of Mexico and the ramp-up of the Matterhorn Express pipeline supporting tight oil production in Texas and New Mexico will push US oil output to new highs of 13.5 Mbd in November and December. The widening WTI-Brent spread will make US crude more attractive to Asian buyers.

Want access to Insights on a regular basis?

Through unbiased, expert-driven research and news, you’ll receive valuable information on supply, demand, and market movements, enabling you to make informed trading and risk management decisions.

Unbiased. Precise. Essential.

Curious? Request access to Kpler Insight today.

See why the most successful traders and shipping experts use Kpler

Get daily expert-driven research through Insight.