Assessing the impact on Russian energy infrastructure from renewed Ukrainian drone strikes

With the recent wave of new Ukrainian drone strikes against Russian infrastructure, we are taking a step back to assess what is currently known and draw some conclusions from available data. This special article will be updated when new information becomes available or there are new developments in Russia's struggling downstream industry.

Exective summary

Refinery operations

- Crude throughput slipped to ~5.1 Mbd in August, then down again to ~4.9 Mbd in September, a drop of 300–500 kbd from previously forecast levels and some 400 kbd lower y/y.

- For Q4, Russian refinery runs are expected to average around 5.25 Mbd — steady on paper, but a fragile balance that could collapse in the face of further strikes.

Product markets

- The loss of Russian gasoil barrels is already creating visible shortages in Atlantic Basin gasoil markets, with Brazil and Turkey scurring to find alternative supplies, diverting flows from the traditional net-short in Europe and North Africa this fall.

- There is a clear incentive for WoS refiners to try to keep processing as high as possible this maintenance season, as the drop in Russian gasoil exports is providing a boon for margins.

Upstream

- The Russian crude supply outlook for Q4 is seen neutral to negative. Logistical bottlenecks from refinery attacks and limited spare production capacity will constrain any crude supply upside through the fourth quarter.

- Seaborne crude flows are seen picking up over Q4 as well. Crude displaced from the domestic refinery system will be redirected to the export market. Barrels that cannot find immediate buyers will likely move into floating storage, keeping Russian crude on water volumes robust.

Freight

- Clean and dirty Russian freight rates are moving in opposite directions, with lower product exports pushing clean rates lower, while an increase in crude exports has boosted dirty tanker rates.

- The lower EU price cap is also contributing to tighter vessel supply, with vessels exiting the trade.

Ukraine has intensified its drone campaign against Russian energy infrastructure, with refineries now a central target. The strikes aren’t random — they’re hitting the most sensitive units like crude distillation towers, FCCs, hydrocrackers, and reformers. The result is a downstream system that’s increasingly fragile, where shutdowns drag on, restarts are delayed, and plants are forced into costly unplanned maintenance.

Refinery operations

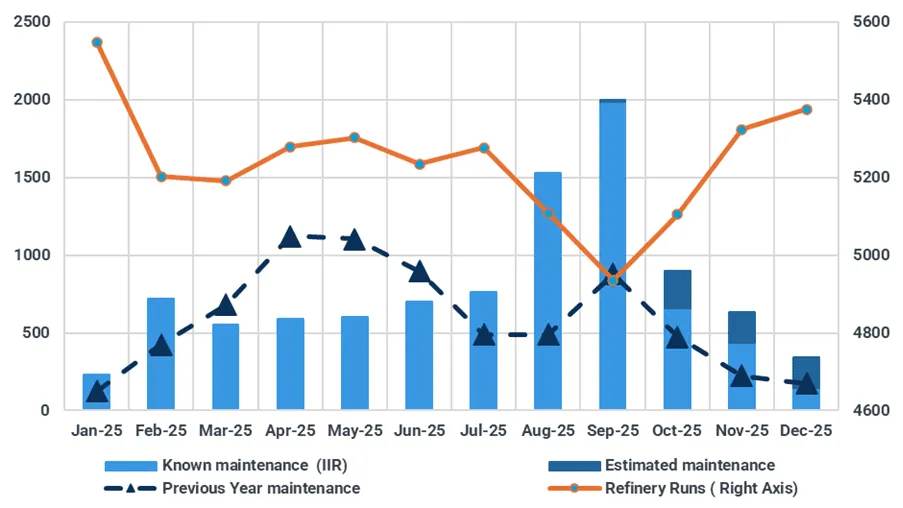

The disruption is already showing up in the numbers. Refinery downtime averaged about 1.6 Mbd in August and could climb to nearly 2.0 Mbd in September, according to IIR estimates. That doesn’t mean every lost barrel is removed from throughput, but the strikes have effectively sidelined ~500–600 kbd of processing capacity.

Reported strikes in August and September include:

Russian refinery operations (kbd)

Source: Kpler

Belarus as a backstop

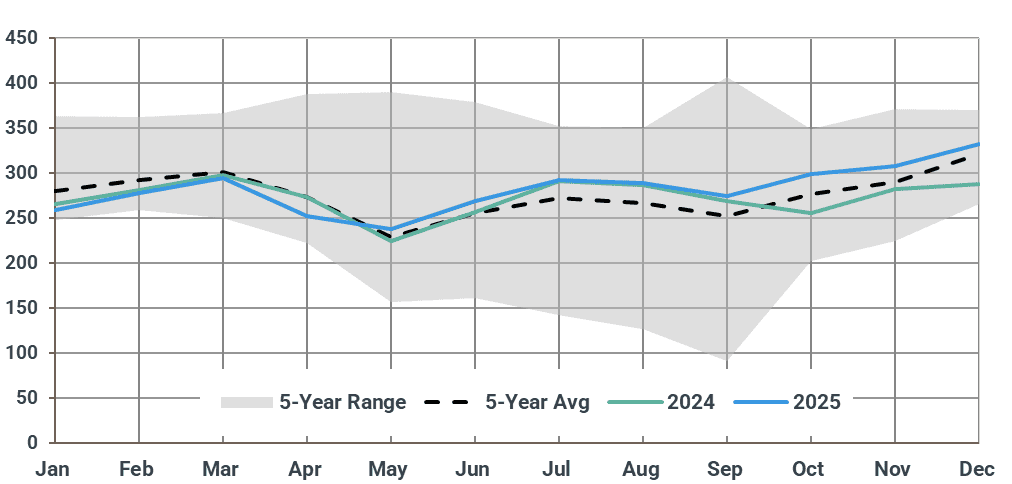

Given the current dynamics, we anticipate that Belarus will move to ease some of the shortfall. Consequently, we have lifted our Q4 crude throughput forecast to an average of 310 kbd (up 40 kbd y/y), representing a 50 kbd upward revision from prior estimates, effectively offsetting part of the lost Russian processing capacity. In addition, we have raised refinery crude intake projections across several European markets (France, Germany, the Netherlands, Greece, Italy, Spain, and Turkey) by a combined average of 160 kbd in Q4, bringing our total European crude runs to about 11.7 Mbd for the quarter. This upward adjustment comes despite seasonal maintenance, with offline downstream capacity in the EU-27 expected to peak at 1.05 Mbd in October, according to IIR data. Nevertheless, refiners are expected to try and sustain elevated utilization levels to capitalize on favourable refining margins in the near term.

Belarus refinery crude intake (Kbd)

Source: Kpler

Impact on product output

The sharpest impact of the strikes is being felt in clean products, particularly diesel and gasoline:

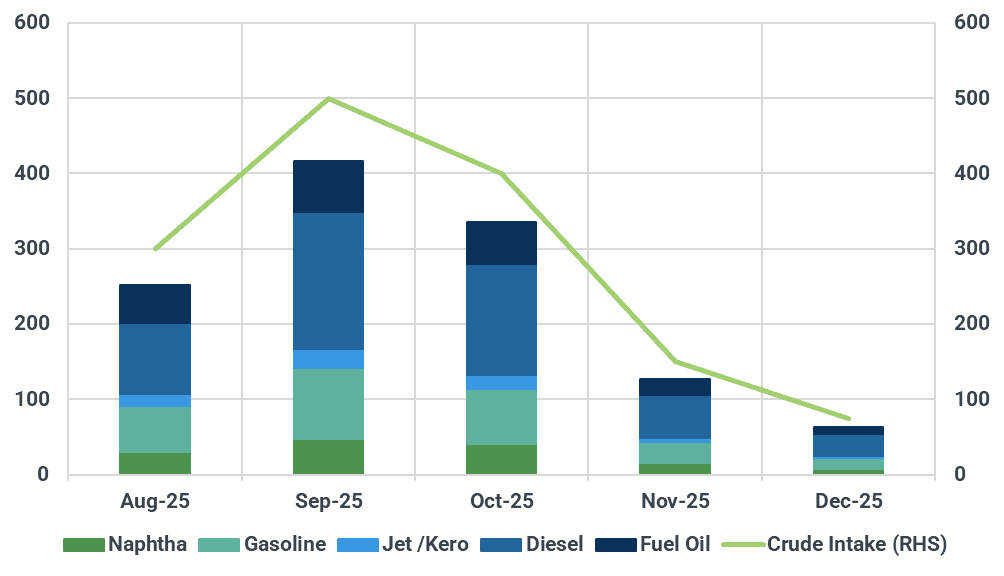

- Gasoil (diesel): Output dropped by 90–180 kbd in August–September and is projected to remain down by around 80 kbd through Q4 2025, all figures are compared to pre-strike estimates.

- Gasoline: Supplies fell by 60–90 kbd in August–September, coinciding with peak seasonal demand from tourism and agriculture. In Q4, gasoline output is expected to remain lower by roughly 40 kbd.

The timing is also unfortunate for Russia — seasonal demand uptick, ahead of the looming winter, colliding with reduced output is creating fuel shortages across several Russian regions, while tightening already stressed domestic balances. Indeed, gasoline prices on the domestic market have already risen over the past weeks but more importantly, several of Russia’s most populated provinces (particularly in the south-western part of the country) are already suffering from acute fuel shortages at the pump, regardless of government regulated price levels.

Lost refinery product output due to Russian refinery outages (kbd)

Source: Kpler calculations based on IIR, own data and analysis

Exports reflect the same pattern, with naphtha and gasoil flows are trending lower(down 80 kbd,m/m), while fuel oil shipments remain steady. HSFO exports surged to 980 kbd in August and are averaging ~ 975 kbd in September, supported by higher CDU activity at simple or previously idled refineries that have stepped in while modern plants undergo repairs. These simple units can take on additional runs, but they add little to clean product supply, turning out mostly fuel oil. Their produced naphtha is probably being redirected into gasoline blendstock units (CCR) to lift output as domestic shortages push prices higher, while kerosene streams are suspected to be flowing into the straight run gasoil pool, leaving no jet fuel available for export thanks to Russia’s winter diesel flash point specifications that allow such blending. With crude flows to these refineries largely locked into fixed supply circuits, flexibility to offset losses at complex sites remains limited.

Product markets

The drop in Russian exports is material at 200 kbd y/y so far in September, with the change most significant in the Black Sea rather than in the Baltic. The biggest effects will be felt in Turkey and Brazil, two substantial shorts in the broader West of Suez market, who have emerged as the principal offtakes of Russian diesel in the wake of the EU sanctions.

This effect has already materialized with a Brazil in the grips of strong agricultural demand pulling additional cargoes from the Middle East and India that otherwise would likely have gone to NWE or Med. In the same vein, Brazil is returning to the USGC in force with September expected to be the first time since February 2023 that the US will supply more than Russia. This has made sourcing cargoes from the USGC for arrival in Northwest Europe more problematic ahead of its maintenance season and keeping seasonal stock builds modest and adding to the pervasive bullishness in the Atlantic basin.

For Turkey balances will tighten with fewer cargoes. However, this has implications for the wider Mediterranean as Turkish gasoil/diesel outflows are currently the lowest since July 2022. With the EU the main recipient of these exports, this further diminishes European supply during the maintenance season.

North African imports, by contrast, are perhaps the least affected, with a substantial grey market in Libya and the surrounding area likely to be impacted first before filtering through into tendered demand. Nevertheless, the Mediterranean is substantially exposed and replacing the cargoes will come from either India and the Middle East - were larger vessels will require STS transfers into more restrictive ports increasing costs – or local refiners.

Upstream

Logistical challenges keep a lid on Russian crude supply

Ukrainian drone attacks have created logistical bottlenecks for Russian crude, causing temporary supply disruptions. While downed refineries have increased crude availability for export, these export volumes have failed to match the full loss in refining capacity. This indicates that the country is facing logistical challenges in re-routing crude flows from damaged refineries to export terminals.

The mismatch between the impacted refining capacity and the rise in oil exports highlights Russia's upstream struggles too. We currently estimate the country's sustainable crude production capacity at around 9.45 Mbd, much lower than the pre-war level of 10.1 Mbd. This is mainly the result of lower capital investment and difficult access to foreign technology, which have made it difficult to combat field decline rates. As a result, output from North-Western Siberian fields, closer to Baltic Sea ports, cannot be ramped-up easily.

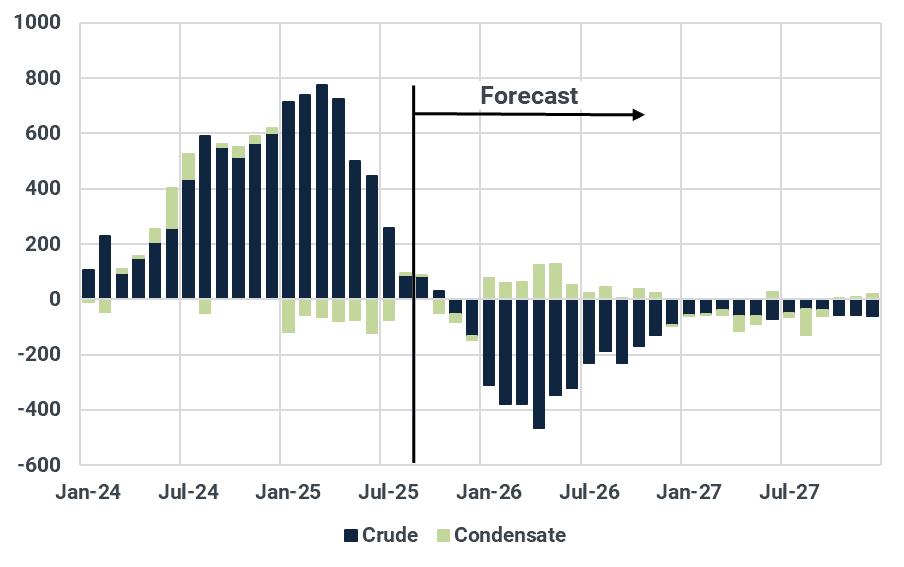

Russian crude and condensate supply change y/y, Mbd

Source: Kpler

Russian crude supply is currently at around 9.15 Mbd, well below its estimated sustainable capacity of 9.45 Mbd. Sustained Ukrainian drone attacks on Russian infrastructure this winter could also pose a critical threat to the nation's long-term crude production capacity. Any forced well shut-ins, particularly in mature Siberian fields, risk causing permanent damage. Freezing conditions can lead to wax and ice blockages, irreversible loss of reservoir pressure, and frozen infrastructure, making a restart of production prohibitively expensive, if not impossible.

While the opacity of Russian reporting is making near real-time assessments difficult, we suspect that if crude exports, floating storage levels, or observed stock levels do not start increasing materially in the next weeks, it would be an indication that Russian crude supply is facing severe headwinds that may limit its capacity to rebound. It is true that the underutilized Transneft pipeline system, which leads crude to the West, could still be used as a temporary storage facility, but this also has its limitations that could not be extended beyond a couple of weeks, as we have seen previously during the contamination issue of early 2019. Therefore, we expect a pick-up in crude departures over the weeks ahead, but will need to reassess the situation once more data becomes available.

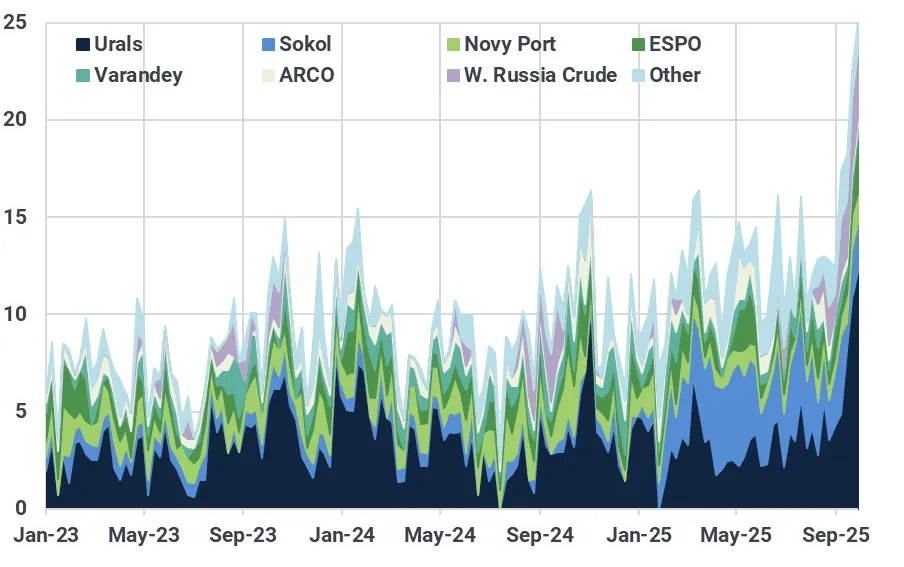

Seaborne exports surge to multi-month highs

Lost refining capacity presents a significant logistical challenge. Crude originally destined for domestic refineries—particularly from inland regions like Volgograd—cannot be easily rerouted to distant Baltic Sea export terminals. Furthermore, adverse weather has constrained exports from Black Sea ports like Novorossiysk, with flows of Russia’s CPC grade declining so far this month.

Despite these constraints, the redirection of crude from downed refineries has propelled Russia’s seaborne exports to their highest level since March. The four-week moving average for September peaked at 3.65 Mbd. Weekly exports even surpassed 4 Mbd in early September—a threshold breached only 21 times since Kpler began tracking in January 2013. This surge has pushed the total volume of Russian crude on water to an all-time high, setting a new record for the fourth consecutive week.

Russian crude on water by grade, Mbbls

Source: Kpler

Floating storage builds as excess barrels are exported

A rise in floating storage, driven by a widening gap between supply and demand, is also boosting the volume of Russian crude on water. Flows to India, Russia's largest single buyer, have slowed to an average of 1.8 Mbd since July—down from a 2.1 Mbd peak in June—even as overall exports rise. This mismatch is forcing a growing number of unsold cargoes into short-term storage at sea.

The volume of crude on idle tankers (stationary for over five days) has swelled to nearly 4 Mbbls, the second-highest level on record. This suggests growing pressure on Russia to find buyers for its excess barrels. This trend is expected to accelerate should further refinery outages materialize. A hypothetical import ban by NATO members Slovakia, Hungary, and Turkey would also trigger a significant build-up in floating storage, though this scenario remains unlikely.

Russian floating storage by grade, Mbbls

Source: Kpler

Freight

Russian clean freight rates fall on weaker demand

Falling product exports has lowered clean tanker demand from Baltic and Black Sea ports. MR rates for Brazil, Middle East and the Mediterranean have all been assessed lower in the last month by Argus Media, with most trading at the lowest level this year. What is notable it that rates have not reached the lows hit last October, when exports were some 200 kbd above current levels.

The decline in clean tanker demand is pushing more of the fleet serving Russia to look for alternative employment, adding to positions lists across the Atlantic, depressing rates on non-Russian routes.

Rising crude exports and lower cap lift Western Russian freight

The increase in crude exports has coincided with tightening vessel supply, particularly in the West. Exports from Russian Western ports are averaging 2.57 kbd so far in September, an 18-month high. While in the East, Russian crude exports have dropped to 908 kbd, pushing the difference in flows between the two regions to the highest point since June 2022.

This has lifted freight rates from Western Russian ports over the last month. Rates for an Aframax from Novorossiysk to west coast India increased $1.80/bbl in the last two months to $10.50/bbl (Argus Media).

In contrast, the slump in loading in the East means rates from Kozmino to China have been flat, widening the spread between the two markets to the widest point since Argus began assessing the routes. The firming Russian freight market in the West relative to the East is a reversal of the situation at the start of the year, when the US sanctioned a record 183 vessels. This heavily affected Aframax supply serving ESPO exports, driving rates in Asia higher. The slowdown in ESPO exports is expected to be short-lived, so it is unlikely we will see a shift in tonnage from East to West seeking higher rates.

An additional factor contributing to the tightness in supply is the advent of the lower price cap at the start of September, which dropped from $60/bbl to $47.60/bbl.

Prior to the new cap, Urals had been consistently trading below the $60/bbl cap, opening access to European owned vessels and services for Russian exports. This was clearly evident in March when 23 Aframaxes and Suezmaxes loaded a Russian cargo for the first time in at least 12 months. Most of these tankers will now likely exit this market. This is both swelling supply for non-sanctioned trade and tightening supply in the Russian market.

The price cap transitions to floating cap next year, which will effectively end the practice of entering the Russian trade on an opportunistic basis.

Russian crude exports and freight rate spread

Source: Kpler, Argus Media

Market insights you can trust

Kpler delivers unbiased, expert-driven intelligence that helps you stay ahead of supply, demand, and market shifts.

Trade smarter. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler

Research & analysis driven by proprietary data