Pockets of weakness emerge amid global oversupply

Market & Trading calls

- Heavy crude differentials: Slightly bearish as an expected weakening in Chinese buying and robust output from Venezuela and Canada keep markets oversupplied.

- Medium crude differentials: Slightly bullish as most Russian oil buyers appear to have scaled back trade following the latest US sanctions and the EU’s 18th sanctions package, prompting refiners to seek alternatives from the Middle East and WAF.

- Med light crude differentials: Slightly bullish on CPC Blend differentials as market participants regain confidence in reliability of Kazakh crude supply.

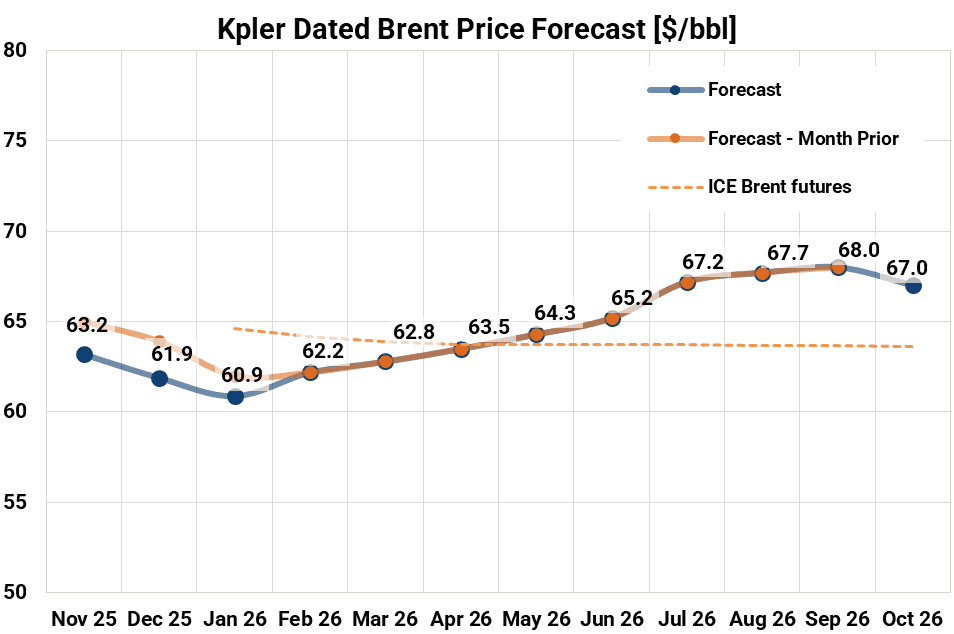

Price forecast: Bearish fundamentals weigh heavier against volatile geopolitical landscape

Near-term volatility received a jolt with the fresh OFAC sanctions on Rosneft and Lukoil last month, but the corresponding price rally remained confined to narrow technical price bands, a theme that has persistent throughout the summer months.

Brent remained in a tight range, with similar geopolitical risks to the upside now supporting a growing glut of oil that is providing serious fundamental pressure to prices.

We have revised our 12-month forecast for North Sea Dated downward to an average of $64.49/bbl, from $64.80/bbl previously. This downward adjustment is concentrated in the near term, and is rooted in the live data supporting our weak Q4 balances.

Q4 2025 is still oversupplied by around 3 Mbd, with oil on water reaching over 5-year highs of around 1.27 billion barrels.

The geopolitical risk premium is still intact, with the US threatening military interventions in Venezuela and Nigeria keeping prices slightly elevated relative to the effect of balances.

Though, the same fatigue around Russian sanctions exists, with the market fading any rally relating to this, anticipating barrels to flow as usual once the re-shuffling of flows normalises.

One key focus for our price forecast has the outsized effect of statistical price bands for flat prices since the summer. There is strong technical support at $60/bbl for ICE Brent futures. Approaching this level should result in a sharp move in either direction, though a trend away from this point would require a strong catalyst to shift the current market narrative.

Looking ahead, we have maintained prices at the back end of the curve. Spare capacity is projected to tighten sharply post-2026, with non-OPEC+ supply growth vanishing and OPEC+ targeting just 2.5–3.0 Mbd of slack. This structural shift underpins our view that the downside for prices beyond 2026 is increasingly capped. Our current forecast accounts for OPEC’s decision for December, as well as the Q1 pause announced.

Nonetheless, one potential weight on the back end of the curve is the resilience of US supply, especially with price spikes allowing producers to hedge their production and lower breakeven costs.

Current data corroborates this, with August US production hitting yet another all-time high at just shy of 13.8 Mbd.

The effect of a potential stronger US dollar with the Fed’s hawkish tone regarding interest rate cuts could weigh on emerging market demand further out into 2026.

Source: Kpler

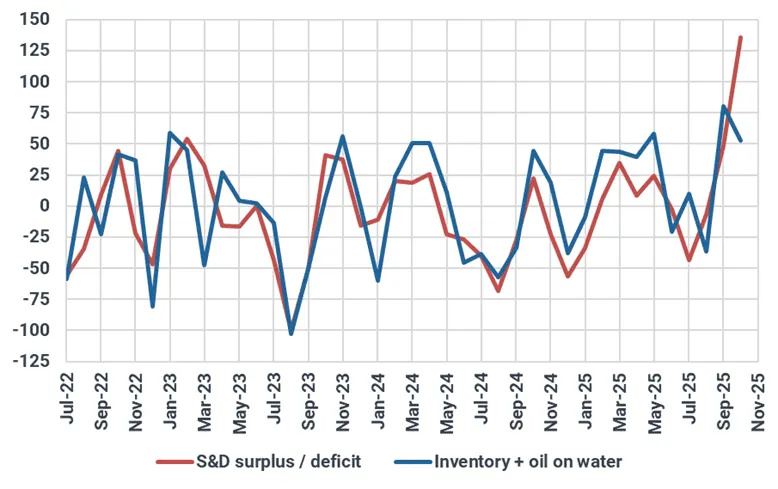

Chart of the Month: Oil on water and slow steaming point to surplus supply

The growing supply glut and the volumes of oil on water have been the principal talking points last month, pointing to the fundamental shift most had anticipated this year, yet these barrels have yet to translate to marked price downside on flat price just yet.

Oil on water touched its highest level in over five years at the end of October, coinciding with the expect supply glut that has been present in Kpler’s S&D forecast for this year. The big spike up to 1.27 billion barrels is now translating into inventories, with the stock build for November anticipated at over 3 Mbd.

The supply glut is also translating to the North Sea, where the anticipated loadings in December are set to reach multi-year highs. Exports of benchmark BFOET loadings should reach five-month highs, though the anticipated ramp up in European refining will be the key factor in seeing whether local differentials gain support (especially at a time of Dangote CDU maintenance), or weigh heavily on Dated Brent and futures pricing.

In conjunction with the swelling oil-on-water figures, a key metric from last month appears to be a dramatic drop in VLCC speeds. The average speed of loaded VLCCs has dropped below 9 knots — the first time this threshold has been breached since July 2022. Slowing vessels typically indicate a deliberate delay - either because the cargo is not yet needed, or worse, because the seller has no firm buyer lined up.

With the growing loadings and tanker speeds, the market seems to be receiving a clear behavioural signal: delivery windows are being extended. This behaviour rarely appears in tight or balanced markets. It typically suggests either a lack of buyer demand or an attempt to manage timing around saturated terminals.

S&D vs inventories + oil on water, Mbbls

Source: Kpler

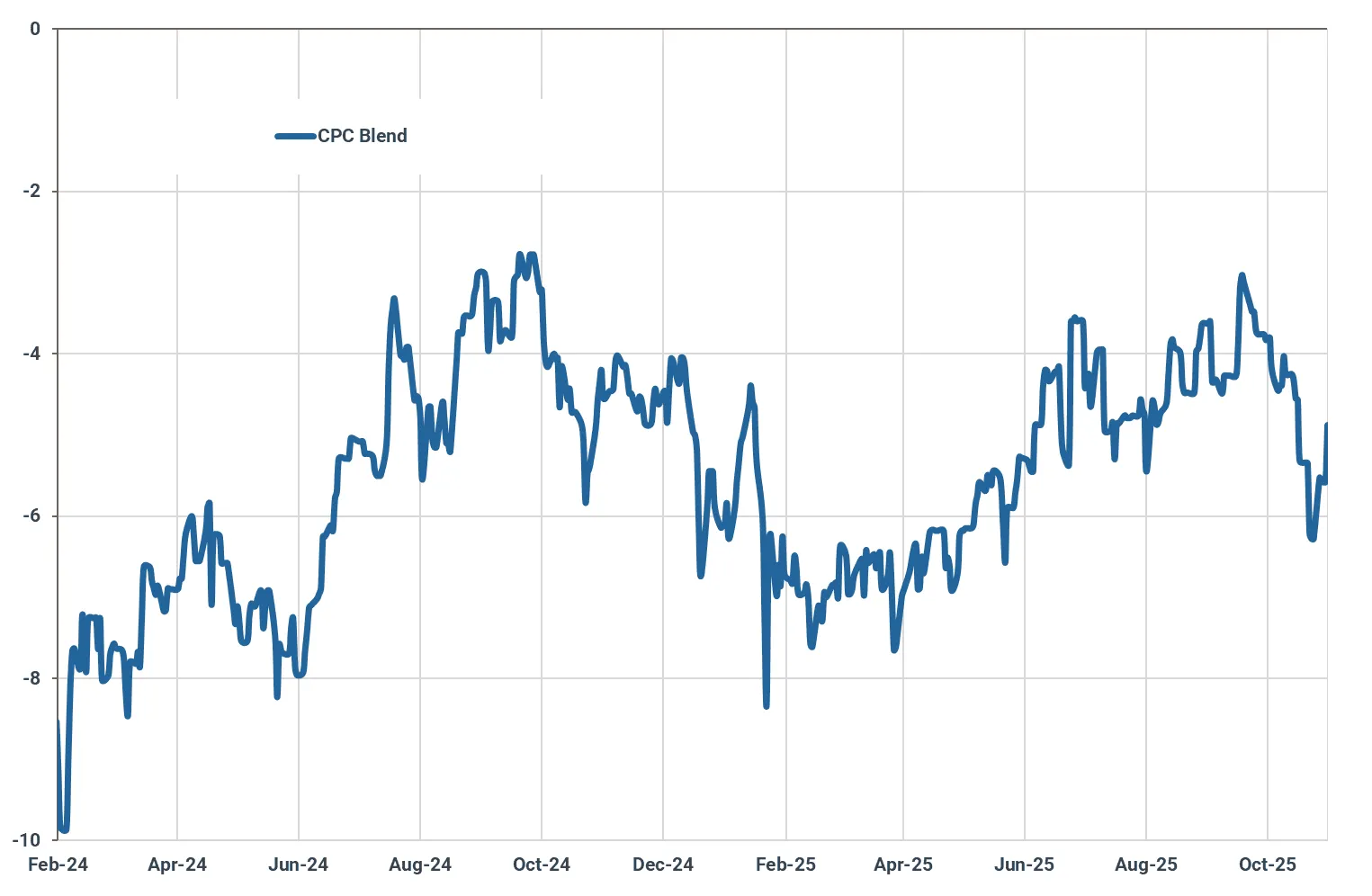

Light crude: Kazakh CPC Blend prices plummet amid supply uncertainty

CPC Blend drops from -$3/bbl discount in September to -6/bbl vs NSD in October

Crude differentials for Kazakhstan’s CPC Blend fell to multi-month lows of around –$6/bbl vs NSD in late October. This marked a sharp reversal from September, when the light sour grade had surged to nine-month highs, narrowing to just under a –$3/bbl discount to Dated Brent. The earlier rally was driven by strong buying interest from Asia-Pacific refiners, supported by a narrow Brent-Dubai EFS that hovered near parity at times, making CPC Blend more economical than alternatives such as Omani crude. The subsequent drop in October was largely due to waning demand amid heightened supply uncertainty. Ukrainian drone strikes in late October targeting facilities near Novorossiysk and Tuapse severely disrupted loading operations at the CPC terminal. In addition, Kazakhstan’s Karachaganak field—a key ~220 kbd producer—implemented a “controlled reduction” in output after a mid-October drone attack damaged a gas processing plant in Russia’s Orenburg region, on which the field is entirely dependent for gas treatment and impurity removal. As a result, CPC Blend exports fell to nine-month lows in October, averaging about 1.3 Mbd (–300 kbd m/m). Over the past week, CPC Blend valuations have started to recover and looking ahead, CPC differentials are expected to rise further as supply concerns ease and as major importers such as India seek alternatives to Russian crude.

CPC Blend differentials vs NSD, $/bbl

Source: Argus Media

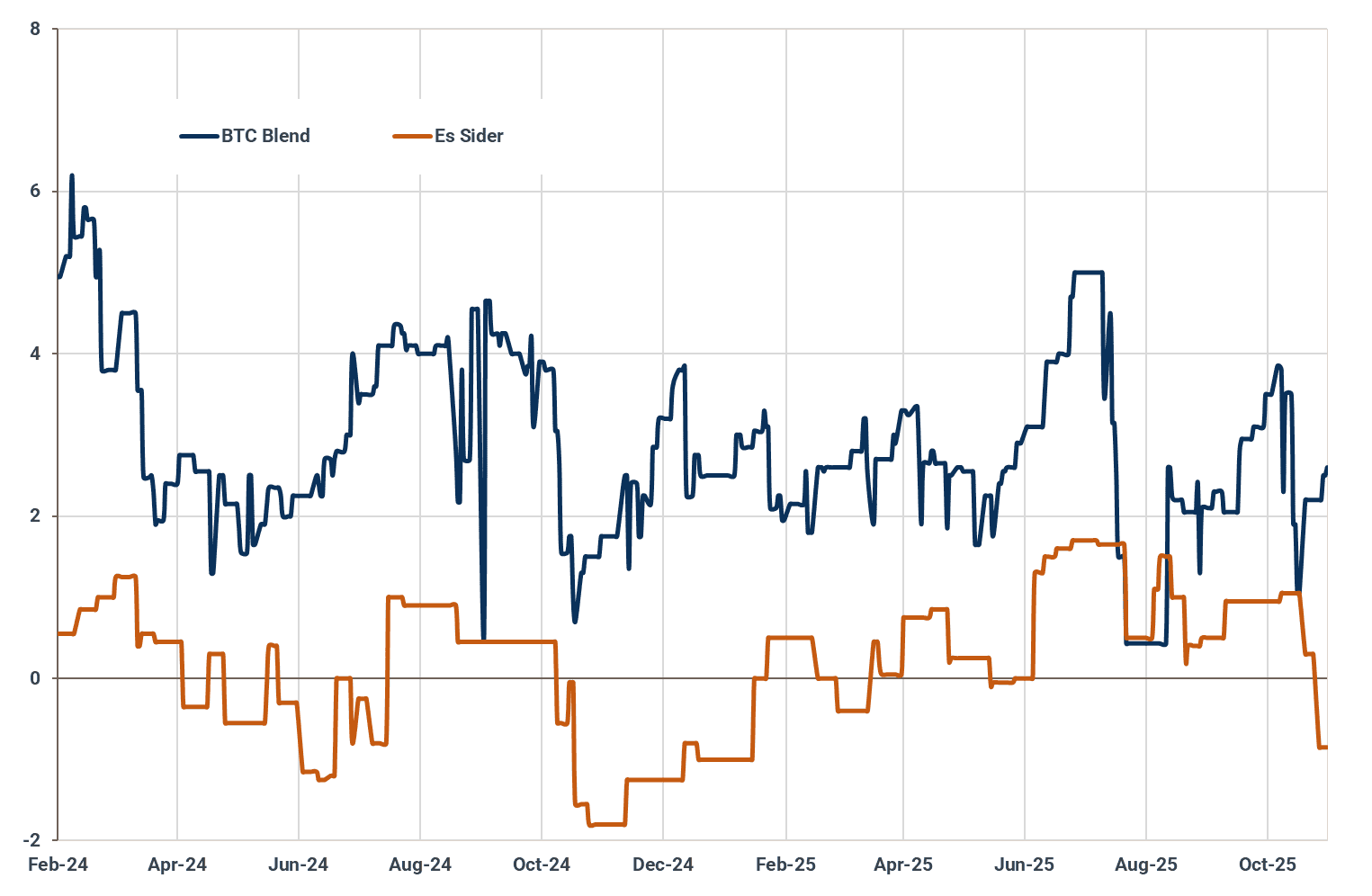

Azeri BTC differentials recover in H2 October

Elsewhere in the Mediterranean, light crude values have also experienced notable volatility. By the end of October, Libyan Es Sider crude fell to its lowest premium to Dated Brent amid abundant supply and rising freight costs. In contrast, Azeri BTC has rebounded over the past two weeks. Earlier in the year, Azeri BTC differentials had been under sustained pressure, reaching four-year lows during the summer after excessive organic chloride levels led to quality concerns. Values began to recover through the second half of August and September as regular buyers gradually returned to the market. However, during the first few weeks of October, BTC differentials softened again, dragging the month’s average lower. Toward the end of October, BTC Blend prices strengthened once more, supported by concerns that the latest U.S. sanctions on Russian crude could tighten medium crude availability. Renewed Indian buying interest also appears to have underpinned this recovery, with reports indicating that Indian refiners purchased November-loading cargoes of Azeri BTC Blend. Looking ahead, we expect the grade to remain firm above $2/bbl for the rest of the month.

Azeri BTC Blend and Libyan Es Sider differentials, $/bbl

Source: Argus Media

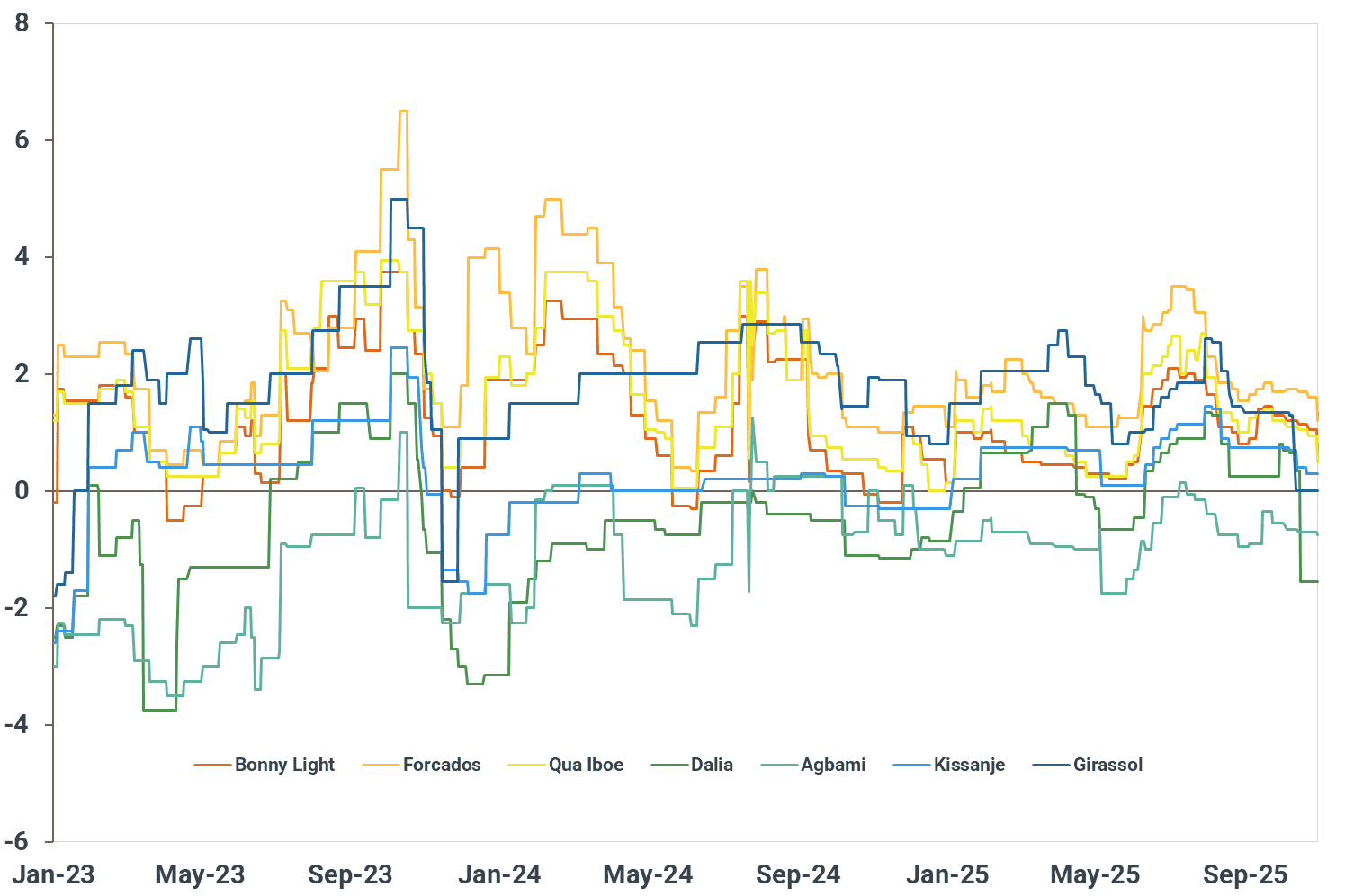

WAF differentials remain pressured in October but a recovery is near

Over the past two months, West African crude differentials have remained broadly stable at subdued levels. Bonny Light and Qua Iboe averaged around $1.00/bbl through October, while Forcados hovered near $1.70/bbl versus Dated Brent (Argus Media). The continued weakness reflects muted European demand and elevated freight costs. TD20 WAF–NWE Suezmax rates climbed from WS 82 in July to WS 111 in September, peaking at WS 123 in October—the highest level since March 2023. Tight vessel availability in West Africa has kept freight rates supported, while record Suezmax loadings from Brazil have lifted rates across the Atlantic Basin more broadly. Nigerian differentials have also come under pressure from weaker domestic demand. Crude arrivals at the Dangote refinery have dropped sharply—from 550–580 kbd in July–August to around 380 kbd in September–October—amid unstable operations. Following reductions of $0.60–1.00/bbl m/m in October OSPs (bringing Forcados, Escravos, and Bonny Light to $1.91, $1.82, and $0.89/bbl, respectively), NNPC left November formula prices largely unchanged (Qua Iboe –$0.07/bbl m/m, Escravos –$0.09/bbl, Forcados –$0.03/bbl, Bonny Light +$0.24/bbl). This relative stability may reflect recovering European refinery runs, with EU-27 crude intake rising to 9.6 Mbd (+350 kbd m/m) in November and projected to reach 9.96 Mbd in December.

West African crude differentials vs NSD, $/bbl

Source: Argus Media

Medium crude: US sanctions and OPEC+ strategy lend support to Dubai prices

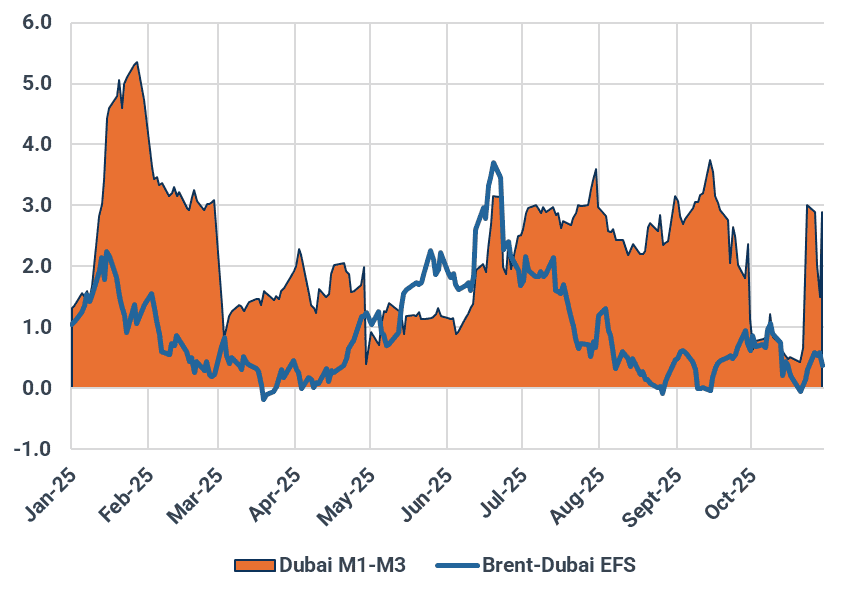

Dubai swings as OPEC supply climbs and geopolitical risks mount

The Dubai structure rode a rollercoaster in October as the market grappled with supply overhang concerns and geopolitical fallout. The Dubai M1–M3 spread plunged to around $0.5/bbl during the first two decades of the month, as rising supplies from OPEC+ nations became more evident. At the same time, U.S. sanctions on a key Chinese oil terminal created logistical snarls for Sinopec, China’s top refiner, likely curbing its crude purchases in the near term. Against this backdrop, QatarEnergy set the term price for its December Al-Shaheen crude at $0.54/bbl following its closely watched monthly tender — the lowest level in two years.

However, the tide shifted overnight after Washington sanctioned Russia’s top two oil suppliers, Rosneft and Lukoil, stoking concerns over tighter supply in Asia as major Russian oil buyers such as India and China scrambled to secure alternative barrels, primarily from the Middle East. The Dubai timespread widened to as much as $3/bbl and held close to that level toward the end of October, according to Argus Media data, buoyed by strong spot-market buying from Indian refiners.

This has effectively driven the average Dubai M1–M3 spread to $1.3/bbl in October, still well below the $2.8/bbl recorded in the previous month, signalling a potential notable reduction in Middle Eastern OSPs for December-loading cargoes. We expect Saudi Arabia to cut the OSP for its flagship Arab Light by $1.2–$1.4/bbl, a slightly smaller adjustment than the change in the Dubai structure, reflecting strong middle-distillate cracks and firmer crude intake demand from Asian refiners. Market participants told Kpler that some South Korean and Japanese refiners may have requested additional December Saudi barrels beyond their term contracts. At the same time, Indian refiners are also likely to seek more term cargoes as they scale back or temporarily suspend purchases of Russian crude.

What could limit the case for a deeper OSP cut is the ongoing OPEC+ quota increases, along with higher Middle Eastern cargo exports following planned refinery maintenance and outages, as well as China’s recent liftings. Over the weekend, the eight OPEC+ members agreed to unwind another 137 kb/d of voluntary cuts in December, though the actual production increase may end up being much smaller. At the same time, they plan to pause the quota hike in Q1 2026, which should help ease the supply glut though not enough to fully offset the oversupply.

Meanwhile, Chinese refiners are unlikely to significantly increase their Saudi term liftings as a whole. While state-owned PetroChina is expected to increase its intake as its refineries complete autumn maintenance — and independent refiners may also seek normal volumes under their 2026 crude import quotas — Sinopec is highly likely to trim its purchases due to the aforementioned U.S. sanctions. That said, Saudi Aramco is expected to keep its OSPs “refiner-friendly” to maintain buying interest — otherwise, it risks facing a supply overhang.

Dubai M1-M3 and Brent-Dubai EFS, $/bbl

Source: Argus Media

Resumed Kirkuk exports drag down medium crude prices in the Med

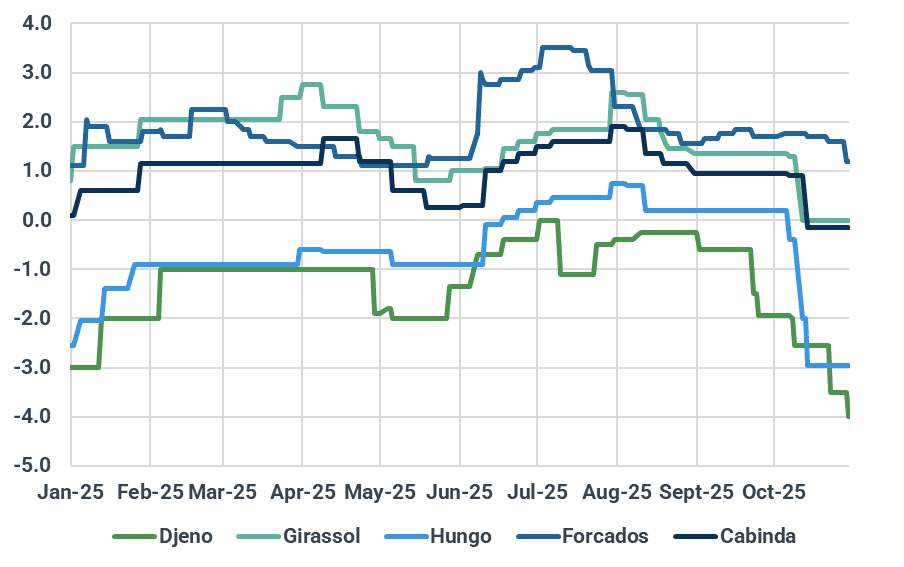

Medium crude prices in the Mediterranean tumbled to multi-month lows in October, as the resumption of Kirkuk flows added further pressure to an already crowded market, just as OPEC+ producers continued ramping up supply. Kurdish crude is currently assessed at -$4/bbl against Dated Brent, compared with -$1.8/bbl in early October, according to Argus Media data. This equates to a $4.4/bbl discount to SOMO’s OSP, reflecting both the abundant supply in the market and the quality compensation. Kpler data shows that recent Kirkuk cargoes have an API gravity of around 29 and a sulphur content of 2.2%, while the Kirkuk OSP corresponds to a crude quality of roughly 35 API. In October, 194 kbd of Kirkuk crude was exported from the Ceyhan port, with one Suezmax cargo bound for the U.S., while the remainder stayed within the Mediterranean region.

Meanwhile, Libya’s medium sweet Es Sider crude slipped to -$0.9/bbl against Dated Brent on an FOB basis, down from a premium of around $1/bbl a month earlier. Kazakh-origin Urals (Kebco) traded at flat against Dated Brent on a CIF Augusta basis, falling from a $2.8/bbl premium in early October and marking its lowest level since January, Argus data showed. The softening prices also coincide with a projected increase in Europe-bound November-loading Middle Eastern crude shipments, driven by rising OPEC+ output, refinery maintenance in Saudi Arabia and Iraq, and weaker demand from China. That said, prices for December-loading cargoes may find a floor — or even stage a modest recovery — as Asian refiners are likely to take more Saudi crude to supplement reduced Russian supplies or support higher run rates. This should, to some extent, ease supply pressure west of Suez. In addition, Turkey’s demand for non-Russian medium crudes is expected to rise, as refiners increasingly diversify their supply sources to ensure compliance with U.S. and EU sanctions.

Selected crude diffs in Mediterranean region (vs Dated Brent), $/bbl

Source: Kpler calculation based on Argus Media data

Sliding WAF medium crude prices near tipping point, but sharp rebound looks unlikely

West African medium sweet crude prices hovered near their lowest level in at least two years in late October, even as U.S. sanctions on Russia’s Rosneft and Lukoil were widely expected to boost demand for alternative grades including Angolan, Nigerian, and Congolese crudes. An overhang of November-loading West African barrels was observed in mid-October as the December-loading program gradually came to market, weighing on spot cargo prices and OSPs for the new cycle. Rising freight rates and increasing competition from the Americas have eroded the economics of West African barrels in both Europe and Asia. Guyanese Liza is currently trading at nearly $2/bbl below Nigeria’s Forcados in the European market, according to Kpler calculation based on Argus data. At the same time, Congolese Djeno is some $0.3-0.5/bbl more expensive than Brazil’s Tupi in China.

Looking ahead, West African crude is expected to find some support in November, as European refiners ramp up purchases post-maintenance and Indian refiners continue to diversify their feedstock sources. However, high freight rates are likely to persist for some time, as the ongoing shift in crude sourcing away from Russian barrels boosts demand for non-sanctioned tankers and increases overall ton-mile demand. Coupled with the sanctions on Sinopec’s main oil terminal in China — which have effectively prompted the refiner to cut run rates and curb feedstock intake — these factors will remain a headwind for West African crude and cap any price gains.

Selected medium-density WAF diffs (vs Dated Brent), $/bbl

Source: Argus Media

Heavy crude: Weaker Chinese buying to weigh on Americas heavy crude markets

Merey crude feels the squeeze from US policy and Chinese quotas

Venezuela's heavy sour flagship grade, Merey, is under pressure, with December-arrival prices widening to $10/bbl against February ICE Brent (Argus Media). This pressure comes amid rising US-Venezuela tensions, which could lead to a potential revoking of Chevron's license, a scenario that would make Venezuela increasingly dependent on China.

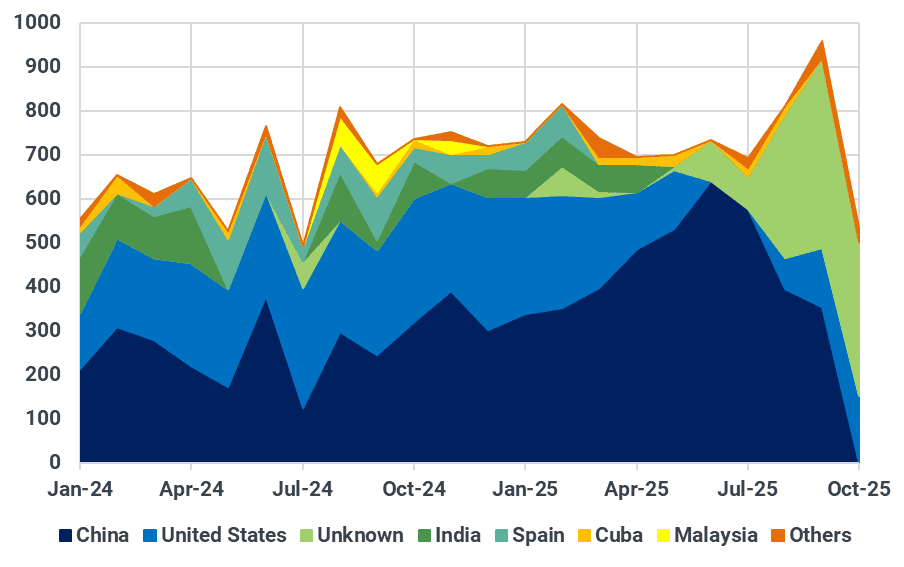

Simultaneously, Chinese demand for Merey remains low, as independent refiners cut purchases, as they near their 2025 import quota limits. This has led to a gradual buildup of sanctioned crude on water (including from Venezuela, Iran, and Russia) in Asia. The buildup of stocks is set to weigh on Merey differentials in the near-term, whilst also keeping a lid on exports, a trend we have already observed last month, with flows falling to 14-month low of 520 kbd, down from multi-year highs of 940 kbd in September.

Chevron is navigating significant geopolitical risk despite securing a new license from the Trump administration this year. CEO Mike Wirth lobbied for the permit, arguing a US exit would cede vast oil reserves to China. The current license is stricter than the previous one, prohibiting direct cash payments to Caracas and requiring Chevron to hand over 50% of its production. This has kept a lid on exports to the US Gulf Coast, which are averaging around 130 kbd, down from 300 kbd in December. This highlights a complex US policy: despite this pressure on Caracas, Washington remains committed to ensuring that energy activity in the region continues under its strategic oversight, demonstrated by its restoration of Trinidad's Dragon gas field license (involving Shell) last month, which now requires mandatory US participation.

Venezuelan crude exports by destination, kbd

Source: Kpler

Canada's heavy sours face headwinds amid record supply and weaker Chinese demand

Discounts for heavy sour crude from the Trans Mountain system has held steady in recent trade, but signs of weakness are emerging, with the January market looking softer, evidenced by a wide bid-ask spread; High TAN bids were last heard around December CMA –$4.75/bbl, nearly $3/bbl below offers (Argus Media). This softening outlook is attributed to a combination of record-high Canadian oil sands production and easing demand in the US West Coast and in Asia-Pacific, with Chinese refiner Yulong reportedly exiting the market for Canadian crude amid and as the Lunar New Year slowdown approaches.

The high output stems from Alberta's oil sands, where heavy production hit a new record of nearly 2.3 Mbd in September, while synthetic production held at an elevated 1.3 Mbd. Output is expected to climb further moving into winter, a period historically associated with less field maintenance and new project ramp-ups. This rising production is tightening pipeline space, corroborated by Enbridge rejecting 4% of heavy crude nominations on its 3 Mbd Mainline for November. On the coast, strong demand from China kept exports from the Westridge terminal supported at roughly 480 kbd in October, offsetting declining flows to the US West Coast, which are tracking at their lowest levels since the TMX expansion began. USWC demand has fallen, tracking the gradual closure of Phillips 66's Los Angeles refinery and a recent disruption at Chevron's El Segundo facility. With demand weakness colliding with Alberta’s oil sands supply ramp up, regional crude differentials are expected to weaken towards the end of the year.

Exports from the Westridge terminal, kbd

Source: Kpler

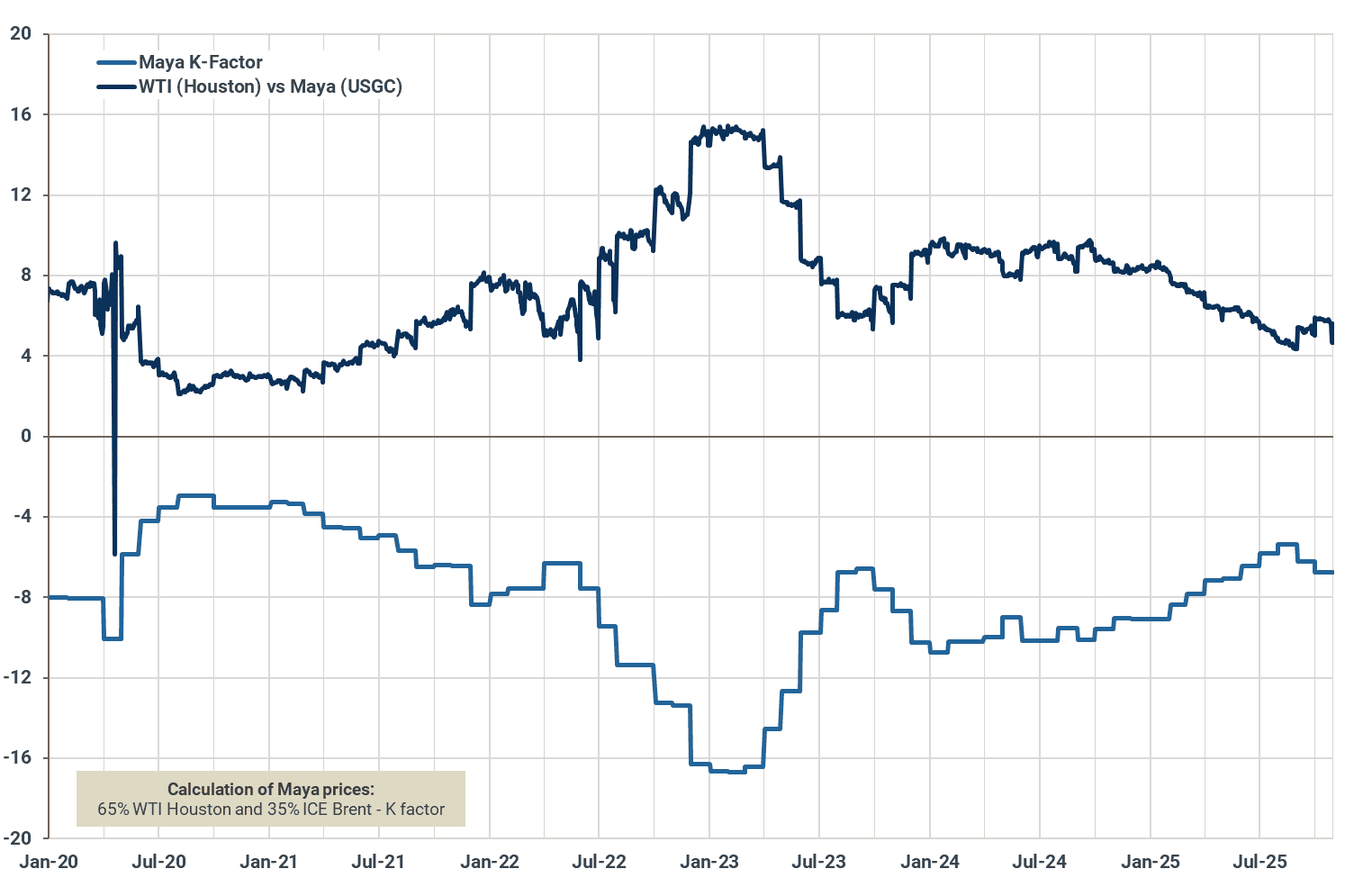

Declining availability of Mexican crude supports Maya prices

Despite pockets of weakness across America's heavy crude markets, arising from high competing heavy crude supply from Venezuela and Canada, Pemex has raised its November adjustment factors (K-factors) for Maya crude destined for the US Gulf Coast by $0.10-0.30/bbl.

The price outlook for Maya is set to remain constructive, as prices are supported by tightening domestic fundamentals. Mexico's crude production remains in terminal decline, limiting availability. Furthermore, domestic refinery is set to rebound sharply. After 600 kbd of primary distillation capacity was offline in October, utilization is expected to recover in November, boosting local Maya consumption. Offline capacity is set to average below 200 kbd, which could help keep domestic throughput robust into year-end.

The volatility in Maya's price is strongly linked to Mexico's underperforming downstream sector. While total refined product output rose 37% year-on-year in September, this masks deep structural weaknesses. The gains came entirely from the new Olmeca refinery (running at ~60% capacity). In contrast, Pemex's six legacy plants averaged just ~50% capacity, their lowest throughput since December 2024. Frequent, unexpected outages at these aging, debt-laden facilities mean domestic crude demand remains unreliable, creating persistent volatility for Maya balances and differentials.

Maya crude differentials, $/bbl

Source: Argus Media

Want market insights you can actually trust?

Kpler delivers unbiased, expert-driven intelligence that helps you stay ahead of supply, demand, and market shifts. Our precise forecasting empowers smarter trading and risk management decisions.

Unbiased. Data-driven. Essential. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler

Expert research & analysis driven by proprietary data