Refinery status monthly - September

Operations: Global refinery outages have climbed sharply in September

Global refinery outages surged in September and are set to rise further in October, driven by seasonal turnarounds and unplanned Russian disruptions.

Global refinery downtime fell to a seasonal low of 5.9 Mbd in August (IIR) but has since risen sharply—driven by unplanned outages in Russia from drone attacks and scheduled maintenance—and is set to climb further in September and October with the fall turnaround season.

Refinery downtime is projected to climb to 7.8 Mbd in September and further to about 8.5 Mbd in October as autumn maintenance peaks. However, the continued pace of drone attacks on Russian refinery infrastructure poses a structural upside risk, potentially pushing outages toward 9.0–9.2 Mbd.

Refining margins remain robust, led by middle distillates. Into Q4, we expect margins to hold as seasonal maintenance picks up and global crude runs ease from August’s high of 84.2 Mbd to about 82.5 Mbd (Q4, 2025, +300 kbd y/y). Elevated margins may prompt refiners to raise CDU utilization before the turnaround season ends to capture gains. We see scope for an extra 300–500 kbd of crude intake—about 100-200 kbd in Europe, 100-150 kbd in the U.S., and up to 100-150 kbd elsewhere—on top of assumed seasonal runs and available capacity.

North America: U.S. refinery runs stay strong but set to ease with maintenance, while Mexico continues to lag

North American refinery downtime averaged ~950 kbd in August 2025 (IIR), up ~60 kbd y/y. Mexico contributed most, with Tula and Minatitlan refineries under maintenance and Dos Bocas offline due to power outages. Downtime is expected to rise to 1.6 Mbd in September and 1.9 Mbd in October, in line with seasonal turnarounds and unplanned disruptions.

In the U.S., downtime remained minimal at ~300 kbd for a third month, with crude intake averaging ~16.9 Mbd in August. Runs were supported by strong margins, tight stocks, lighter crude slates, and ~95% utilization, one of the highest in recent years. BP’s Whiting refinery, hit by flooding, is ramping up. In Q4, Phillips 66's Los Angeles refinery will close operations, while PBF’s Martinez plant should return to full operations after February’s fire, partly offsetting capacity losses. US runs are projected to ease to ~16.5 Mbd in September and ~16.0 Mbd in October, averaging ~16.2 Mbd in Q4 as the maintenance season begins. So far, the Gulf Coast has avoided hurricane-related outages, however, forecasts suggest an above-average season.

Russia: Refining under pressure from drone strikes

Ukrainian drone attacks on Russian energy infrastructure have sharply increased refinery outages, heightening disruption risk across the Russian refining system and the wider FSU. Russian downtime averaged ~1.6 Mbd in August and could rise to ~2.0 Mbd in September (IIR). While not all outages translate directly into reduced crude runs, the strikes have effectively removed ~500–600 kbd of processing capacity, forcing downward revisions to run forecasts. Russian crude throughput was ~5.1 Mbd in August, slipping to ~4.9 Mbd in September, with risks skewed to the downside.

Downtime is projected at ~900 kbd in October , with further upside risk as drone activity shows no sign of easing. For Q4, Russian refinery runs are expected to average around ~5.25 Mbd, assuming gradual capacity recovery, though the outlook remains fragile under persistent strikes.

The attacks have been highly targeted, hitting core processing units such as crude distillation towers, FCCs, hydrocrackers, reformers, and desulfurization systems. This has left refineries prone to prolonged shutdowns, delayed restarts, and unplanned maintenance. The impact has been more severe on clean products than residuals: diesel and gasoline supplies are tightening, straining domestic markets and adding pressure to global balances, while fuel oil exports have so far remained stable.

Reported strikes in August and September include:

- Novokuibyshevsk (160 kbd) – 2 August, 28 August

- Ryazan (376 kbd) – 2 August, 5 September

- Afipsky (155 kbd) – 7 August

- Saratov (150 kbd) – 10 August

- Volgograd (356 kbd, Lukoil) – 14 August

- Syzran refinery (177 kbd, Rosneft) – 16 August and 24th August

- Volgograd Refinery (356kbd, Lukoil)- 19 August and 18th September

- Kuibyshev Refinery (140 kbd, Rosneft) -August 28

- Ilskiy Refinery (131kbd, Kubanskaya Neftegazovaya company) 7th September

- Kirishi refinery (420 kbd, Surgutneftegas) – 14th September

- Saratov refinery (150kbd, Rosneft) -September 16

Middle East: Refinery Activity Stays Strong, Q4 Maintenance to Rise

Middle East refinery downtime averaged ~300 kbd in September and ~340 kbd in Q3, with runs holding near 9.1 Mbd. Downtime is set to climb in Q4 to an average of ~880 kbd, driven by planned works at SATORP, SASREF, and Mina Abdullah, bringing runs down to ~8.6 Mbd.

In Israel, the 197 kbd Haifa refinery restored its CDU-3 in late August after being offline since mid-June following the Iranian missile strike; CDU-1 and CDU-2 had resumed earlier.

Bahrain’s Sitra refinery is advancing commissioning of its residual hydrocracker (RHCK), expected in Q4 2025, though ramp-up will be gradual given the unit’s complexity. Meanwhile, Kuwait’s Al-Zour refinery continues to struggle at 75–80% utilization, as processing heavier crudes deactivates ARDS catalysts quickly and triggers frequent maintenance.

Europe: Heavy October Maintenance to Cut Runs

European refinery downtime was ~200 kbd in August, the year’s low, as refiners chased strong gasoil cracks and pushed runs to a peak of ~12.2 Mbd. Downtime is set to rise sharply to ~850 kbd in September and ~1.2 Mbd in October, reflecting autumn maintenance, particularly hydrotreaters adjusted for winter-grade diesel.

Major refineries offline this fall include Antwerp (362 kbd), Shell Pernis (400 kbd; 200 kbd CDU under maintenance), Sarroch (300 kbd), and Preem Sweden (200 kbd). Greece’s MOH refinery restarted its 140 kbd CDU in August after nearly a year offline due to fire damage.

With maintenance ramping up, runs are expected to ease to ~11.6 Mbd in September (down ~600 kbd m-o-m) and to ~11.2 Mbd in October, before recovering from November as turnarounds wind down.

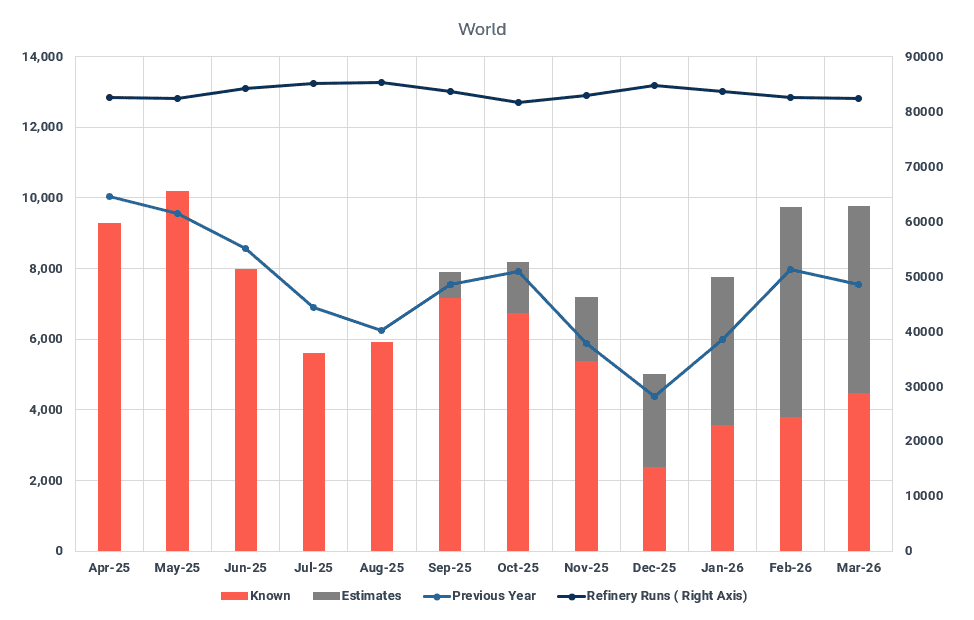

Offline capacity forecast & Refinery runs (Right Axis) in kbd

Source: IIR Energy & Kpler Estimates

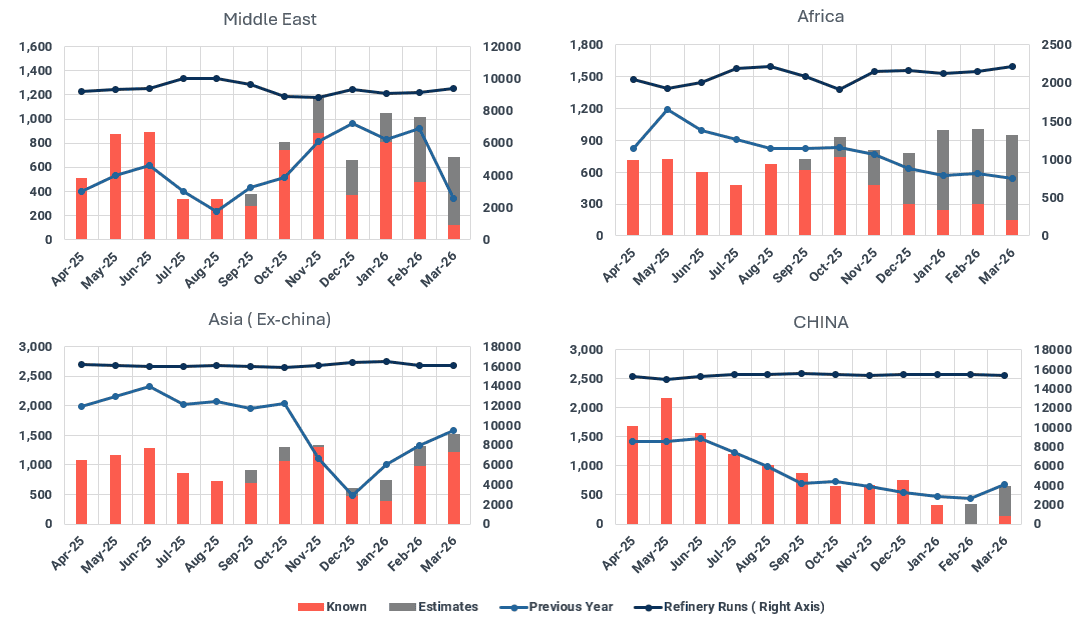

Source: IIR Energy & Kpler Estimates

Source: IIR Energy & Kpler Estimates

Expansions: New refineries and expansions will ramp up through 2025–26, though headwinds persist

Large-scale expansions and new mega refineries coming online will make Asia, Latin America, and the Middle East the main drivers of refining capacity growth in 2025–2026. However, reaching stable, full-scale commercial output of refined products is expected to take an extended ramp-up period

Africa

Nigeria

Nigeria’s refining remains constrained, with Dangote stuck in a maintenance loop, whereas legacy plants are struggling to run reliably.

Nigeria is striving to boost domestic refining capacity, anchored by the ongoing ramp-up at the Dangote refinery—though output remains capped at ~450–470 kbd due to RFCC and operational issues—and revival attempts at state-run plants. The state-owned refineries remain largely offline or only intermittently active. Port Harcourt and Kaduna are still in protracted repair phases with no clear restart dates, while Warri, which briefly resumed in late 2024, was shut again in 2025 after running at just 20–25% capacity, producing mostly residuals. These persistent setbacks underscore the difficulties in restoring reliable state-owned refining, keeping Nigeria dependent on imports in the near term.

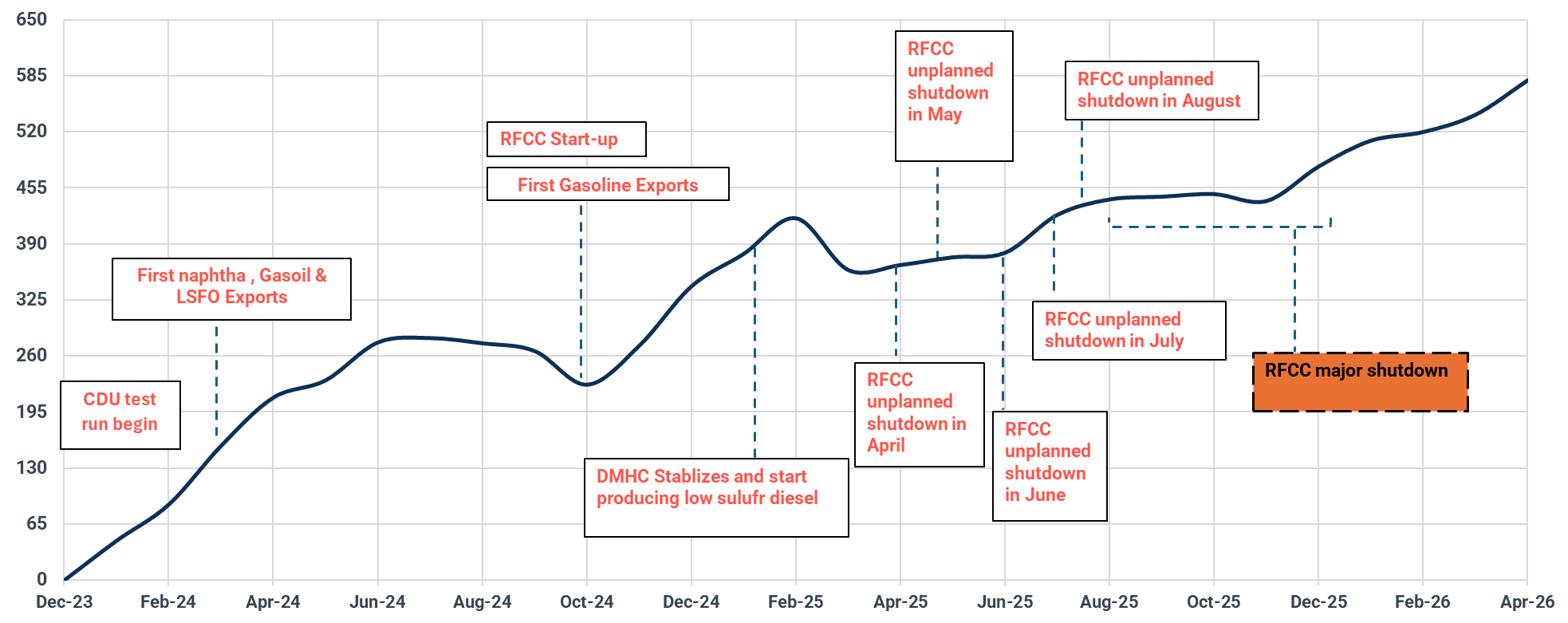

Dangote Refinery-The refinery ramp-up is constrained as the RFCC remains under maintenance

- The 650 kbd Dangote Refinery has made solid operational progress, commissioning all major units—including the reformer, isomerization unit, mild hydrocracker, and RFCC gasoline desulfurization (GDS) unit. However, persistent issues at the RFCC plant have kept the refinery on its back foot.

- To manage bottom-of-the-barrel feed amid RFCC reliability issues, the refinery has maintained a light, sweet, and consistent crude slate—about 60% Nigerian light grades and 35% imported WTI in 2025. The average crude API has held near 38 so far this year, a trend expected to continue into Q4 and early Q1 2026. At the same time, the refinery is adding new regional grades to diversify supply and reduce logistical risks.

- Operational forecast: The RFCC has faced persistent reliability issues in 2025, suffering near-biweekly outages since April, and is currently offline until 10 December after repeated problems. Even during ramp-up, the unit has operated at only ~60-70% capacity, with recurring reactor and regenerator failures disrupting stability. As a result, overall refinery runs are expected to ease to ~420–450 kbd versus the earlier ~490–500 kbd. To offset the loss, the refinery is turning to lighter crude grades to keep CDU-linked secondary units active and may also import naphtha cargoes to keep gasoline production up, a strategy used previously to sustain supply. These setbacks have shifted yields, disrupted trade flows, and kept slurry output high, pushing fuel oil production to 85–95 kbd and gasoline production declining to around 100-120 kbd.

- Market Outreach:-Dangote Refinery has steadily expanded its export footprint beyond West Africa, reaching Europe, Latin America, and now the United States. In August, it shipped ~22 kbd of gasoline to the U.S., with another ~16 kbd expected in September—the first such flows since commissioning. As the refinery ramps toward its rated capacity, U.S.-bound exports are likely to grow further, particularly alkylate or low-sulfur gasoline blend stock, which is in strong demand for meeting U.S. environmental fuel standards.

Dangote major unit start-up timeline and crude throughput forecast (kbd)

Source: Kpler

Americas

Mexico

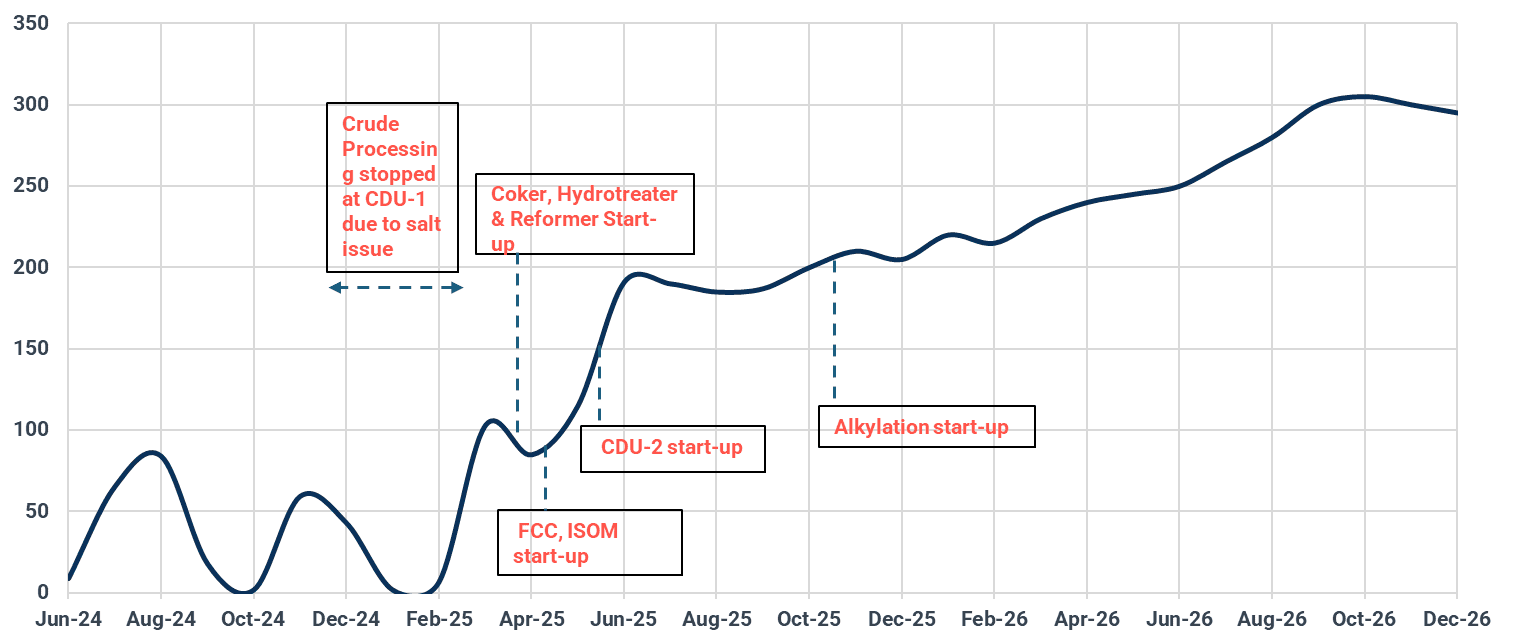

Dos Bocas refinery continues to ramp toward full operations with some repeated setbacks

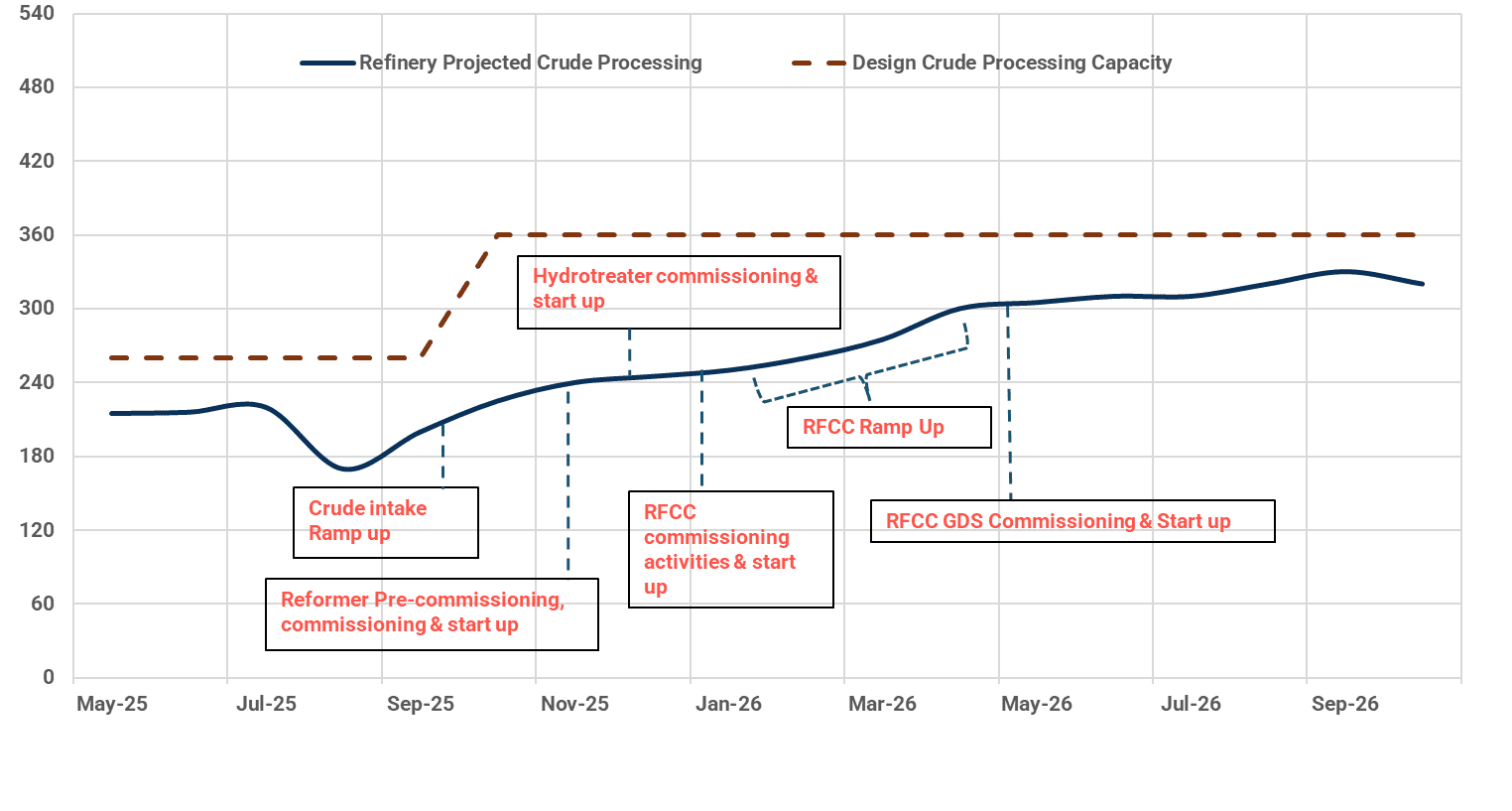

- The refinery features two crude distillation units (CDUs) with a combined capacity of 340 kbd, optimized for processing local Maya crude. Its secondary processing configuration includes a 130 kbd Delayed Coker and a 94 kbd Fluid Catalytic Cracking (FCC) unit, among others. At full throughput, the refinery is expected to produce approximately 158 kbd of gasoline and 142 kbd of middle distillates.

- Operational rates: Since the commissioning of CDU-1 in June 2024, Dos Bocas has struggled to stabilize operations, facing a major setback in December 2024 when salt contamination in the crude feed halted processing. Operations resumed in late February 2025 with a gradual ramp-up, though Pemex data showed utilization at only 56% in June and 45% in July. Another power-related shutdown in late August 2025 highlighted ongoing vulnerabilities, yet the refinery has also shown encouraging momentum, with crude processing ramping up faster than expected in recent months. Notably, reporting output of only finished gasoline, diesel, coke, and LPG at this stage is unusual for a startup but reflects its configuration and testing strategy. While such progress points to resilience, persistent operational headwinds could slow its trajectory. Looking ahead, we expect Dos Bocas to reach 70–80% utilization in 2026, a milestone that would significantly bolster Mexico’s domestic fuel supply.

- Distribution Bottlenecks and Logistics: As Dos Bocas ramps up, moving its output to market remains as difficult as the startup itself. Limited pipeline links to demand centers have created a structural bottleneck, forcing reliance on trucks and coastal shipments. Without new infrastructure, these constraints will cap its effective utilization and delay the refinery from reaching full potential

Dos Bocas Refinery estimated ramp-up and commissioning sequence (kbd)

Source: Kpler

Middle East

Bapco’s Sitra refinery revamp wraps up the latest wave of Middle East refinery megaprojects, following Kuwait’s Al-Zour, Oman’s Duqm, and Iraq’s Karbala, Baiji, and Basrah sites. With no major new ramp-ups expected until 2027, Bapco’s upgrade is the region’s refining finale, for now.

Bahrain

Bapco’s Sitra Refinery

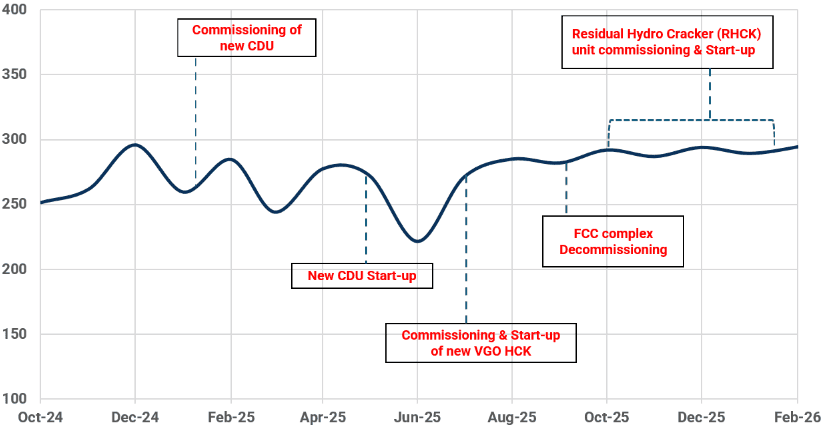

- Bapco is expanding capacity from 267 kbd to 379 kbd by replacing older units with more efficient ones, including a new 60 kbd RHCK and 56 kbd HCK. The upgrades will lift middle distillate yield from 58% to ~70%, adding 115–125 kbd of jet and diesel, while cutting fuel oil output by 30–35 kbd and reducing heavy bottoms yield from 17% to just 3–4%.

- The refinery has commissioned its 225 kbd CDU6 and 40 kbd diesel hydrotreater, both now operational at reduced rates. The 58 kbd VGO hydrocracker and 65 kbd residue hydrocracker (RHCK) remain in commissioning, with the VGO unit expected online by Q3 2025 and the RHCK by late Q4 2025.

- The RHCK (LC-Finer) unit, designed to convert vacuum residue into high-value products, is expected to take longer to stabilize due to its technical complexity and unique configuration, with full operations anticipated by the end of Q4 2025.

Bahrain’s Sitra Refinery unit commissioning timeline and crude runs forecast (In kbd)

Source: Kpler

Asia

Asia is experiencing a divergent trend in refinery capacity, marked by closures in China (see last section) alongside startups of new refineries and upgrades across China, India, Indonesia, and Thailand.

*The Refinery has commissioned its new CDU in 2024, and other major units except the Resid Hydrocracker.

China: Capacity additions continue, but offsets loom (large)

China’s refining landscape in 2025 is marked by targeted capacity growth, led by the startup of Yulong Petrochemical’s 200 kbd second CDU, Zhenhai’s 220 kbd expansion, and Daxie’s 120 kbd upgrade—all concentrated within SOEs and mega independents. However, gains will be partially offset by PetroChina’s planned shutdown of its 200,000 b/d CDU at Dalian in June 2025. Net annual effective capacity growth is expected to significantly increase by 380,000 b/d in 2025, reflecting the ongoing sector reshuffle.

Panjin (HAPCO), Liaoning

- HAPCO, a joint venture between NORINCO Group (51%), Panjin Xincheng Industrial Group (19%), and Saudi Aramco (30%), is developing a 300 kbd integrated refinery and petrochemical complex in Liaoning Province, China. The project will produce 1.65 mtpa of ethylene and 2 mtpa of paraxylene, in addition to transportation fuels. According to market sources, construction progress has reached 75–80%, with commercial start-up targeted for Q2 2026.

Yulong Petrochemical

- China’s Yulong Refinery has ramped up operations with both 200 kbd CDUs now online, with CDU 1 operating since September 2024 and CDU 2 since March 2025. According to Kpler, combined crude throughput is currently ~ 80 - 90 percent, with CDU 1 running near full capacity. The complex features two 1.5 mtpa steam crackers. The first cracker came online in late-24 to early-25 after CDU 1 was stabilized, while the second is expected to be commissioned in September 2025. The refinery is designed with a relatively low transport fuel yield.

Ningbo Daxie Refinery expansion

- Ningbo Daxie Petrochemical Ltd., a subsidiary of CNOOC, is expanding its refining capacity by 50%, from 120 kbd to 240 kbd. The project includes the addition of key secondary units such as a reformer, hydrocracker, FCC, and hydrotreater. According to market sources, pre-commissioning of the CDU began in late April, with start-up trials in mid-July and full commercial production targeted for Q3 /Q4 2025.

India: Refining expansion on track, delay risks persist

India’s refining capacity is projected to climb to 5.9 Mbd by end-2026 and 6.2 Mbd by 2030, supported by rising domestic demand and export growth. Central to this buildout is the 180 kbd HRRL Barmer refinery, a petrochemically oriented greenfield project slated for H2 2026, which will strengthen regional fuel supply and reduce reliance on petrochemical imports.

While the timeline appears ambitious, we maintain a cautious outlook given the scale and complexity of such projects. Similar megaprojects—including Dangote (Nigeria), Jizan (Saudi Arabia), and Al Zour (Kuwait)—faced execution challenges and schedule overruns despite strong starts.

BPCL Bina

BPCL is expanding its Bina refinery capacity under the Bina Petrochemical and Refinery Expansion Project. The refinery’s crude processing capacity is being increased from 156,000 barrels per day (kbd) to 220,000 kbd to cater to the feed requirement of its upcoming petrochemical complex. A key component of this expansion is the installation of a 1.2 million metric tons per annum (MMTPA) ethylene cracker unit. Upon completion, the facility is expected to produce approximately 1,150 kilotons per annum (ktpa) of polyethylene, 550 ktpa of polypropylene, and a range of aromatic products. Construction is underway, with major contract packages finalized.

CPCL, CBR

CPCL, in joint venture with IOCL, is setting up a 180 kbd grassroots refinery at Cauvery Basin. The project involves dismantling the existing 20 kbd distillation and associated units to make way for a new integrated complex. The upcoming facility will comprise a 180 kbd CDU, 100 kbd Diesel Hydrotreater, 55 kbd VGO Hydrotreater, a Petro FCC unit (INDMAX Technology), a 42 kbd DCU, and a Polypropylene unit.

The project is currently in an advanced pre-construction phase, with long-lead items such as CDU/VDU columns and reactors under procurement.

Indonesia

Balikpapan Refinery

- Indonesia’s Balikpapan refinery upgrade is in its final phase, adding 100 kbd of capacity and lifting total throughput from 260 kbd to 360 kbd. The project includes a 90 kbd RFCC and two CCR units, designed to cut fuel oil yields from ~25% to below 10%

- RFCC commissioning is targeted for late Q4 2025, with catalyst loading starting on 17 August 2025. Full ramp-up is expected by late 2026, potentially adding 100 kbd of gasoline and 35 kbd of middle distillates, easing Indonesia’s import dependency.

- The RFCC is the key unit to watch, as startup challenges could mirror those seen in other large projects such as Dangote.

Balikpapan refinery unit commissioning timeline and crude runs forecast (kbd)

Source: Kpler

Closures: 890 kbd of CDU capacity (Outright) is set to shut down in 2025, marking a notable contraction in global refining capacity

*To be decided

- California is set to see two major gasoline-producing refineries shut down within the next 6–7 months, tightening the region’s fuel supply outlook. Phillips66 has announced plans to cease operations at its 133 kbd Los Angeles-area refinery by the end of 2025, while Valero is set to halt crude oil processing at its Benicia refinery by H1 2026.

- BP’s decision to permanently shut down 70 kbd of crude distillation capacity at its 257 kbd Gelsenkirchen refinery in western Germany in 2025 has been put on hold, with operations continuing for now.

- PetroChina’s 410 kbd Dalian refinery ceased operations and was fully closed by July 2025. A 120 kbd crude unit was idled in Q4 2023, followed by the permanent shutdown of a 90 kbd unit in Q4 2024. The remaining 200 kbd crude capacity and associated downstream units were closed this year, completing the full shutdown.

- The 150 kbd Grangemouth refinery was shut down by INEOS in late April 2025, with the site converted into a product import terminal. As the UK’s only refinery equipped with a hydrocracker, its closure is expected to further widen the country’s middle distillate deficit.

- The 150 kbd Wesseling section of Shell’s Rheinland Energy and Chemicals Park in Germany ceased crude oil processing in April 2025, followed by the decommissioning of the CDU, hydrocracker, and other processing units. The adjacent 190 kbd Godorf section remains operational, ensuring continued fuel supply to the region.

- LyondellBasell, as announced, has permanently shut down its 268 kbd Houston refinery, fully decommissioning all process units as of March 2025.

Market insights you can trust

Kpler delivers unbiased, expert-driven intelligence that helps you stay ahead of supply, demand, and market shifts.

Trade smarter. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler

Research & analysis driven by proprietary data