US ethane exports to China at risk due to new licensing requirements

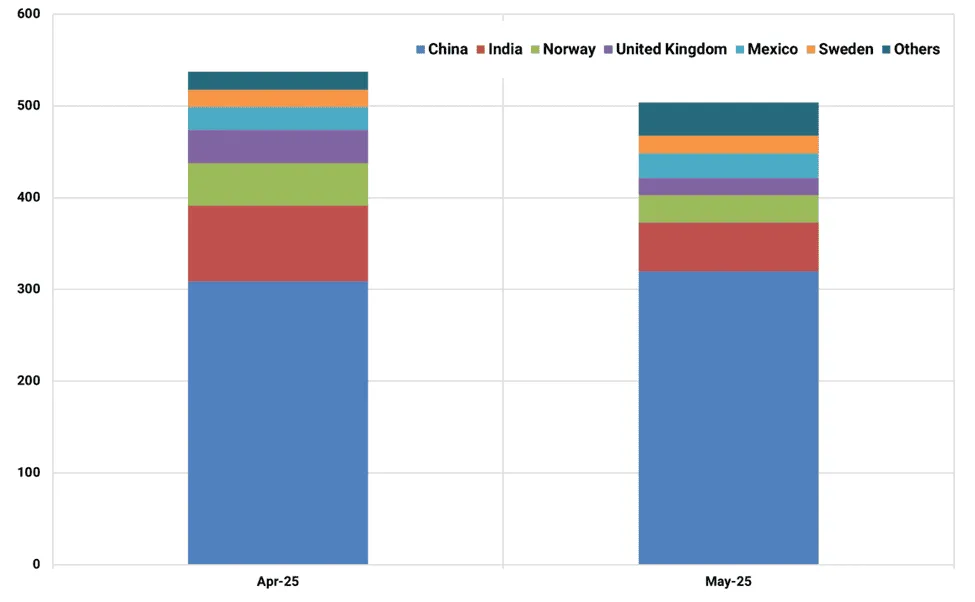

With May nearing an end, US ethane exports are set to drop 33 kbd m/m (-6%) from April’s record high to 504 kbd despite overhanging trade tensions. However, new licensing requirements from the Trump Administration for ethane and butane exporters puts resilient US-China ethane flows at risk.

Market & Trading Calls

- New licensing requirements for US ethane and butane exporters keeps trade barrier uncertainty front and center despite a US trade court finding the Trump Administration’s broad reciprocal tariffs unconstitutional.

- Our base case is that ethane will avoid the worst of the trade barriers from both sides given the concentration of US supply and Chinese demand, allowing resilient Chinese demand and growing US exports to continue, but significant downside in flows and Mont Belvieu ethane prices is a risk depending on licensing requirements and other pending tariffs.

- If US ethane flows to China are blocked, naphtha demand, cracks in China, wider region will pick up as flexi-crackers increase naphtha processing to make up for falling Chinese ethylene output, adding to our already constructive view on the E/W spread through June.

US ethane exports to China have been resilient so far in the face of tariffs, with May export data supporting our recent upward revision to our Chinese ethane demand figures for 2025. In May, US ethane exports to China are set to rise 11 kbd m/m (+3.5%) to 320 kbd (+61 kbd or +24% y/y).

However, an 8-K filed by Enterprise on 29 May shows that this resilience is at risk, as the company noted that the Trump Administration is now requiring exporters of ethane and butane to apply for a license with the Commerce Department’s Bureau of Industry and Security. According to the filing, Enterprise is uncertain if they will be able to obtain the license, and they note that the government rationale is that the exports pose an unacceptable risk relating to military end use in China. Enterprise will review their internal controls, suggesting that further vetting of buyers and end users might be required, which may prove difficult in an opaque and fragmented industry. Other US NGLs exporters likely received similar notices, putting large volumes of ethane in particular at risk given that ethane has more US-China concentration than butane.

The justification of these restrictions have parallels to existing limitations on the export of high-end AI chips to China, but with some key differences. While ethane and butane can be used in military applications, they are fundamental building blocks to a range of goods outside the military realm. And unlike purpose-built semiconductors, they are not direct tools in an area of strategic competition between the two countries. Given these differences, the Trump Administration may choose to work with the ethane and butane exporters to make licensing requirements less onerous to reflect the wide range of non-military end uses.

Our view is that ethane is likely to avoid the worst of these impacts as it has received differential treatment before given the lack of options for both US sellers and Chinese buyers. This continuation of the status quo is at risk depending on the requirements of the export license, and any significant and persistent trade barriers would push our view back towards our much more bearish early-April demand outlook.

Indeed, if ethane exporters are unable to ship ethane to China, flexi-crackers in country would turn to naphtha to help fill the domestic ethylene gap and crackers in the wider region would be able to lift runs to make up for the loss of ethylene production in the Chinese market, which retains the largest net short of ethylene and derivatives.

Nonetheless, with China-bound ethane volumes holding up for now, this month’s drop in US exports was driven by the three next largest importers: India, Norway, and the UK. US ethane exports to those three nations dropped 63 kbd m/m (-38%) to 102 kbd in May. Seasonal maintenance may be starting later than usual at Rafnes this year in Norway, while exports to the UK may be limited due to downstream demand concerns, high energy costs (which forced Sabic to postpone its Wilton ethane cracker upgrade project this year) and naphtha-based term contract pricing which has outpaced the rebound in USGC spot ethane prices since the lows of early April.

US ethane exports by destination country (kbd)

Source: Kpler

There is some destination uncertainty for two VLECs which recently left ET Nederland and are likely heading to Eastern Asia, though they are both included in the May China destination figures in this analysis. The Satellited-charted Seri Elbert left Nederland on 26 May, and her usual Nederland to Satellite Lianyungang voyages suggest a return to China. Additionally, the VLEC Gas Jessamine was recently delivered to Tianjin Southwestern Marine, and she is likely chartered by Satellite and headed to Lianyungang with her first cargo.

While ethane has seen significantly less destination reshuffling than LPG since early April, even diversions of the Seri Elbert and Gas Jessamine could swing May US-China exports by around 30 kbd each if they end up at a different destination. Additionally, although downstream demand uncertainty has been felt across the board, ethane utilization rates will be supported by comparatively superior margins.

Northeast Asian gross complex steam cracking margins per ton of ethylene ($/t)

Source: Kpler calculations using Argus Media prices

See why the most successful traders and shipping experts use Kpler