Mixed global LNG price outlook as TTF strength contrasts with stable Asian LNG and softer HH

Market & Trading Calls

European TTF front-month price outlook: Slightly bullish, supported by lower-than-average temperatures, strong storage withdrawals, and Norwegian maintenance. Upside risk remains from concerns of potential disruptions to US LNG exports amid cold temperatures. However, upward revisions to temperature forecasts, improving wind generation, and strong LNG inflows into Europe could cap further gains.

Asian LNG front-month price outlook: Stable, as easing cold in China and stronger coal-fired in Korea offset emerging cold spells in Japan and Korea, keeping spot buyers sidelined.

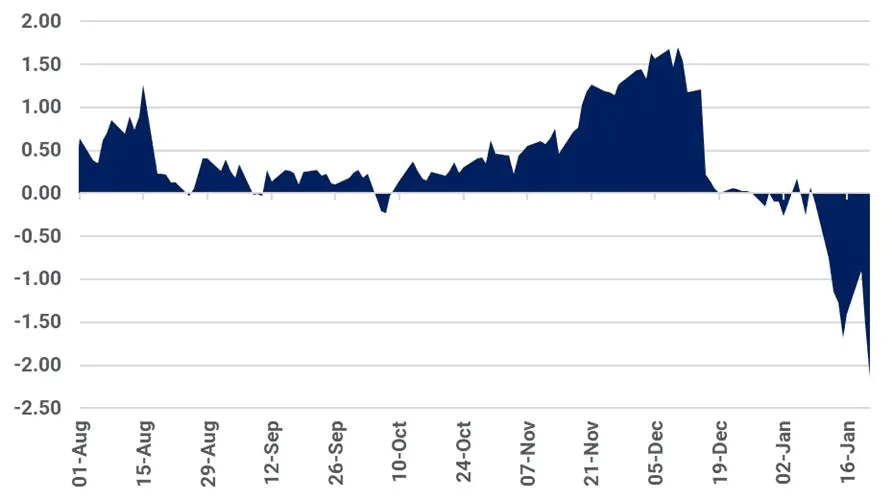

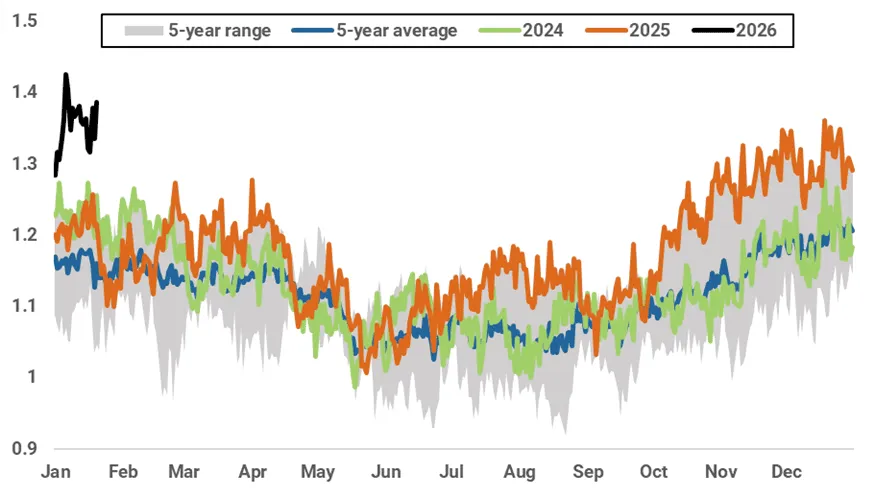

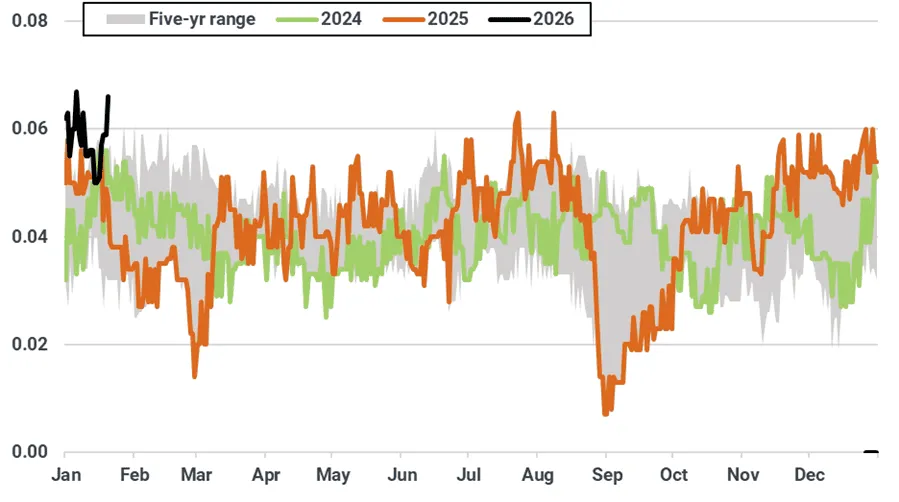

Asian LNG – TTF spread outlook: TTF premium to widen as Asian LNG prices are likely to remain stable while TTF is expected to gain slightly next week. The TTF premium increased to $2.15/MMBtu on 21 January, driven by the sharp w/w uptick in TTF prices.

US Henry Hub front-month price outlook: Slightly bearish as while the nearly $2.00/MMBtu surge in prices this week brought bulls firmly back into the market, the imminent roll off of the February contract and forecasts for a mild start to February may cause prices to ease over the next week. However, prices are also expected to be highly responsive to upcoming revisions to weather models.

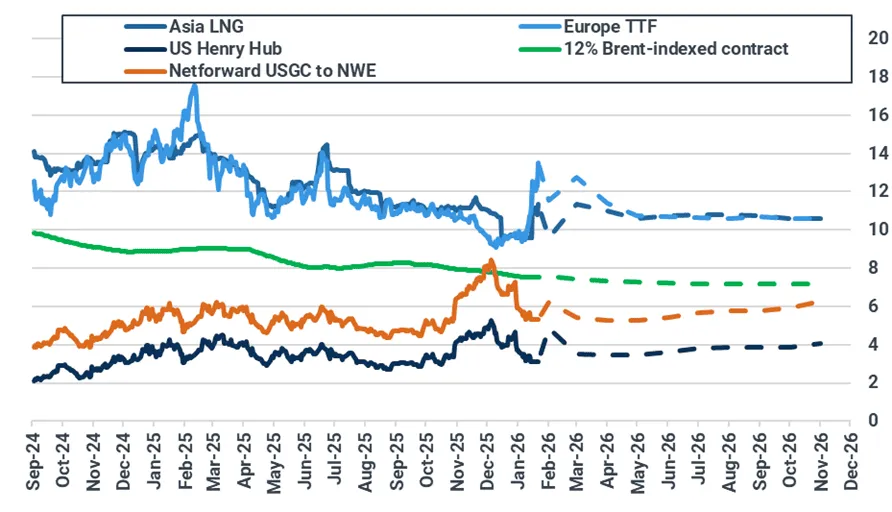

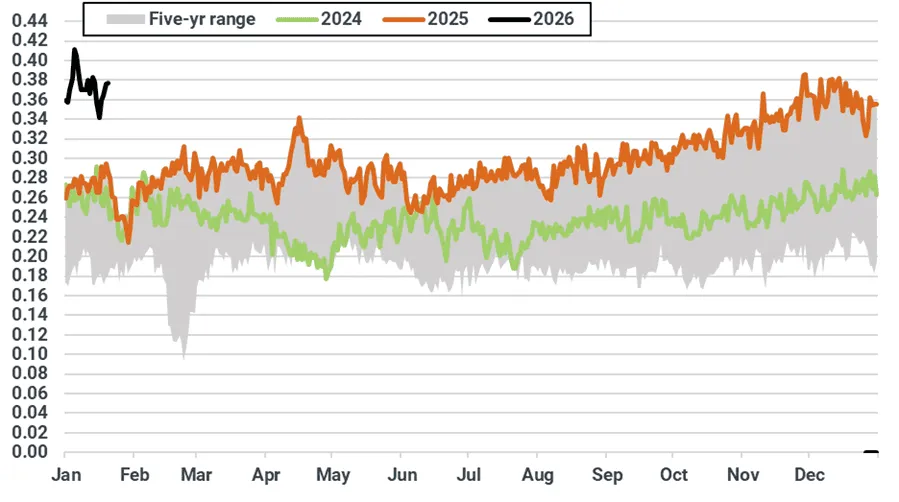

Key natural gas and LNG front-month prices ($/MMBtu)

Source: ICE, NYMEX, Spark Commodities. Brent-indexed price represents 12% slope of 90-day moving average of Brent contract. Netforward USGC to NWE calculation is 115% Henry Hub contract plus shipping and regasification costs into Gate (Spark Commodities).

Asian LNG-TTF front-month spread ($/MMBtu)

Source: ICE, Kpler Insight

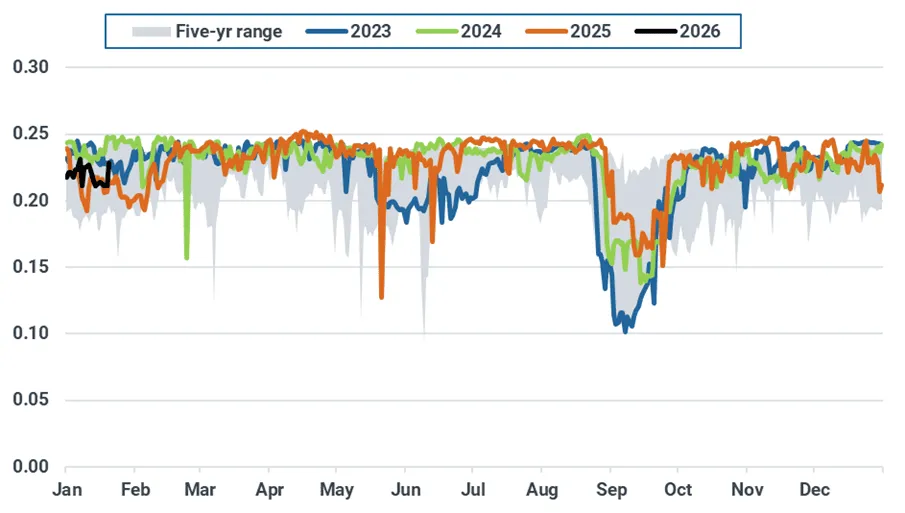

Atlantic basin LNG front-month arbs ($/MMbtu)

Source: Spark Commodities, incorporating ICE-listed Spark Freight and Spark Cargo products. For a full M+12 forward curve and netback cost breakdown, contact Spark at info@sparkcommodities.com

Europe: TTF to remain supported by low temperatures, storage drawdowns, Norwegian maintenance, and fears of disruption to US supply

The European TTF front-month contract extended its bullish run last week, rising sharply to $13.5/MMBtu on 21 January, up $2.6/MMBtu (+24%) from 14 January. Prices climbed through most of the week, declining on 19 January following concerns over potential of US tariffs on European goods. The move proved short-lived and the rally continued driven by temperature forecasts pointing to a prolonged cold spell extending into February, lower y/y underground gas storage levels, highlighting concerns over faster-than-expected depletion, and revisions to Norwegian scheduled maintenance over the coming weeks. On 21 January alone, TTF jumped by $1.1/MMBtu amid fears that an approaching cold spell in the US could disrupt LNG feedgas flows and exports.

Looking ahead, Kpler Insight holds a slightly bullish view on the TTF front-month contract for next week, supported by forecasts for below-average temperatures across Northwest, Central, and Eastern Europe. Concerns over faster underground storage depletion and Gassco’s revised maintenance schedule, reducing availability by around 25 mcm/d at Nyhamna and associated fields, and potential disruptions to US feedgas flows and LNG export capacity amid an approaching cold spell will continue to provide support. That said, downside risks persist as upward revisions to temperature forecasts over the past week and improving wind generation point to a more limited demand impact, while strong European LNG imports are expected to provide some offset on the supply side.

Turning to supply, EU net pipeline imports declined by 2.4% w/w to an estimated 2.6 bcm, driven by lower inflows from Norway. Looking ahead, Kpler Insight expects net pipeline imports to edge lower, as Gassco has scheduled maintenance at the Nyhamna gas processing plant and other fields, impacting around 25 mcm/d over the coming week.

Norway daily net pipeline flows to the EU (bcm)

Source: ENTSOG, Kpler Insight

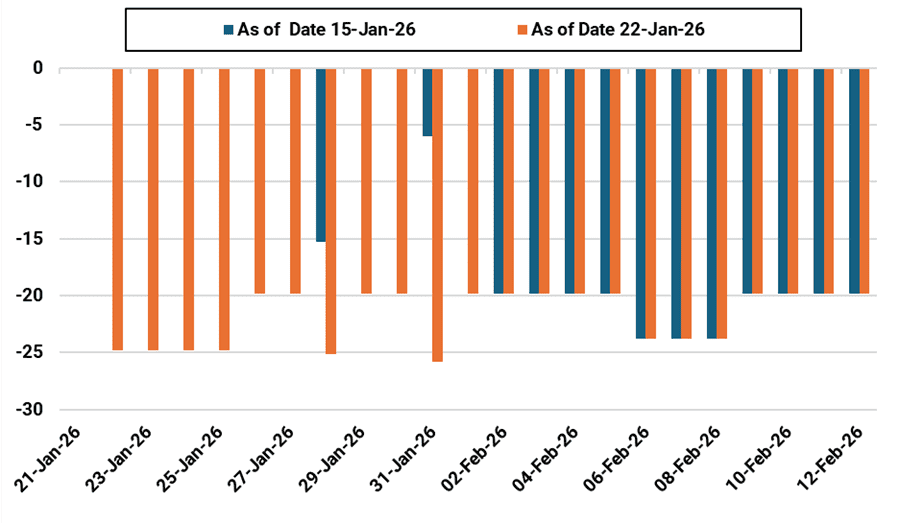

Aggregate daily capacity unavailability of Norwegian fields and processing plants over the next 30 days (scm)

Source: GASSCO, Kpler Insight. As of 22 January 2026

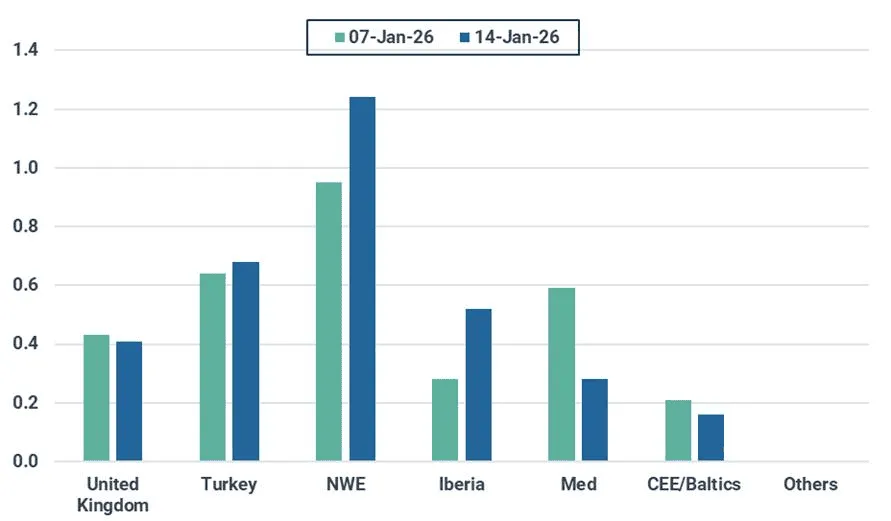

European LNG imports increased by 6% w/w to 3.3 mt last week, broadly in line with our expectations. The rise was driven by higher arrivals in Northwest Europe (+0.3 mt) and Iberia (+0.25 mt), as Atlantic Basin exports recovered and elevated TTF prices continued to attract uncommitted cargoes. Looking ahead, Kpler Insight expects LNG imports to increase further, supported by persistently high TTF prices and the end of unplanned outages at the OLT Toscana terminal, which should lift import capacity in the Mediterranean.

EU-27 weekly LNG imports by region (mt)

Source: Kpler Insight. Data represents week commencing 14/01 and 07/01. NWE=FR, BEL, NL, GER. Iberia=ESP, POR. Med=ITA, HVR, GRE. Baltics/CEE=FI, LT, POL. Others=SWE, MT.

On the demand side, local distribution consumption across 15 EU countries declined to an estimated 4 bcm, down 19% w/w, in line with levels seen in 2024. The weekly drop was mainly driven by Italy (-31%), Netherlands (-29%) and France (-24%) as above seasonal temperatures reduced heating demand. Looking ahead, Kpler Insights expects local distribution consumption to rebound next week as temperatures are forecast to remain below average in Northwest and Central Eastern Europe. Any upside may be capped as temperature forecasts have been revised higher over the last week (see average forecast temperatures for NWE chart below).

EU-15 weekly consumption in the local distribution sector (bcm)

Source: ENTSOG, ENAGAS, Eustream, AGCM, Kpler Insight. The EU-15 perimeter includes AT, BE, CZE, FR, HU, GRE, ITA, NL, LUX, POL, POR, ROM, SLVN, SLVK, and SPA.

On the power side, EU-25 gas-fired generation rose to an estimated 13 TWh, up 9% w/w. This increase came despite a 5% w/w decline in total power demand, as sharp drops in wind output (-37%) and slightly lower nuclear availability (-3%) increased the call on thermal generation. Looking ahead, the outlook for gas-fired generation is mixed: ongoing nuclear outages in France and weak wind generation in Germany provide support, although improving wind output elsewhere in Europe is expected to cap upside potential.

EU-25 weekly gas-fired generation (TWh)

Source: Kpler Power, Kpler Insight.

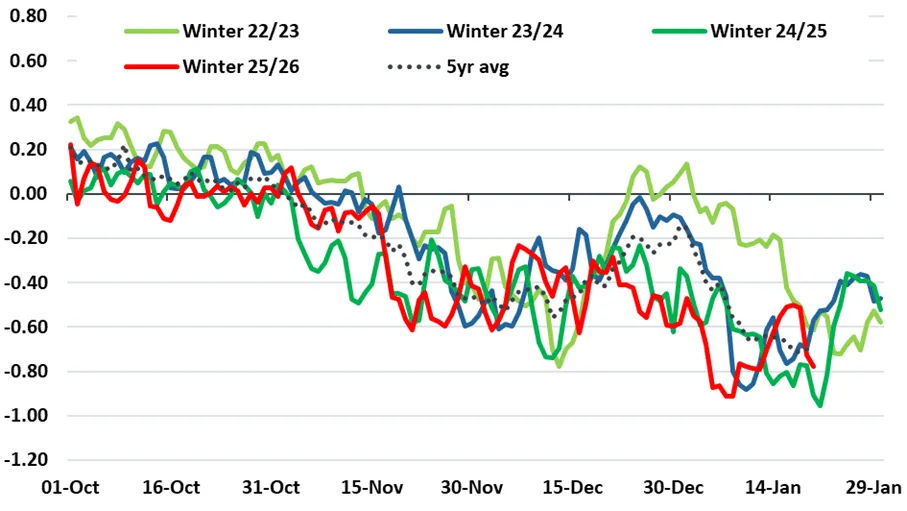

Average forecast temperatures for NWE, excluding the UK (°C)

Source: Kpler Insight. Run comparison 22/01 (solid) vs. 15/01 (dotted), 00:00 UTC. Seasonal is a five-year average. NWE includes BE, NL, FR, DE

EU-27 underground gas stocks fell to 48.3% full as of 20 January, down 4.2 percentage points w/w, as withdrawals accelerated in line with our expectations. The increase in withdrawals was driven by weak wind generation and a favourable TTF day-ahead to front-month spread, which continued to incentivise storage drawdowns. Looking ahead, Kpler Insight expects withdrawals to remain elevated, supported by lower-than-average temperatures lifting heating demand in the local distribution sector and persistently favourable short-term TTF spreads.

EU-27 daily UGS change (bcm)

Source: GIE, Kpler Insight. Latest data as of 20 January 2026.

Asia: Ebbing chill in China offsets emerging cold spells in Japan and Korea, keeping prices rangebound

Asian LNG prices rose to $11.34/MMBtu on 21 January, up $1.74/MMBtu w/w, as firmer TTF and cold snaps across Northeast Asia supported market sentiment, driving Asian prices higher despite limited spot activity.

Asian LNG prices are expected to remain broadly stable this week, supported by cold spells in Korea and Japan, lower-than-expected Korean inventories, and sharper pipeline gas declines in Thailand. However, this is largely offset by easing cold conditions in North China, ample Chinese pipeline and domestic gas supply, stronger coal-fired generation in Korea, and warmer Mar–Apr temperature expectations in Japan reducing near-term restocking needs. Japan’s Kashiwazaki-Kariwa unit 6 nuclear power plant restarted on 21 January but shut again on 22 January, in line with our expectations of restricted output before end-February commercial operations.

Cold spells across Japan and Korea are expected to push temperatures below five-year averages next week, lifting heating-related gas demand w/w. In China, temperatures are forecast to return to near-normal levels as cold waves ease, reducing heating demand w/w. Overall, stronger demand in Japan and Korea is expected to be offset by weaker demand in China, leaving Asian gas demand broadly stable w/w.

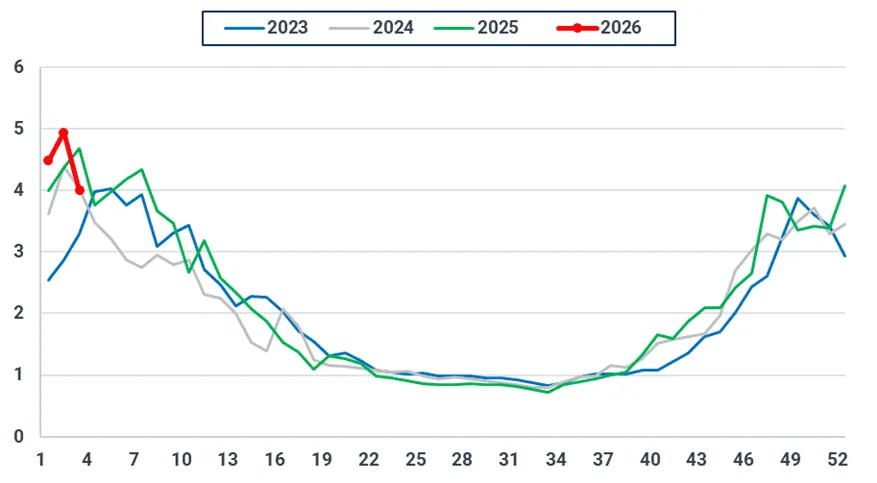

Temperature trend in South Korea (°C)

Source: Meteostat, GFS, Kpler Insight. As of 22 January 2026 00:00:00 UTC. Population-weighted average temperature is shown for both historical and forecast.

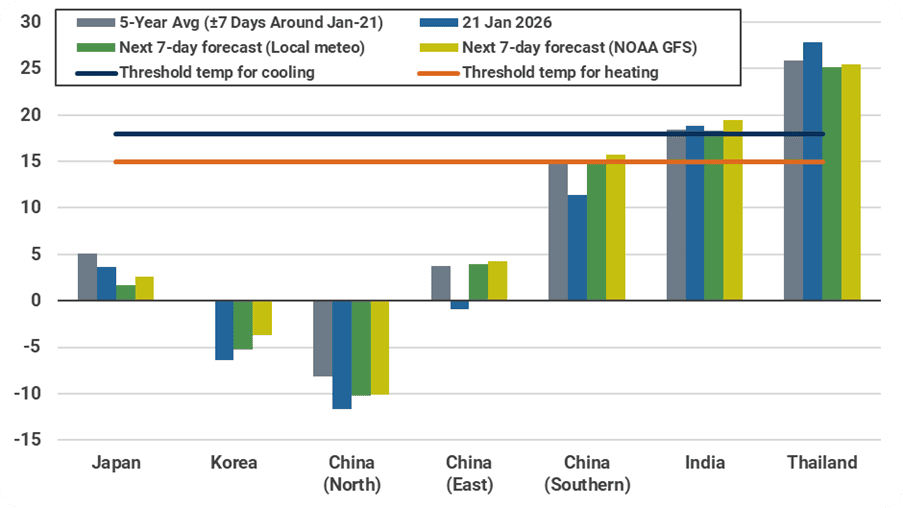

Forecasted average temperatures for Asian countries (°C)

Source: Meteostat, Kpler Insight. As of 22 January 2026 00:00:00 UTC. Population-weighted average temperature of selected major cities across a country is shown for both historical and forecast.

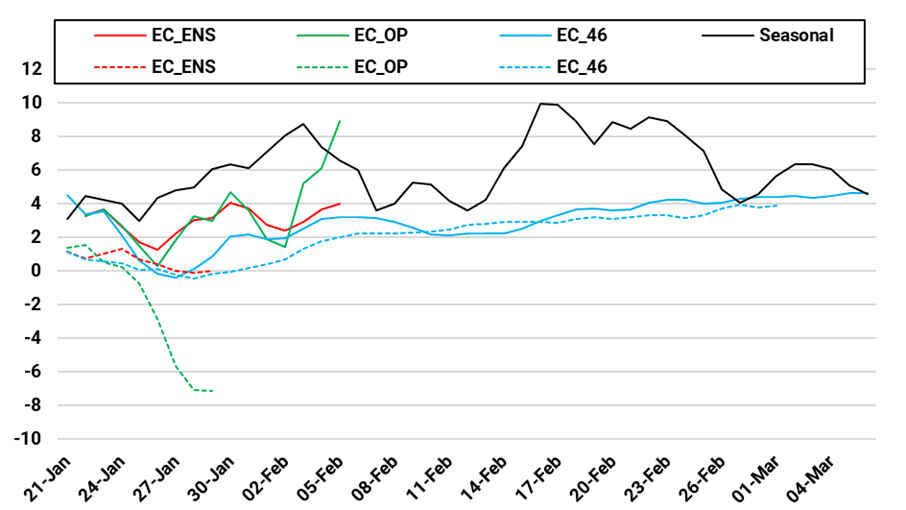

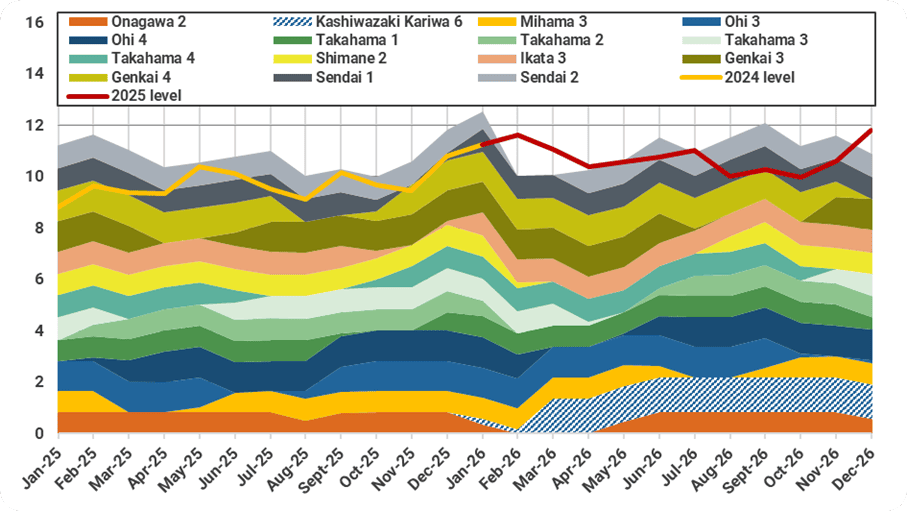

Japan’s METI reported major utility LNG stocks at 2.3 mt as of 18 January, stable w/w and near five-year averages. Latest JMA forecasts of higher temperatures in late winter are expected to offset the gas-for-power demand upside from restricted output from the Kashiwazaki-Kariwa 6 nuclear unit before commercial operation in end-Feb. Implied power-sector LNG inventories are expected to ease to 2.3 mt by end-February, before rebuilding to 2.5 mt by end-March. Above-average March–April temperatures are unlikely to trigger urgent restocking, capping near-term spot price upside.

Japan implied power-sector LNG inventory forecast (mt)

Source: METI, Kpler Insight

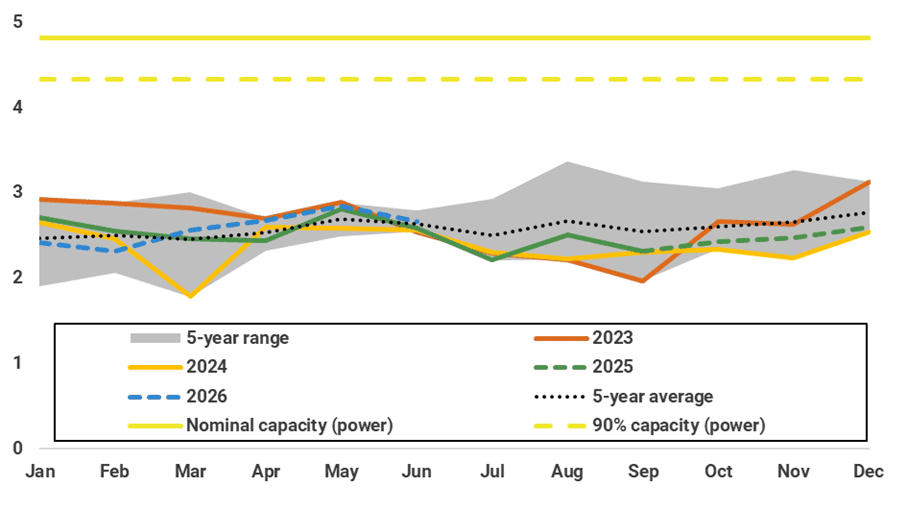

Japan monthly nuclear availability forecast by reactor (GW)

Source: HJKS, Kpler Insight. Note: Dashed area shows the assumed restart timeline and capacity availability of Kashiwazaki Kariwa 6

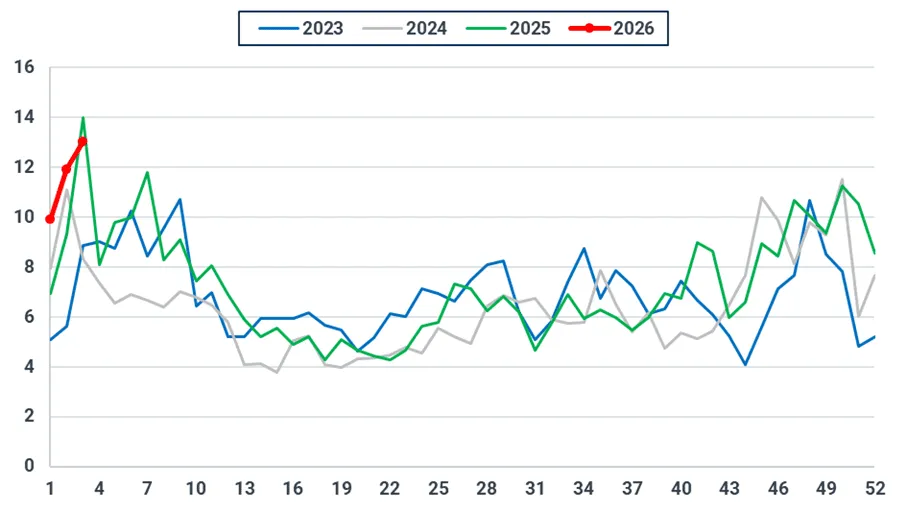

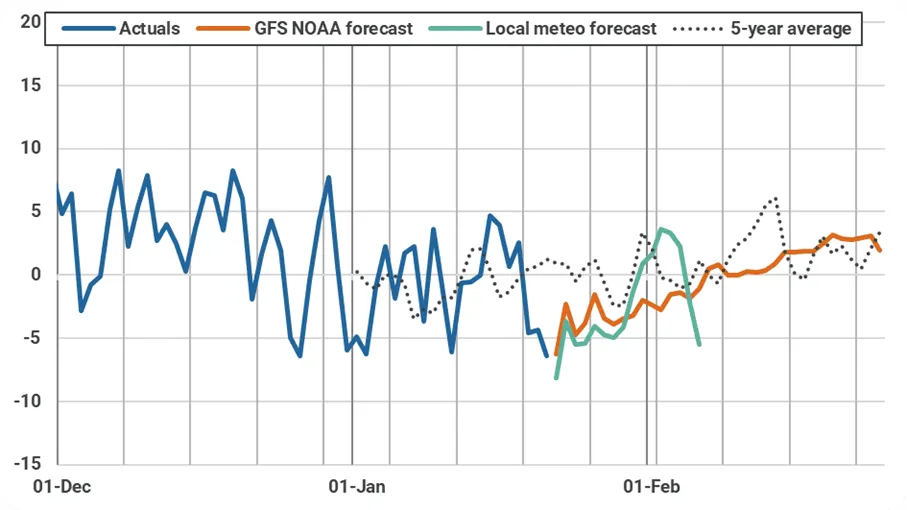

Population-weighted dry-bulb HDDs in Japan (degree-days)

Source: Meteostat, Kpler Insight. Note: 1) Population-weighted HDD of selected major cities across Japan is shown for both historical and forecast. 2) Dry-bulb HDD is based off the actual air temperature measured by a thermometer

In South Korea, ongoing cold snaps are expected to keep heating-related gas demand elevated w/w. However, reduced y/y coal maintenance supports stronger coal-fired generation and caps gas-for-power demand upside, slowing inventory draws through February-March. As a result, implied LNG inventories are forecast to ease to 3.6 mt by end-February before rebuilding to 3.8 mt by end-March, slightly below prior estimates but still above five-year averages, capping regional spot demand and price upside.

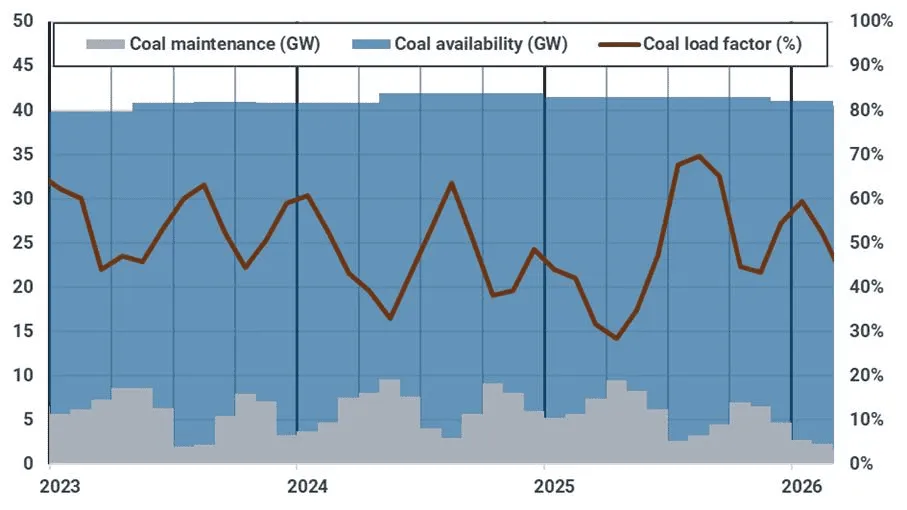

Monthly coal plant maintenance (GW) and estimated coal-fired load factor in Korea (%)

Source: KPX, Kpler Insight. Note: Latest maintenance data is as of 19 January 2026.

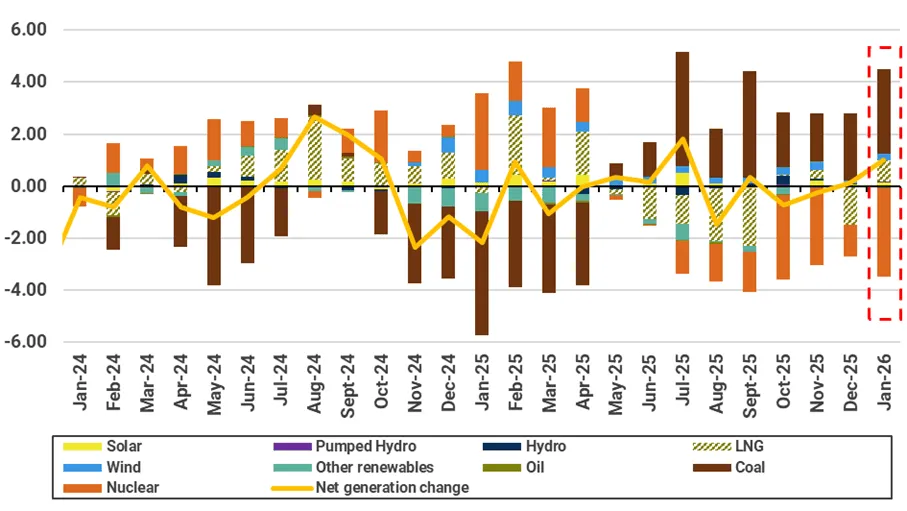

Year-on-year change in power generation by fuel type in Korea (TWh)

Source: KPX, Kpler Insight. Note: 1) Actual data is as of 22 January 2026. 2) y/y changes in January 2026 is our forecast data.

South Korea monthly implied LNG inventory (mt)

Source: Kpler Insight, KESIS

In China, easing Northern cold waves are expected to reduce heating-related gas demand w/w. Ample domestic gas production and pipeline imports, both in line with expectations, are limiting additional LNG demand. As a result, Kpler Insight maintains its view that LNG inventories are expected to ease to 54% full by end-February before rebuilding to 56%, remaining above five-year averages and capping regional price upside. Higher-than-expected Russian LNG inflows reported by China Customs, likely via dark fleet movements, further weigh on spot LNG demand.

Estimated China pipeline gas imports by country between 2020 – 2025 (bcm)

Source: China Customs, Kpler Insight *Note: Data from 2022 onwards are Kpler Insight estimates, as China Customs stopped publishing pipeline gas import volumes by country.

China implied LNG inventory forecast (%)

Source: Kpler Insight

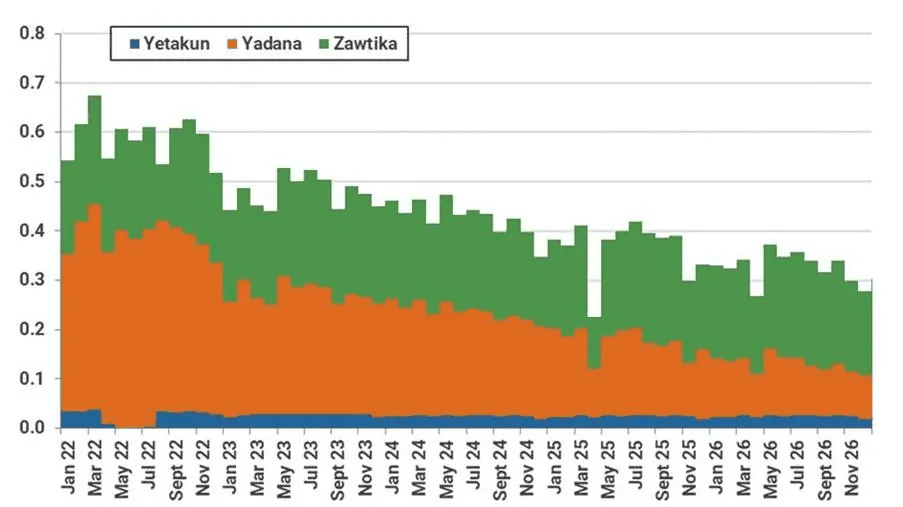

Elsewhere in Asia, latest EPPO data points to steeper-than-expected pipeline gas import declines in Thailand, modestly lifting the 2026 LNG demand outlook. However, any spot demand upside is likely capped by new long-term contracts starting.

Thailand gas pipeline imports (bcm)

Source: EPPO, Kpler Insight. Note: Forecast data starts from December 2025.

US: Henry Hub skyrockets to $5.00/MMBtu as late January forecasts turn frigid

US Henry Hub front-month prices settled at $5.01/MMBtu on 21 January, up 62% from the $3.10/MMBtu settlement a week prior on 14 January. Prices remained subdued through last week after a bearish storage report, strong production, and cold, but unimpressive, temperature forecasts for the final days of January kept Henry Hub prices flat at $3.10/MMBtu on Friday. However, revisions to the US weather model trended considerably colder over the weekend, projecting a prolonged and widespread period of brutal cold for the latter third of January. This shift, coupled with the arrival of wintery conditions over the Martin Luther King Jr. Day weekend, brought bullish energy roaring back into the market. Prices surged to $3.91/MMBtu on Tuesday as demand expectations rose and fears of production freeze-offs grew. Weather models added even more heating degree days (HDDs) overnight, prompting additional buying amid concerns that the severity of the approaching cold could rapidly draw down storage levels.

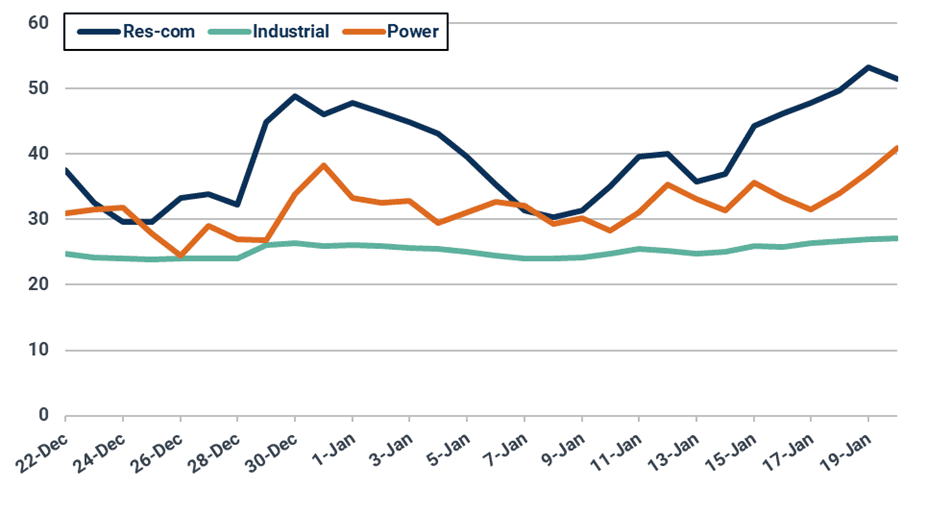

US domestic gas consumption by sector (bcf/d)

Source: EIA

After a mild first half of the month, temperatures began to fall going into last weekend. Residential and commercial heating demand steadily rose over the last 7 days, eventually cresting 50 Bcf/d on 18 January as cold fronts swept across the eastern US. After a brief respite on 22 January, a sustained period of brutal cold is forecast to set in across the eastern half of the Lower 48, including Texas and Florida which have thus far avoided winter’s wrath this season. Heating demand is set to rise well above 60 Bcf/d over the weekend and into next week as much of the US experiences its coldest temperatures of the season. The cold will also likely decrease LNG feed gas demand, with deliverability into Gulf Coast facilities impacted by both production and pipeline freeze-offs.

Henry Hub front-month prices are likely to remain elevated for much of the coming week as cold temperatures are likely to curtail production in key basins and prompt near-record storage withdrawals. However, Kpler Insight does expect prices to ease going into next week as the February contract rolls off the board and traders begin to look beyond winter. If current forecasts of more seasonal weather patterns in early February hold, prices could fall back close to $4.00/MMBtu. Though storage fears may keep prices elevated even after the near-term cold dissipates.

Forecast of residential and commercial demand (bcf/d)

Source: National Weather Service

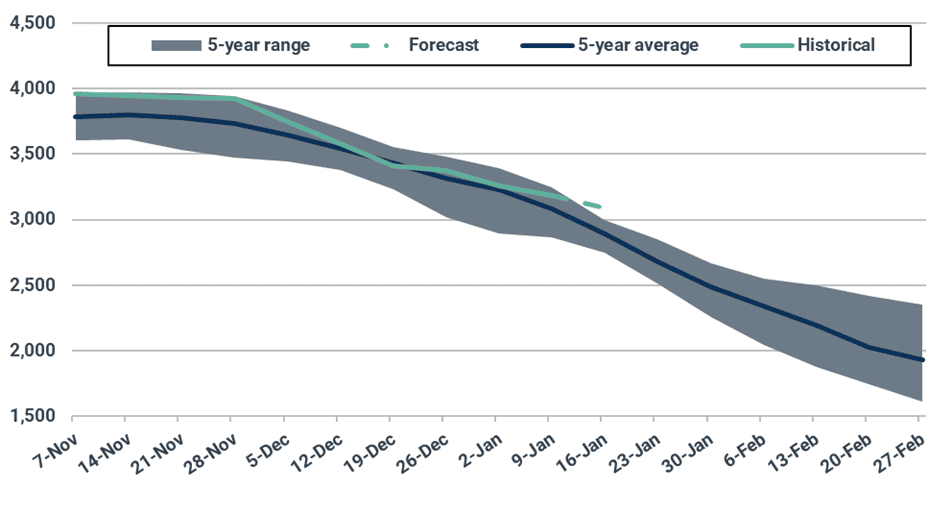

Forecast of heating degree days

Source: National Weather Service

US dry natural gas production averaged 108-109 Bcf/d over the last week, as freeze-offs in some areas reduced output. With upcoming sub-zero temperatures set to extend down to Texas and Louisiana, freeze-offs are expected to be significant as the wells in these regions are not winterized. Freeze-offs in Appalachia are also likely, though to a lesser extent. Kpler Insight expects production to fall to 107 Bcf/d for the coming week.

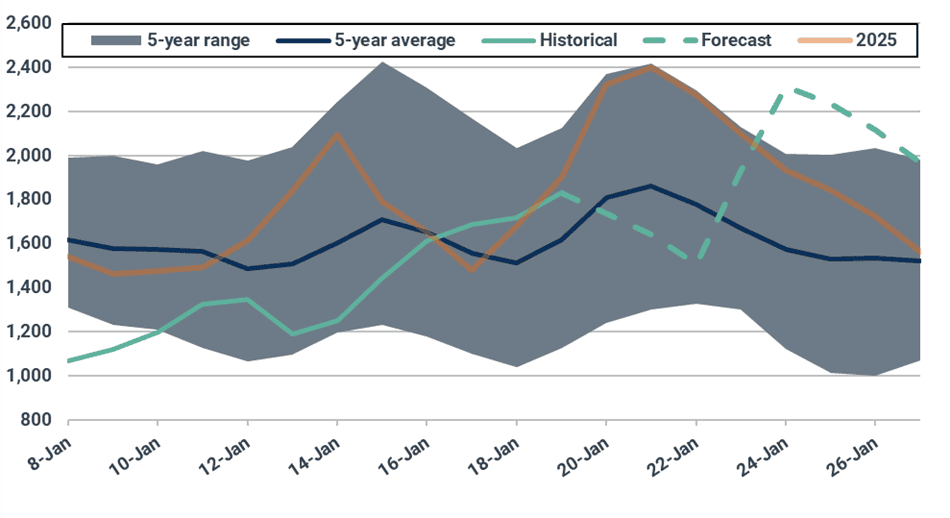

Forecast of natural gas volumes in underground storage (bcf)

Source: EIA

The US withdrew 71 Bcf from underground storage for the week ending 9 January, with widespread above-average temperatures limiting gas demand. This pull proved both bearish relative to the 5-year average and market expectations. Storage levels fell to 3,185 Bcf, a 3.4% surplus to the 5-year average. Kpler Insight projects a 91 Bcf storage pull for the week ending 16 January, reflecting the mild seasonal demand experienced during the period.

Global LNG Supply: US LNG exports to increase, while the first export from Darwin is set to boost Australian volumes

Global exports were stable w/w reaching 9.5 mt, with decreases seen in Australia (-0.5 mt w/w) and the US (-0.3 mt w/w), as some dips in feedgas were noted at the Plaquemines, Corpus Christi, and Freeport plants. This was compensated by slight increases in exports from most other suppliers, including Canada and Norway, who returned to the market after a one-week hiatus.

For the week ahead, we expect higher global supply, as US feedgas nominations recover and Nigerian LNG exports remain robust. In the Pacific basin, the imminent restart of exports from the Darwin plant should help boost Australian volumes. Kpler Insight continues to monitor the progress of the Alexey Kosygin Arc7, which is likely to begin lifting volume from the Arctic LNG 2 plant in the coming weeks.

Global LNG exports (mt, 10-day moving average)

Source: Kpler

In the Atlantic Basin, US exports were expected to rise going forward as feedgas to LNG plants rebounded, after exports declined to 2.4 mt last week, with the arb remaining firmly closed to Europe at ~$1/MMBtu. The US thus continues favoring Europe as a destination for its cargoes, having sent ~85% of its cargoes there in the past two weeks, with strong buying from the UK and Turkey to be noted.

US LNG exports (mt, 10-day moving average)

Source: Kpler

Kpler Insight continues to monitor the movements of Alexey Kosygin, the second Arc7 vessel set to serve the Russian sanctioned Arctic LNG 2 plant. It is currently sailing through the NSR, just behind the Arktika icebreaker that is accompanying it, and is set to arrive at Arctic LNG 2 before the end of the month. Another Russian-linked vessel, Valera, is set to load at the Portovaya terminal, making it the third cargo to load there since international exports resumed in October last year.

In Africa, Nigerian exports have been performing well since the start of the year, reaching 0.44 mt last week. Europe remains the preferred outlet for Nigerian cargoes due to a closed arb, as well as some Turkish LNG demand. Algerian LNG exports however are set to remain intermittent going forward, with volumes hovering around the 0.1-0.2 mt/week. Algeria’s domestic gas balance remains tight, meaning disruptions on the supply side or periods of increased demand can curtail exports.

Nigeria LNG exports (mt, 10-day moving average)

Source: Kpler

Volumes are set to remain stable in the Middle East, with robust Qatari exports reaching 1.8 mt last week with three vessels currently loadings and eleven at the anchorage.

In the Pacific Basin, Australian exports saw a minor drop in volume across most plants, including the GLNG terminal currently under light maintenance until 5 February. Australian LNG exports should pick up again next week with the restart of the Darwin plant, as the Kool Blizzard is currently loading the first cargo there.

Canadian exports continue their return to normal after a week without loadings earlier in the month. Last week exports reached 0.2 mt, while for this week one vessel has already loaded, one is currently docked at the facility and three more are expected to load.

See why the most successful traders and shipping experts use Kpler