Refined Products Weekly: China’s 4% export VAT to support Singapore ULSD cracks

Light Ends:

- Bearish near-term sentiment for East of Suez naphtha cracks as waning cracking demand persists. Outlook improves from mid-December as demand strengthens on the back of cracker ramp-ups.

- In the West of Suez, we are moderately bearish in the short term as blending and cracking demand support cracks, but the E/W spread will widen from December due to softening Atlantic Basin fundamentals.

- Key Trade Insight: Favor short positions in Asian naphtha markets in the near term while monitoring signs of recovery from mid-December. Long opportunities in E/W spreads could emerge next month.

Gasoline:

- Sentiment to shift quickly on US gasoline: Expect lengthening balances and pressure on cracks post-Thanksgiving.

- Bearish on European cracks: While export demand has improved this month, Atlantic Basin length will keep weighing down the regional market.

- Moderately bullish on Singapore cracks through Q4: Wider regional tightness continues to support.

Middle Distillates:

- Bullish Singapore ULSD cracks: VAT changes in China are set to drive cracks higher, justifying increased runs from South Korean refiners.

- Atlantic Basin tightness to persist: NWE spot markets remain backwardated as imports drop and cold weather adds upward pressure.

- East/West spread support: Expect East/West swaps to stabilize around $20/t as NWE and Singapore premiums align.

Residue:

- In the East of Suez, steady to bearish for HSFO in the EoS as supplies grow, while for VLSFO the outlook is neutral on firm supply-demand dynamics.

- A similarly weaker outlook for HSFO in the West of Suez amid widening supply replenishments althought in the US the downside will be limited by ending refinery turnarounds and low inventories.

Light Ends: Naphtha cracks continue to weaken as Asian demand drags

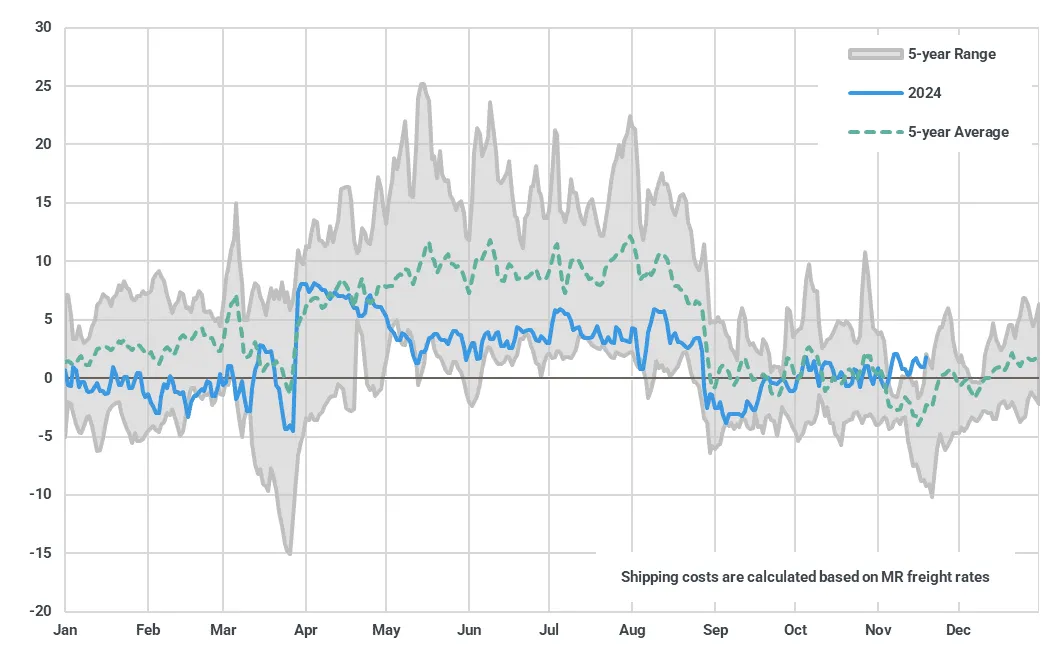

Light naphtha cracks ($/bbl)

Source: Kpler calculations using Argus Media prices

East of Suez

Global naphtha cracks have continued their modest decline, as expected, with cracks in Asia pulling the global complex lower w/w. Indeed, in the East of Suez, refinery maintenance in the Middle East has not been enough to offset waning cracking demand and improved simple refinery margins allowing the region’s net short position to ease as cracker operators look to destock inventories ahead of the year’s end.

Moreover, initial reports for November suggest Russia’s refinery runs have improved m/m with maintenance largely finished, although weak simple refinery margins and ongoing issues at Tuapse are likely to cap exports going forward, despite additional output from Novatek’s new splitter in Ust-Luga.

Looking ahead, although two steam crackers are in the process of ramping up in China (Ineos-Sinopec, 1.2 Mt/year) and Yulong’s No.1 (1.5 Mt/year) these units will rely on ethane and integrated-refinery feedstock, having little effect on naphtha balances.

Indeed, we expect Chinese naphtha appetite will only begin to improve from mid-December as Wanhua Chemicals No.2 (1.2 Mt/year) mixed feed ethane/naphtha cracker and Exxon’s Huizhou mixed feed (LPG/naphtha) cracker (1.6 Mt/year) look for feedstock ahead of their Q1 2025 start dates. As such, we continue to expect Asian naphtha cracks to modestly decline w/w until mid-December (without falling below the five-year average), after which strength will return to the market as flexible crackers continue to favor naphtha over LPG and meagre refinery runs continue to crimp local supplies.

NEA Naphtha cracking margins ($/t)

Source: Kpler calculations using Argus Media prices

West of Suez

In the West of Suez, European cracks only moderately fell w/w, being dragged lower by weakening fundamentals in Asia. Indeed, a recovery in gasoline exports to Africa in recent weeks has helped to spur blending demand while the easing of cracker maintenance in Germany has added structural support to cracking demand m/m.

USGC light naphtha arbs ($/t)

Source: Kpler calculations using Argus Media prices

As such, with US exports underperforming in relation to seasonal refinery runs and lower-than-typical turnarounds (likely due to more light naphtha being blended into winter gasoline following a specification change last month), there has been a surge in demand for swing barrels from the Med, with competition between NWE and Asia briefly leading to the E/W spread flipping into negative territory on Monday.

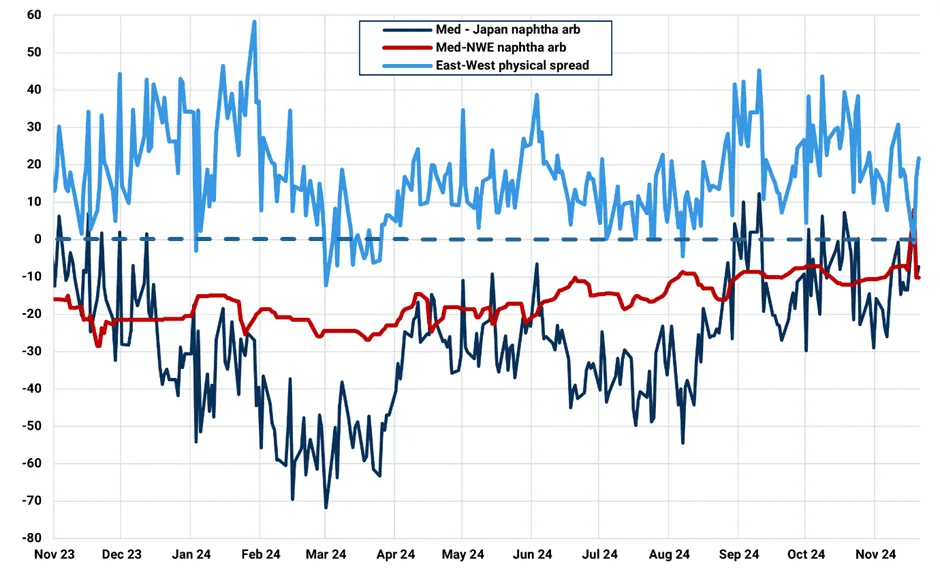

Med naphtha arbs ($/t)

Source: Kpler calculations using Argus Media prices

However, the spread has since normalized and looking ahead, we continue to expect that the E/W spread will widen back above the five-year average from December. This is due to Atlantic Basin refinery maintenance ending, blending demand weakening and cracking demand in Asia improving as operators in the region look to replenish stocks for the H2 January delivery cycle while new crackers reliant on imports look to purchase feed before they ramp up in China over Q1.

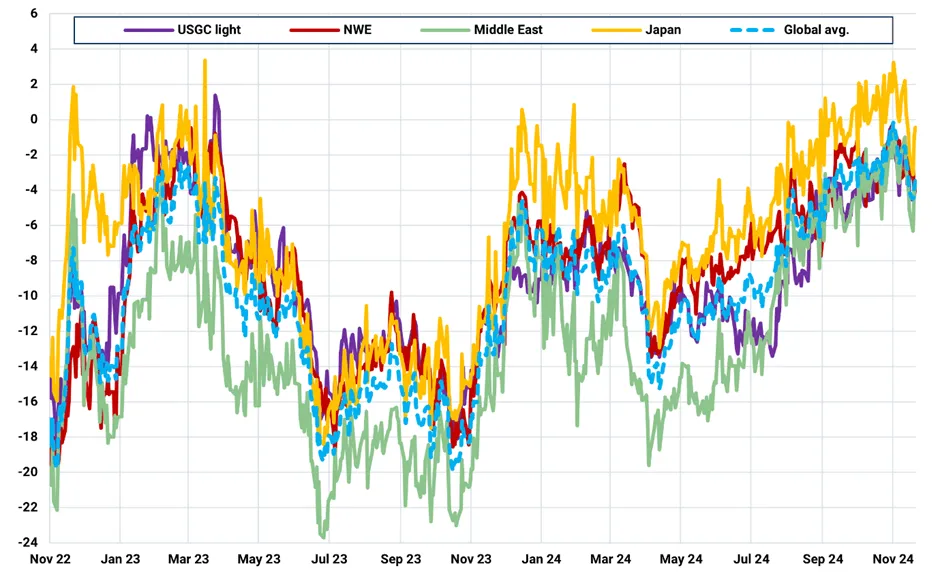

Global naphtha cracks ($/bbl)

Source: Kpler calculations using Argus Media prices

Gasoline: Cracks Up; US Gasoline Market May Soon Lose Momentum

Global Gasoline Cracks ($/bbl)

Source: Kpler based on Argus Media

Americas

US gasoline cracks posted weekly gains, with RBOB cracks in particular rising $2.90/bbl w/w to $17.30/bbl — leading global benchmarks. Gulf Coast cracks also gained $0.80/bbl to $10.00/bbl. Recent bullishness stemmed from destocking, heightened implied demand, and reduced imports. However, market fundamentals are starting to signal a potential reversal. The latest EIA data showed motor gasoline inventories increasing by 2.1 Mbbls to 208.9 Mbbls, aligning with seasonal trends but still 4% below the five-year average. At the same time, implied demand dropped to its lowest since early September. While we could still see some upside around Thanksgiving and the holiday period, with refining capacity back in full force post maintenance and crude processing remaining at elevated levels, we expect the market to lengthen considerably towards the end of the year, setting a ceiling for cracks.

US: Weekly gasoline inventories (Mbbls)

Source: EIA

US: Weekly gasoline supplied (Mbd)

Source: EIA

Europe

European gasoline cracks climbed as well, with NWE gaining $0.40/bbl w/w to $7.05/bbl and Med cracks up $0.50/bbl to $9.00/bbl. Despite this month’s recovery in export demand (alongside improved transatlantic arbitrage economics, see chart below), the European region is set to remain the weakest in our books in the weeks ahead, as balances keep swelling.

Of note, Nigeria’s Dangote refinery has started shipping gasoline abroad – something we anticipated was about to materialize (see Chart of the Month), which should add further pressure on the European gasoline market.

Freight Adjusted Arb Incentive: 3DMA of Gasoline reg RBOB NYH barge fob 20 days fwd vs Gasoline Eurobob non-oxy NWE barge ($/bbl)

Sources: Kpler calculations using Argus Media pricing, McQuilling freight data

Asia

Singapore cracks rose $0.40/bbl w/w to $11.70/bbl. News that the Chinese government is planning to reduce the VAT rebate on oil product exports from December have dominated the East of Suez market this week, with reports indicating that Chinese refiners are attempting to increase gasoline exports before the reduced rebate kicks in, as export incentives are still more favourable for gasoline as compared to other products (see Middle Distillates section). However, this will be difficult to execute given that we are quickly approaching December, and the November loading program for gasoline was already increased vis-à-vis previous months.

Notwithstanding, our view remains that there is some upside potential to be realised in the wider region as the market remains tight over Q4, adding a floor of support under the Singapore gasoline crack.

Data Spotlight

Hedge Fund Activity: Data up to November 12 shows money managers have increased their RBOB long positions to the highest since May, reflecting near-term optimism. However, this positioning could face headwinds as inventories recover and fundamentals soften into December.

Nymex RBOB Gasoline hedge fund positioning (contracts)

Source: Kpler calculations using CFTC data

Middle Distillates: China’s 4% export VAT to support prompt Singapore cracks

East of Suez

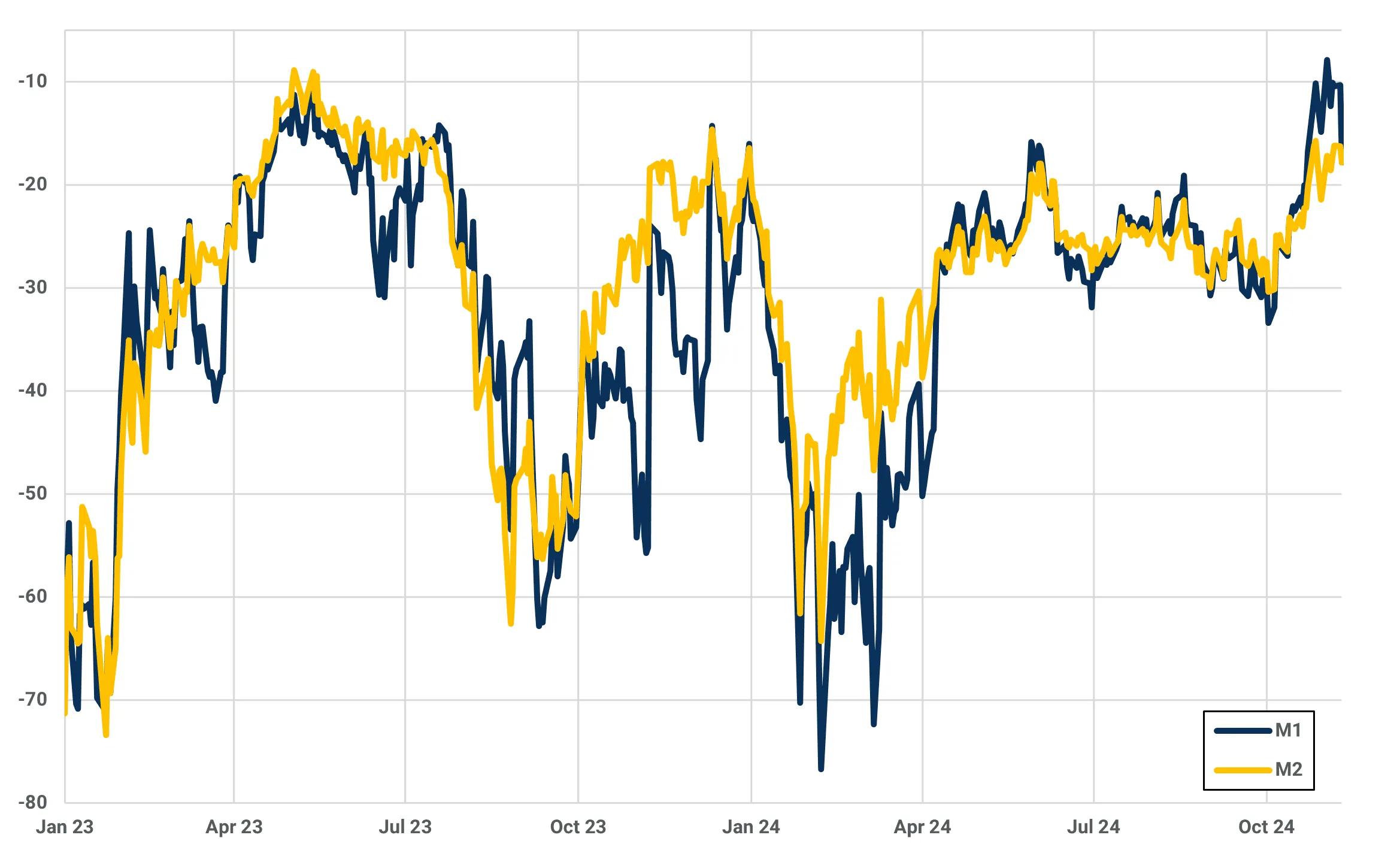

The Singapore spot market is set for another bout of tightness, following news that the Chinese government has scaled back VAT rebates on oil product exports from the full 13% rate to 9%. In practice, this is a 4% VAT rate and will further strain Chinese refiners who are already struggling with low margins and peaking domestic demand.

This 4% VAT appears very damaging to Chinese refiner margins, rendering exports unworkable for large parts of the year. Our calculations indicate that the China-Singapore gasoil export incentive is reduced by an average of $3.80/bbl when retroactively applied throughout 2024.

China-Singapore gasoil arbitrage incentive ($/bbl)

Source: Kpler calculations using Argus Media pricing

The timing of this announcement is unfortunate on many fronts. For Chinese refiners, this represents a missed opportunity to fully utilize their export quotas, with over 10 Mt left for December. Chinese refiners’ attempts to shift December-loading cargoes to November to beat the hikes will be logistically and operationally challenging. As for the broader region, this further tightens a market that is already short on both higher sulfur grades and ULSD due to refinery outages and maintenance.

We expect Singapore ULSD cracks to rise in the interim, which will justify higher runs from South Korean refiners and exports. Summer-grade producing Indian and Middle Eastern refiners are also expected to continue their Eastward pivot.

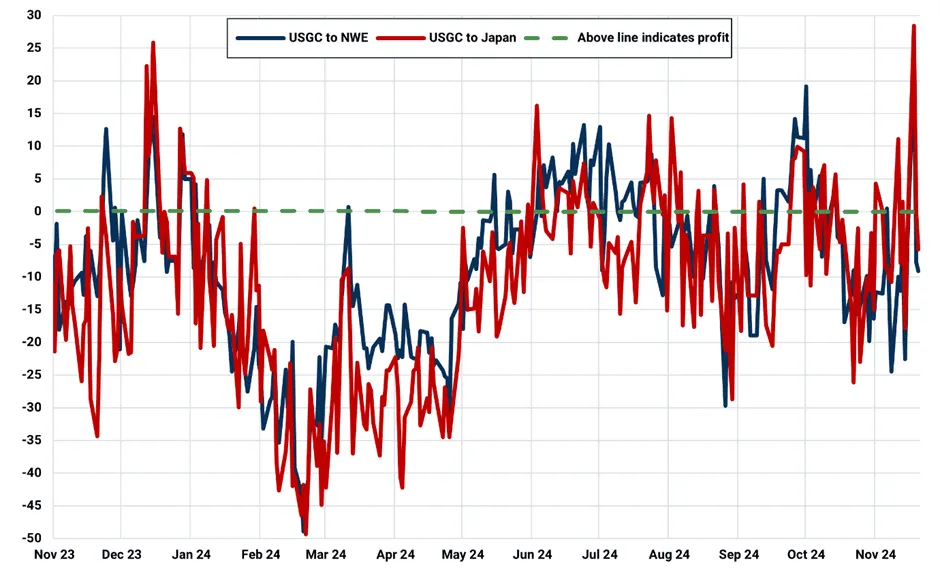

Gasoil East/West swap ($/t)

Source: Argus Media pricing

West of Suez

While this would typically cause a major narrowing of the East/West spread, the effect has been muted given maintenance in the Middle East – taking export-oriented refineries al-Zour and Yanbu offline. The current Atlantic Basin tightness shows no signs of easing as NWE imports have declined in recent weeks while there has been a sharp drop in cargoes on water. The onset of a cold snap across Europe has provided further support to the prompt spot market, with December forecasts expecting temperatures across France and Germany to be 3-6°C lower than average. This constructive momentum looks set to stay: the prompt time spread is steeply backwardated at over $6/t, while ICE Gasoil net short positions have hit a three-month low of minus 7.97 Mbbls.

We expect the East/West swap to trade around minus $15-20/t level as NWE cash differentials must rise along with the Singapore market to continue drawing cargoes from the Middle East and India.

Residues: HSFO markets soften after prolonged summer buzz

The HSFO market presents divergent dynamics across key regions. In Europe, prices face downward pressure as supply replenishments grow and refining margins remain weak, despite easing maintenance and ongoing outages at major refineries like Shell Pernis and Greece’s MOH. In contrast, the US market is supportive, buoyed by resurgent feedstock demand as maintenance halts in December, compounded by tight inventories and low imports. Meanwhile, HSFO markets in the East of Suez are set to soften, driven by weakening European markets and a looming recovery in Middle Eastern exports although potentially lower Russian loading could limit the downside. As for eastern VLSFO markets, they remain steady on steady bunkering demand, stable floating storage levels, and robust Chinese imports.

West of Suez (WoS)

The European HSFO market faces further downside risks as supply replenishments continue to trickle in, weighing on prices as they continue to recover from their recent peaks. Although refinery maintenance has slowed from its October peak of 2 Mbd to 1.1 Mbd in November (IIR), weak simple refining margins could offset increased feedstock demand, limiting the downward pressure on regional fuel oil markets.

Simple GRM ($/bbl)

Source: Kpler based on Argus data

Compounding these headwinds, ongoing maintenance at Shell's Pernis refinery in Rotterdam and prolonged outages at Greece's MOH refinery are contributing to constrained fuel oil output. While these factors may tighten supply in regional markets, the overall European HSFO market remains poised for further losses, driven by growing replenishments and weak margin environments.

In contrast, the US HSFO market shows signs of support as refinery maintenance comes to a full stop in December (IIR), driving an uptick in feedstock demand. This comes against a backdrop of persistently low domestic fuel oil inventories, which continue to trend well below their five-year seasonal averages.

US: Weekly fuel oil inventories (Mbbls)

Source: Kpler calculations based on EIA

The end of maintenance activity is expected to bolster refinery utilization rates, increasing the demand for HSFO as a critical feedstock. Additionally, subdued imports into the US further amplify its supply tightness, reinforcing supportive price expectations for the coming weeks.

East of Suez (EoS)

Our near-term outlook for HSFO markets is steady to bearish, primarily driven by the expectation of growing supplies. Weakness in the European markets will also seep into EoS markets, compounding the weaker sentiment.

Asian refinery maintenance schedules show a slowdown in offline capacity, with offline crude distillation unit (CDU) capacities falling from 2.3 Mbd in November to 1.5 Mbd in December (IIR), signaling increasing availability of HSFO in the region.

In the Middle East, fuel oil exports during the first 20 days of November have dropped nearly 50% to 2.2 Mt compared to full October volumes due to maintenance activities. However, exports are expected to recover as maintenance winds down in December, contributing to regional supply increases.

Additionally, Russian fuel oil exports, which predominantly are shipped to EoS markets, are slowing amid reported refinery stoppages, including the Tuapse refinery which has seen its fuel oil exports drop to a nine-month low of 150 kt in November. While this could strain supplies in the East, the rebound in Middle Eastern exports will likely counterbalance this, maintaining the weaker outlook for regional HSFO prices.

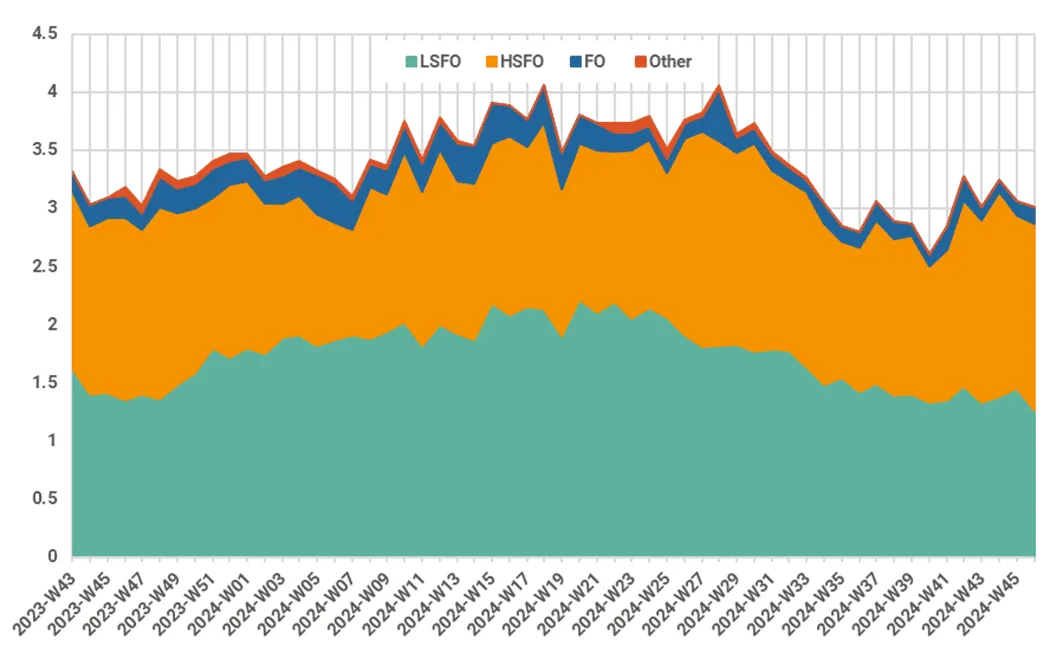

Meanwhile, the outlook for VLSFO markets remains steady on balanced supply-demand fundamentals. Firm Chinese VLSFO imports, driven by limited domestic VLSFO export quotas, are supporting prices as suppliers source cargoes from abroad creating a price floor under regional prices.

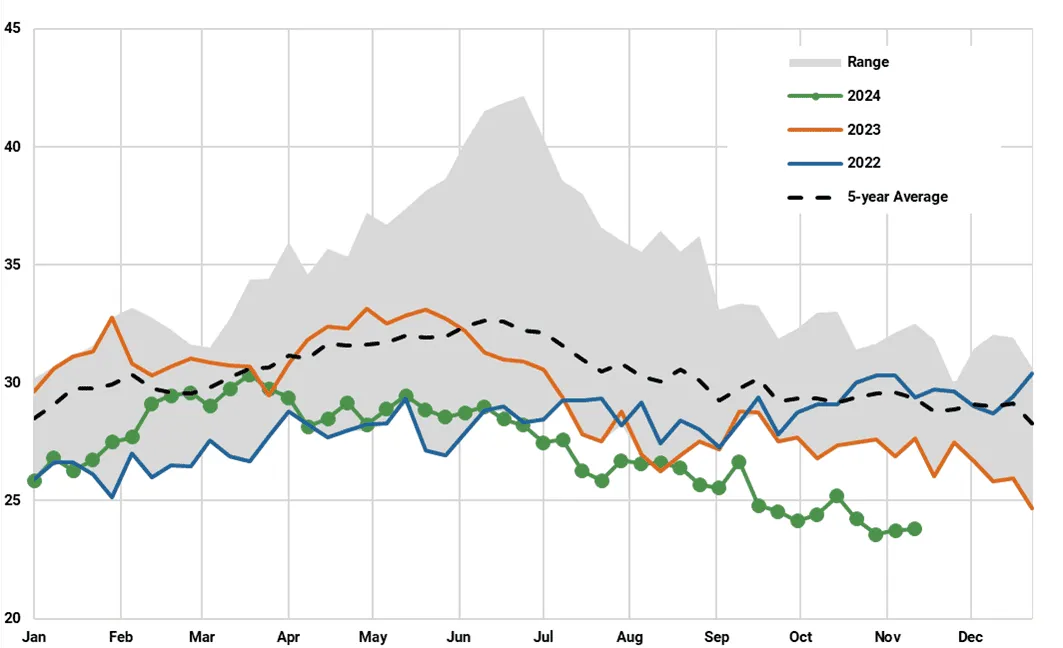

VLSFO floating storage around the Singapore hub are holding steady at approximately 1.5 Mt. Import activity into Singapore also remains robust, ensuring consistent supply flows.

Fuel oil inventories in floating storage around Singapore (Mt)

Source: Kpler

Want access to Insights on a regular basis?

Through unbiased, expert-driven research and news, you’ll receive valuable information on supply, demand, and market movements, enabling you to make informed trading and risk management decisions.

Unbiased. Precise. Essential.

Curious? Request access to Kpler Insight today.

See why the most successful traders and shipping experts use Kpler

Get daily expert-driven research through Insight.

.jpg)