The French power supply glut

Two features make power markets fundamentally unlike any other commodity.

- A single commodity (electricity) is produced by multiple technologies and fuels, all competing on the same stack.

- The grid (the infrastructure through which electrons flow) must be balanced in real time to avoid blackouts.

The current lack of storage means power markets cannot cushion demand shocks, making the commodity uniquely inelastic and prone to extreme price spikes. Moreover, electricity storage faces hurdles that oil and gas do not: it is not merely a matter of tankage, but of complex economics that make building inventory far harder to monetize.

Yet despite this complexity, the basic commodity logic still applies. Prices are set where supply meets demand, at the intersection of their curves.

In France, that intersection is shifting. The country is witnessing a wave of structural oversupply:

- Renewables are on track for an exceptional year in 2025

- The nuclear fleet can now be considered fully back online after a strong 2024 and the maintenance crisis of 2022.

- With 89 TWh of net electricity exports in 2024, France broke its previous record of 77 TWh set in 2002, according to RTE.

- Domestic power demand remains stagnant

It is important to note that it is easier to unplug than to plug in to the grid: de-industrialization is removing electro-intensive demand from the grid, and the expected ramp-up from data centers has yet to materialize.

Altogether, the risk of a widening supply-demand imbalance, and the associated upside price risk, still dominates.

However, this overcapacity comes at a pivotal moment. France’s historical nuclear fleet is approaching the Grand Carénage: a major maintenance program to extend the lifetime of plants nearing 40 years of operation. Following two nuclear maintenance crises in 2016 and 2022, the choices made during this period will shape the system for decades.

Amid this uncertainty, Kpler Insight is assessing what the French power outlook could look like over the coming years, and what this implies for prices.

The French overcapacity outlook

Kpler LT Super Residual Demand Forecasts in France - Source: Kpler

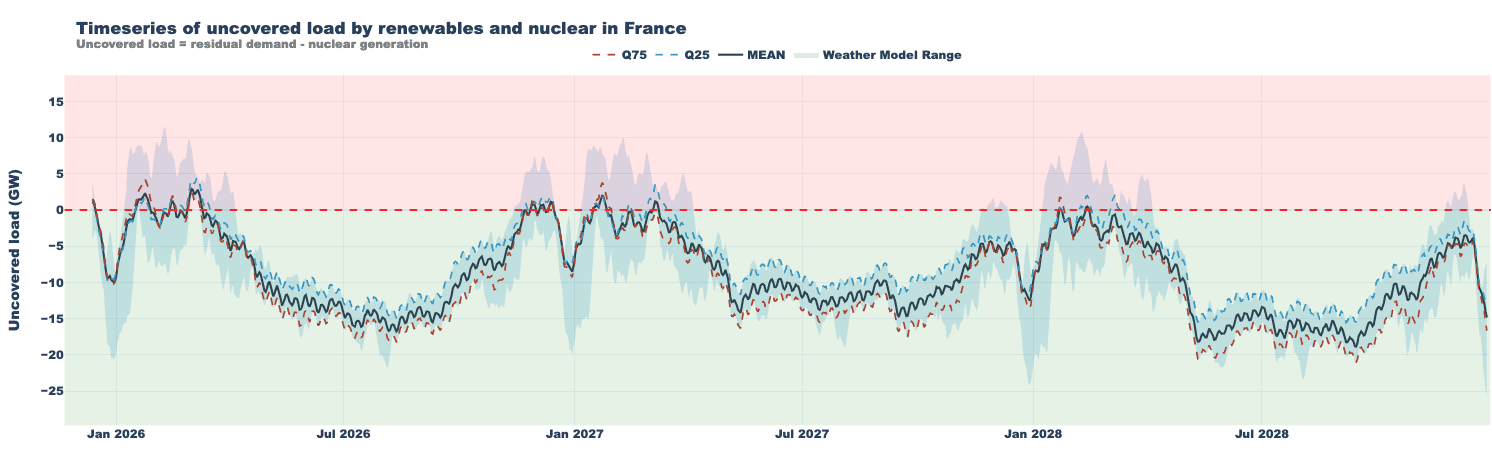

A look at the delta curve between residual demand and nuclear generation highlights periods of uncovered load, that is demand not met by solar, wind, and nuclear, over the next four years, through 2030. The curve hovers above zero mainly during winter, while during summer periods it drops sharply negative, potentially reaching up to –20 GW in Summer 2028. Damping these extremes will be necessary for grid balancing purposes, putting extra pressure on export dynamics, nuclear modulation and renewable curtailment.

Kpler French LT Uncovered Load by Solar, Wind and Nuclear Forecasts - Source: Kpler

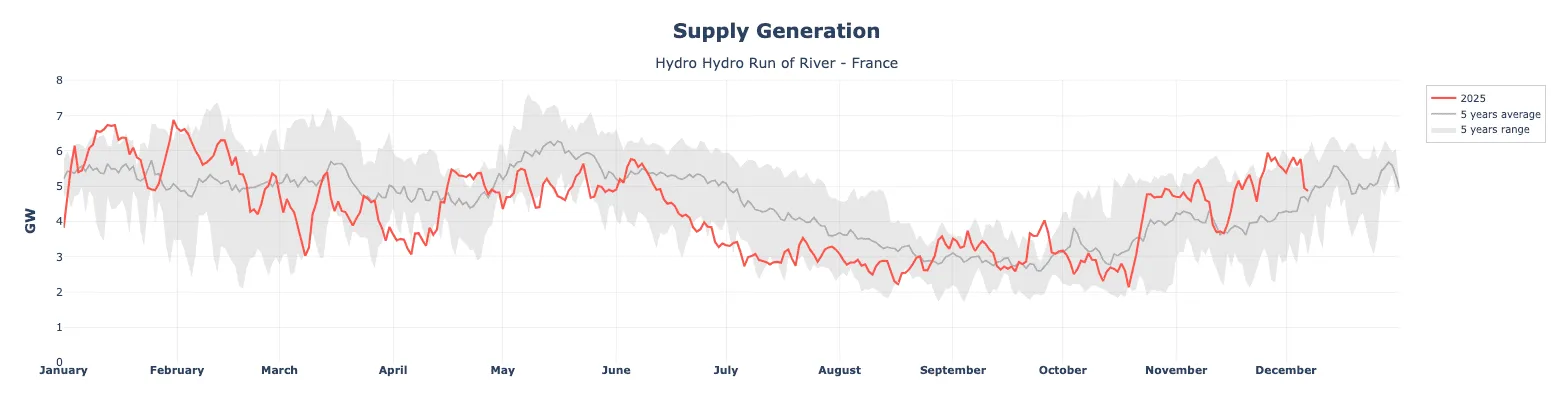

A closer look at the uncovered-load distribution shows a relatively thin but operationally relevant upper tail in the 0–10 GW “tightness” band. This range sits comfortably within the dispatchable envelope of France’s existing hydro and fossil-gas fleet. Firstly, hydro run-of-river, a must-run generation source, delivered more than 5 GW of average output during winter.

Hydro Run of River Generation Historical Trend - Source: Kpler

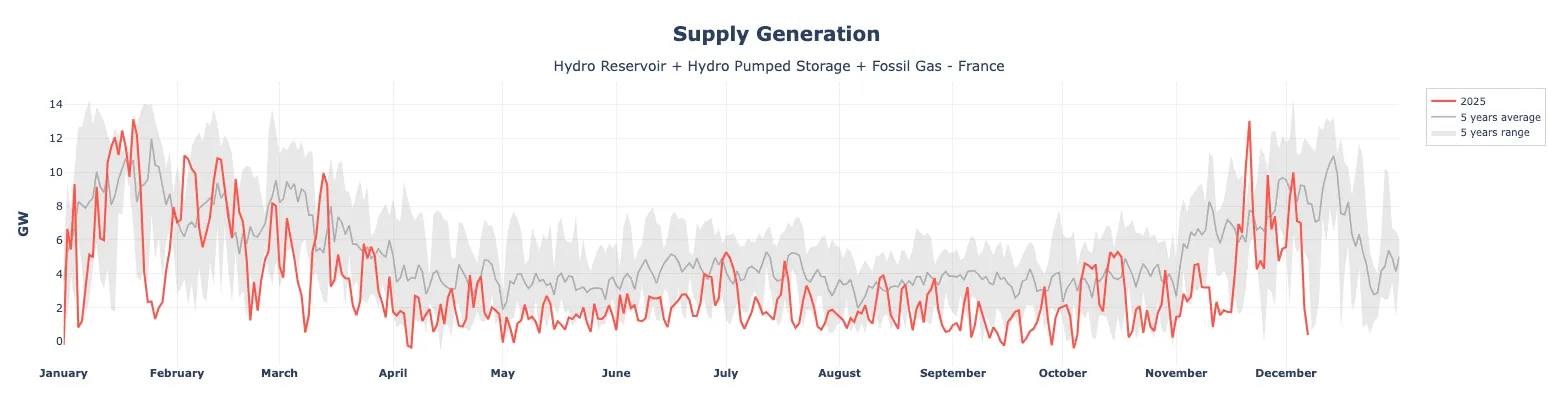

This leaves us with an average 5 GW of uncovered load to be met by pumped storage, hydro water reservoir and fossil gas.

French Hydro (excl. RoR) and Fossil Gas Generation Historical Trend - Source: Kpler

The 3 fuel types have historically been able to supply well above the 5 GW threshold. In fact, historically these technologies supplied around 6 GW on average across winter months in 2025, rising to 7.2 GW on a monthly average in February 2025, broadly in line with the five-year historical average.

On a daily basis, they demonstrated their ability to deliver as high as 13 GW.

The current average fossil gas capacity was 12 GW in 2025 during winter months. Likewise, the average hydro pumped storage and water reservoir capacity in France amount to 13 GW.

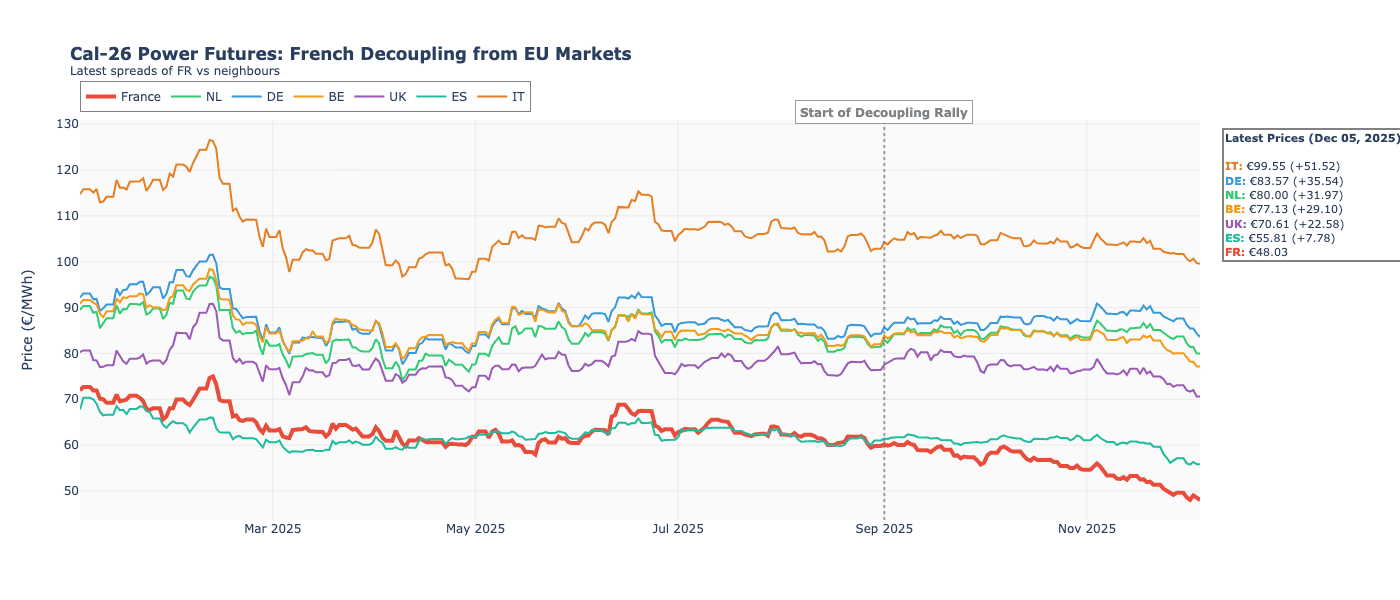

France Cal-26 Decoupling: A Sharp Downtrend Since September

Starting in September 2025, the French Cal-26 contract entered a pronounced sell-off, at a faster rate than any other neighboring Cal-26 product.

Cal-26 Historical Settlement Prices - Source: Kpler

The latest FR Cal-26 settlement (Friday, Dec 5, 2025) stands at 48.03 €/MWh, marking roughly a 60% decline versus prices at the start of the year. This move reflects a market pricing exceptionally strong nuclear availability, reinforced by a solid renewable output year and stagnant demand, none of which is expected to reverse meaningfully in the near term.

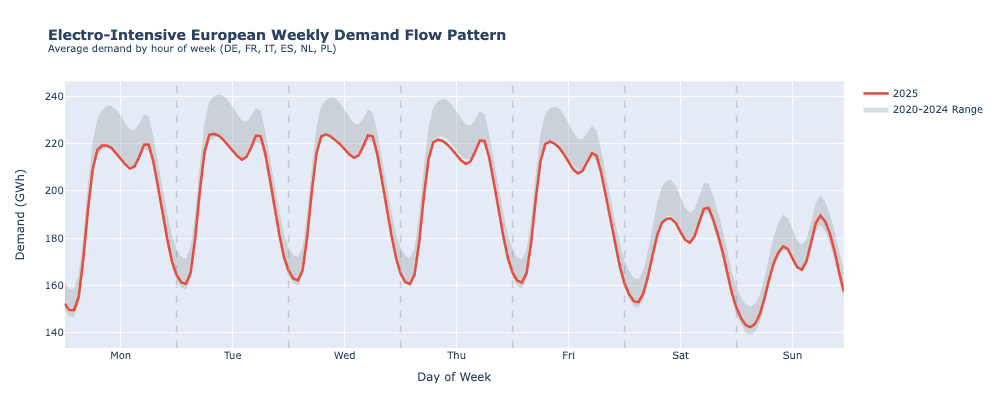

Top Electro-Intensive European (DE, FR, IT, ES, NL, PL) Weekly Demand Pattern - Source: Kpler

In this context, exports are no longer an upside option but a structural requirement for balance. As a result, the Cal-26 downside may not be fully exhausted yet, and the contract could still be searching for its floor. France is faced with oversupply just a couple of years after the extreme scarcity seen in 2022. On December 9th, RTE will be publishing its “Bilan prévisionnel 2025” projection paper, and we expect them to raise concerns on this particularly sensitive topic.

See why the most successful traders and shipping experts use Kpler

Unlock full power market analytics