Detangling the tariff knot – considering what’s returning to China

Market & Trading Calls

- Trump Tariff De-Escalation: following a chaotic start to 2025, the Trump administration has eased back on tariff implementation in a bid to negotiate trade deals. This marks a clear retreat from earlier ambitions to begin taking on a highly imbalanced global trading system. It looks likely that Trump will negotiate some type of limited deal with the Chinese that involve commitments to buy a certain amount of US goods and possibly cap Renminbi strength.

- Short-Term Relief, Long-Term Risks: market sentiment and consumer confidence have rebounded, but deeper issues remain unresolved, namely widening global trade imbalances and associated wealth inequality. China, meanwhile, gains short-run flexibility to maintain its investment-led model, delaying the structural rebalancing needed to correct global trade imbalances.

- US NGLs Matter the Most: China’s temporary rollback of tariffs on US crude, LNG, coal, and grains will have a limited volumetric impact as these trade flows were already small or heading into the off-season. However, the easing of duties on US NGLS, especially ethane and propane, is critical for China’s petrochemical sector, where US supply is irreplaceable.

- Petchems and Ag Shifts: the return of US NGL exports to China is bearish for Middle Eastern LPG and naphtha but bullish for US and European LPG markets. Meanwhile, even with lower soybean tariffs, China’s record Brazilian purchases and seasonal factors limit upside for US soybeans, while Chinese demand for US corn and wheat continues to decline.

Market Analysis

Trump capitulates on Chinese tariffs bringing short-term macro relief but delaying an eventual trade rebalancing.

The Trumpian tariff policy of the past three months has been nothing if not chaotic. At the height of the trade war in April, the S&P traded down to levels that effectively erased the entirety of gains seen in 2024. The 10y treasury yield, after initially trading lower on growth concerns, surged by 70bp as rising inflation expectations took hold, and outside entities looked to diversify away from US debt. Simultaneously, USD briefly traded down to levels not seen since March 2022, also a result of de-dollarization diversification efforts. It was clearly apparent that Trump’s somewhat incongruent policy mix meant to rebalance the global trading system was resulting in a high degree of pain.

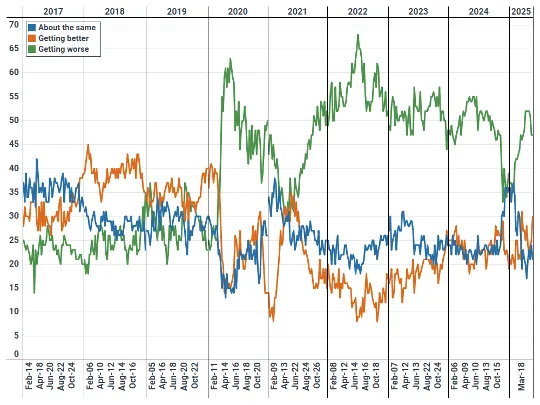

Daily US Household State of the Economy Poll (%)

Source: YouGov, The Economist

Nonetheless, in the weeks following the Liberation Day announcement in early-April, the Trump administration began to capitulate. First, the White House removed extremely high reciprocal tariffs on all but China for three months with the aim of getting trade deals completed. Trump officials quickly followed this up by announcing a cut in tariffs on imports from China as well, with the same framework of a three month holding period to get a deal done. In our view, this is a clear indicator that the Trump administration has moderated his desire to seriously take on the issue of widening global trade imbalances, which would have required a number of additional policy efforts beyond tariff implementation.

Backing off of an aggressive US tariff policy brings short-run macro relief. The S&P has rebounded 20% off the intra-day low on April 7th, and consumer confidence levels have recovered a bit after rapidly weakening between January and mid-April. While the American macroeconomy will likely undergo slowing consumption and investment growth over the next couple of quarters as a result of extreme uncertainty in March/April, if Trump sticks to a roughly 10% baseline tariff, with a rate a bit above this level for China, American growth is poised to pick up again at the end of this year and into early next year. A potential US tax cut will also provide a tailwind, albeit at the expense of higher interest rates and debt accumulation over the medium- and longer-term.

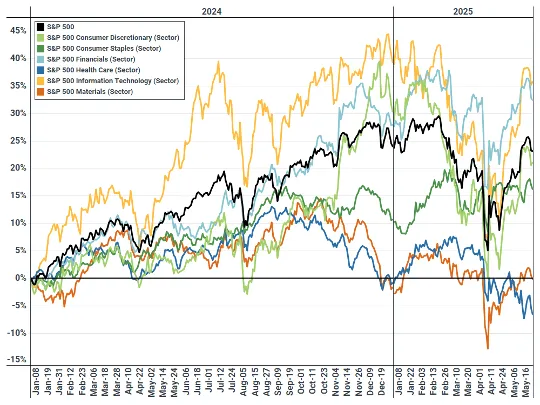

Relative S&P Sector Performance Relative to Jan 1, 2024 (%)

Source: FMP

However, we want to stress that the issue of widening trade imbalances will likely intensify over the next decade given the reality that an imbalance in trade tends to result in rising wealth inequality. The status quo, where America absorbs roughly half the global surplus from places such as China, and Germany, is unlikely to continue into perpetuity, even if that system is set to remain in place for now. It is our view that the bottom 50% of American households, who have seen their labor share of income drop precipitously while failing to enjoy the sizeable runup in US asset prices over the past two decades, will demand changes. These issues are largely the result of offshoring, overproduction in China, and a sizeable US current account deficit.

China is also set to benefit from White House capitulation in the short run. China will have more flexibility to continue its investment-led growth model with less fear that America is going to step back from playing the role of global importer. China’s economic model tends to encourage investment and production while suppressing household consumption, which effectively pushes net exports ever higher. So far this year, against our expectations, Chinese growth has yet again been led by manufacturing investment and industrial production, rather than household consumption. Virtually no steps towards rebalancing have taken place.

Eventually, as the United States steps back from its dominant importer role, China will have to rebalance. Consumption will need to increase by roughly 20pp as a percentage of domestic income, while the rate of investment declines by roughly the same amount. This will require a Chinese wage environment that far better aligns with Chinese worker productivity, and a dramatically widened social safety net. However, these shifts in political policy have likely been pushed further out amid Trump’s step back from aggressive tariff policy.

Through the rest of this update, we will focus in on the short-run shifts in commodity trade flows resulting from an easing in trade tensions between America and China. This will include highlights around US NGLs, and grains, as well as considerations of knock on effects to alternative exporters who were looking to fill the gap left by the United States.

US energy commodities: major tariff impact on NGL flows; limited implications for US crude, LNG, and coal.

While initial Chinese tariffs on US crude, LNG, and coal were certainly a symbolic ratcheting in trade tensions, the recent easing in import duties will have a limited impact given the relatively limited volumes of these trade flows to begin with. Chinese imports of US crude halted entirely in May, with the last US cargo unloading in Ningbo on April 25, 2025. Nonetheless, US crude volumes made up just 1.5% of China’s total crude imports last year (178 kbd). These barrels consisted primarily of Mars and WTI. Mars can be readily replaced by grades from the Middle East and Latin America, while WTI alternatives are available from West African grades, CPC Blend, and Murban.

US-China Trade - Share of Seaborne Commodity Flows 2024 (%)

Source: Kpler

Similarly, flows of US LNG and coal to China are minor in volumetric terms and a resumption in US-China flows would therefore not prove very consequential. US LNG accounted for just 5.5% of Chinese imports in 2024. The last US LNG cargo discharge in China took place February 6, 2025. Ample Pacific LNG supply currently facilitates replacement, while a greater share of US LNG was shipped to Northwest Europe and Northeast Asia. US coal only represented 2.4% of Chinese imports in 2024, with India emerging as a major alternative buyer of US-sourced volumes shunned by China. Simultaneously, China’s big three suppliers, Indonesia, Australia, and Russia, have easily replaced these US flows.

Nonetheless, China’s petrochemicals sector relies heavily on US NGLs of which it imported 863 kbd in 2024, representative of 62% of total NGLs imports into the country that year. The bulk of this volume was comprised of propane (576 kbd) and ethane (261 kbd). The 125% tariff on US ethane was already waved on April 29, even before US tariff capitulation. Contrary to LPG, the US is the only exporter operating at a scale large enough to meet Chinese demand. US ethane has thereby regained its position as the most profitable petrochemicals feedstock in China.

Yearly Chinese Seaborne NGL Imports by Origin (kbd)

Source: Kpler

The most recent 90-day US-China tariff pause that began on May 14th restores typical trade flows of US LPG, ethylene, and derivatives, helping these volumes re-enter the Chinese market. This shift is bearish for Middle Eastern LPG as Chinese buyers pivot back to US supply. Simultaneously, OPEC is ramping up crude output, albeit the correlation between crude and NGLs production should not be overstated as rising crude production often comes from heavier fields with lower associated gas content. The resumption of US ethylene flows to China will also support US ethane cracking demand once unplanned outages ease in June. US ethane and derivative exports are poised to benefit from resumed trade, while naphtha demand softens in Asia as flexible crackers revert to LPG.

In Europe, LPG prices will rise as US cargoes reroute to China, tightening regional supply amid seasonal maintenance and strong naphtha cracks. Overall, the market outlook turns bullish for US, European, and Asian LPG versus crude, but bearish for Middle Eastern LPG and naphtha. Nonetheless, although the temporary rollback of US-China tariffs has undone many of the market trends seen since April, most prices and petrochemical margins have yet to fully recover, with elevated uncertainty continuing to delay petrochemical project timelines.

A resumption in Chinese purchases of US soybeans unlikely

Among the major grains/oilseeds, soybeans play the largest role in US-China trade, with China being the largest buyer of US volumes. While Chinese imports from the US have remained relatively stable in outright terms, China ramped up its buying of Brazilian soybeans in 2023 and 2024, and this trend accelerated this year amid a record harvest in Brazil.

Yearly Chinese Share of Demand for US Grains/Oilseeds Exports (%)

Source: Kpler

Chinese imports of US soybeans have come under pressure since tariffs were announced in February. Even though Chinese duties on US soybeans were reduced to 23% for 90 days from May 14, this will only have a marginal impact on physical flows as we are approaching the off-season for US exports. Overall, fundamentals for US soybeans remain bearish even in the relative absence of tariffs, as China is likely to take advantage of Brazil’s record crop this year to strategically lower its imports needs from the US in H2 2025.

Chinese buying of US corn has already been on a firm downward trajectory since 2022, and dropped to only four cargoes year-to-date, compared to 35 during the same period last year. However, weaker exports from the Black Sea region and Brazil allowed US corn to successfully gain market share in Northeast Asia and even Europe this year. This temporarily buffered muted Chinese buying interest, however, a likely continuation of reduced Chinese buying of US corn will become increasingly difficult to compensate due to greater competition from Brazil (safrinha corn crop in very good condition) and Argentina (average yields above year-ago levels). Simultaneously, the potentially largest US corn acreage planted since 2013 suggests a major US crop this year.

By comparison to soybeans and corn, demand for US wheat exports is more diversified. Wheat plays a minor role in US-China trade, and volumes took another step lower in 2025 relative to year earlier levels. Year-to-date, only a single US wheat cargo is scheduled to discharge in China in late May compared to 18 cargoes over the same period 2024.

Monthly Chinese Imports of US Soybeans (Mt)

Source: Kpler

Want market insights you can actually trust?

Kpler delivers unbiased, expert-driven intelligence that helps you stay ahead of supply, demand, and market shifts. Our precise forecasting empowers smarter trading and risk management decisions - backed by the most accurate oil price predictions two years running.

Unbiased. Data-driven. Essential.

See why the most successful traders and shipping experts use Kpler

Expert research & analysis driven by proprietary data