Mixed LNG price outlook as TTF faces upside on Norwegian outages, Asian LNG slips on weaker Chinese demand, HH slightly bearish

Market & Trading Calls

European TTF price outlook: Slightly bullish as some uncertainty around Norwegian pipeline flows lingers on and sustained competition with Asia could pull prices upwards

Asian LNG price outlook: Slightly bearish next week as softening demand in China and Thailand outweighs lingering supply risks in Indonesia and Malaysia, though a recent US court ruling could offer limited upside support.

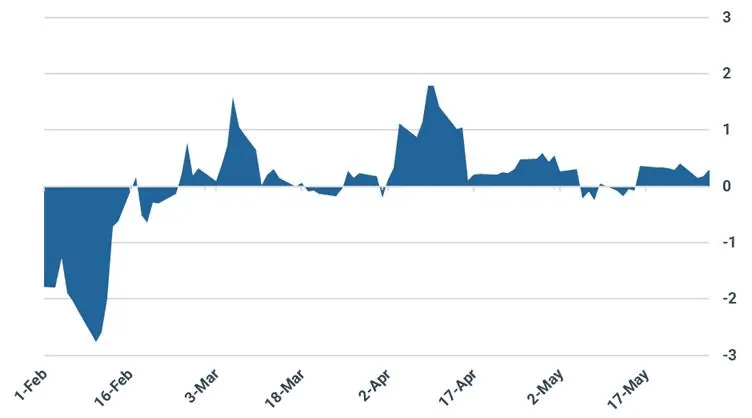

Asian LNG – TTF spread: Narrow with Asian LNG bearish and TTF facing upward pressure next week. As a result, we expect Asian LNG will continue to retain a slight premium over TTF. As of 28 May, the Asian LNG price traded at a $0.30/MMBtu premium to TTF.

US Henry Hub price outlook: Slightly bearish as weak near-term demand, flat production, and robust storage injections put downward pressure on prices. As temperatures warm in the middle of next week, prices could see some upward support, especially if weather models continue to project a hot July.

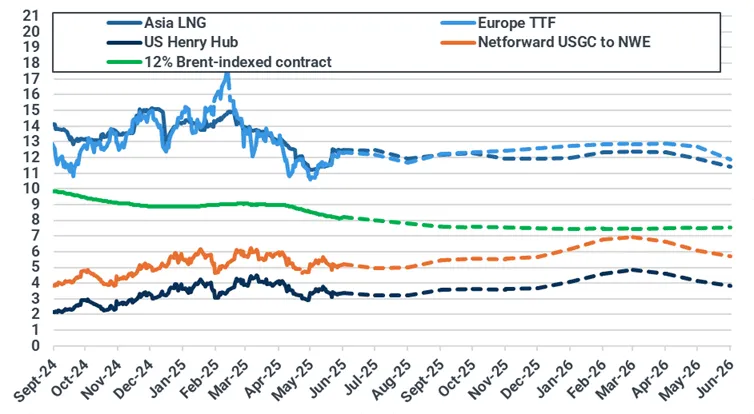

Key natural gas and LNG prices ($/MMBtu)

Source: ICE, NYMEX, Spark Commodities. Brent-indexed price represents 12% slope of 90-day moving average of Brent contract. Netforward USGC to NWE calculation is 115% Henry Hub contract plus shipping and regasification costs into Gate (Spark Commodities).

Asian LNG-TTF spread ($/MMBtu)

Source: ICE, Kpler Insight

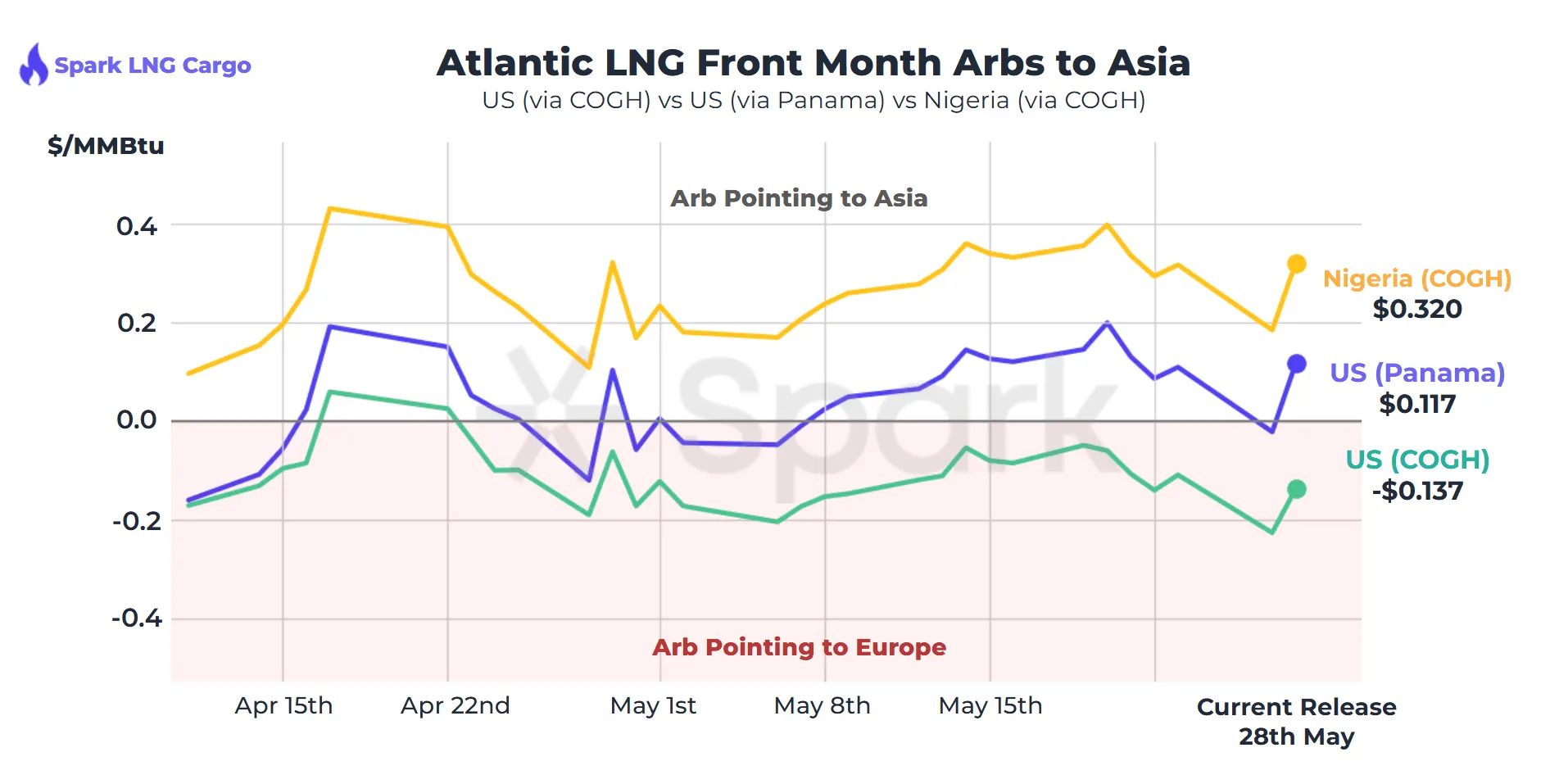

Global LNG front-month arbs ($/MMBtu)

Source: Spark Commodities, incorporating ICE-listed Spark Freight and Spark Cargo products. For a full M+12 forward curve and netback cost breakdown, contact Spark at info@sparkcommodities.com.

Europe: Some bullish pressure after Norwegian maintenance and continued competition with Asia

TTF front-month prices slightly rose compared to last week, settling at $12.2/MMBtu on 28 May – a modest 0.1% ($0.02/MMBtu) increase from 21 May. Market sentiment turned mildly bullish last week, driven by extensive maintenance at Norway’s Troll field, which pushed Norwegian flows to the EU down to just 0.13 mcm/day. Additional uncertainty stemmed from the inconclusive Russia–Ukraine peace talks in Istanbul, compounded by growing perceptions that the US is stepping back from direct involvement in the diplomatic process.

Looking ahead, Kpler Insight expects a modest uptick in TTF prices, underpinned by lingering uncertainty around Norwegian flows. While volumes have partially recovered following the Troll field incident, Gassco has confirmed that the unplanned outage will not be fully resolved until the end of the month. A secondary driver remains ongoing competition with Asia, as the Asia LNG–TTF premium has held near $0.30/MMBtu since mid-May—supported by supply disruptions in the Pacific Basin. This trend is expected to persist into next week, adding further upward pressure to TTF.

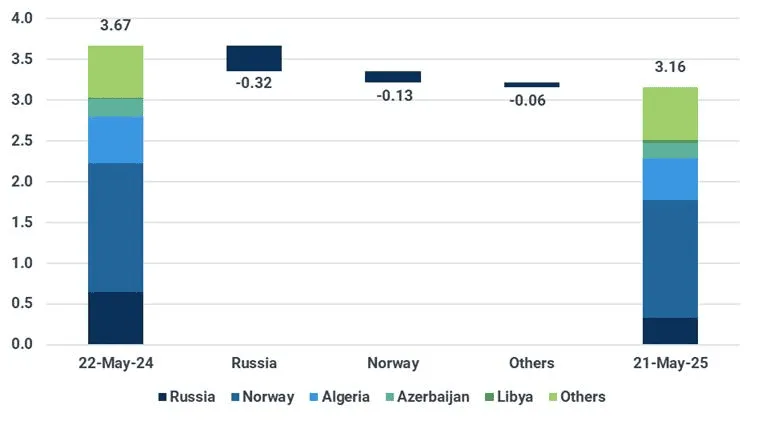

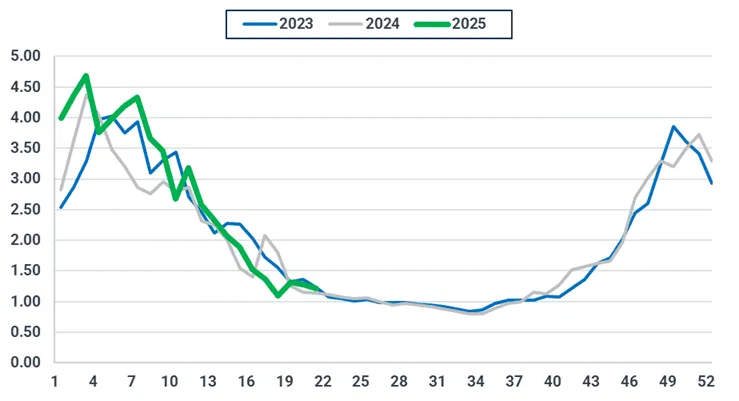

On the fundamentals side, net pipeline flows into the EU declined slightly last week, easing by 9.8% w/w to 3.16 bcm. Turkstream deliveries into Bulgaria held broadly stable, while Algerian flows to Italy dipped marginally due to maintenance. That said, combined Algerian volumes to both Spain and Italy remained relatively steady overall. A standout development was the sharp rise in flows to Ukraine, which averaged 18.8 mcm/d over the past 4 days—the highest since late February. Notably, volumes from Slovakia have surged and are now nearly on par with those from Poland, a trend that is expected to further tighten supply conditions across the CEE region.

EU-27 weekly net pipeline gas imports (bcm), y/y comparison

Source: Kpler Insight. Data represents week commencing 22/05/2024 and 21/05/2025.

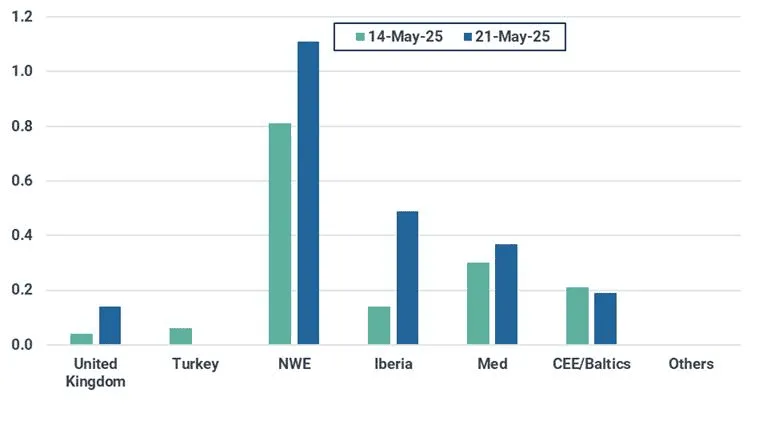

European LNG imports rose to 2.3 mt over the past 7 days (+47% w/w), driven by higher imports into NW Europe, Iberia and the Med. This was still lower than the record arrivals in March/April, and we expect this downwards trend to continue as heavier maintenance continues in Montoir and more maintenance in Dunkerque, Barcelona and Mugardos is set to start next week.

EU-27 weekly LNG imports (mt)

Source: Kpler Insight. Data represents week commencing 14/05 and 21/05/2025.NWE=FR, BEL, NL, GER. Iberia=ESP, POR. Med=ITA, HVR, GRE. Baltics/CEE=FI, LT, POL. Others=SWE, MT.

Local distribution network gas demand across 15 EU countries fell 5.5% w/w to 1.21 bcm, led by warmer weather in Southern and Eastern Europe. While demand should stay near seasonal norms, rising summer temperatures could trigger modest upside risk in the coming weeks.

EU-15 weekly consumption in the local distribution (res/com) sector (bcm)

Source: ENTSOG, ENAGAS, Eurstream, AGCM, Kpler Insight. The EU-15 perimeter includes AT, BE, CZE, FR, HU, GRE, ITA, NL, LUX, POL, POR, ROM, SLVN, SLVK, and SPA.

Average forecast temperatures for selected European countries (°C)

Source: Kpler Power. As of 29 May 00:00 UTC.

Gas-fired generation across the EU-23 declined 10% week-on-week to an estimated 3.3 TWh, as surging wind output displaced gas demand in the power sector. Wind generation jumped 32% w/w to 9.7 TWh, exceeding levels observed in both 2023 and 2024. Looking ahead, warmer weather could provide modest support for gas burn if cooling demand intensifies. However, the scope for any rebound will depend on renewable performance, with current forecasts suggesting elevated wind output will persist into next week.

EU-23 weekly gas-fired generation (TWh)

Source: Kpler Power, Kpler Insight. Excluded EU-27 countries are HR, IE, MT and CY.

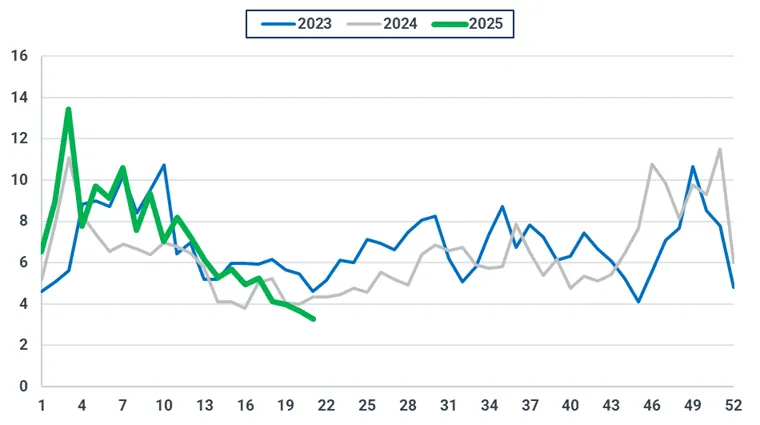

As of 27 May, EU gas storage stood at 46.9% full, rising 1.7 percentage points week-on-week. Injection rates dipped below the 5-year average for 6 consecutive days, as France and Germany drew down stocks in response to the Norwegian supply outage—on some days, withdrawals even exceeded injections. Despite this temporary disruption, current price levels remain well below those seen in December, and injection activity is expected to return in line with the 5-year seasonal trend in the coming weeks.

EU-27 cumulative gas storage injections (bcm)

Source: GIE, Kpler Insight. Latest date as of 27/05/25.

Want the complete report?

The full report is available within Insight and contains:

- Market & Trading Calls

- Europe: Some bullish pressure after Norwegian maintenance and continued competition with Asia

- Asia: Weaker Demand in China and Thailand Offsets Supply Risks

- US: Henry Hub Slumps on June Contract Expiry: Near-Term Bearish, But July Heat Could Offer Support

- LNG Supply: Pacific supply set to gradually recover as NWS and Bintulu increase exports; Indonesia underperformance poses downside risk

Stay ahead of the curve with up-to-the-minute news and forward-looking views on market-moving developments covering LNG, European natural gas and US natural gas markets. Get daily LNG reports and understand the interplay between natural gas, LNG, and coal including supply and demand fundamentals.

Unbiased. Data-driven. Essential.

Trade smarter. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler

Expert research & analysis driven by proprietary data