Chevron’s Venezuela comeback will spark heavy crude price correction

It didn’t take long for Washington to reverse its stance on Venezuela, much like many of its policy shifts these days. U.S. refiners will welcome the move, Chinese teapots will feel the pinch, and the heavy crude market is set for flow reshuffles and price realignments.

Market & Trading calls:

- Bearish on Canadian crude prices in both the U.S. and Asia, as heavy crude tightness is expected to ease with the return of Venezuelan barrels to PADD 3.

- Bullish on Venezuelan oil production, with output likely to rebound as access to U.S. naphtha resumes.

- Bullish on Merey prices in China as cargo availability is poised to tighten amid shifting trade flows.

Washington has reportedly reauthorized Chevron’s operations in Venezuela, reversing its decision from just two months ago to revoke the licenses that allowed the company to produce oil in the Latin American country and market the barrels in the U.S. Details of the renewed permission remain unclear, but it is expected to help cool the heat in the heavy crude market — albeit arriving somewhat late, as the peak summer demand season is nearing its end. Nevertheless, it introduces upside risk to global supply just as the market is on the brink of shifting into oversupply by late Q3.

U.S. imports of Venezuelan crude peaked at as much as 300 kbd between late 2024 and early 2025, with the vast majority flowing to the PADD 3 region. On average, volumes reached 230 kbd last year and 166 kbd over the first five months of this year. The most recent Venezuelan crude cargo to the U.S. was delivered to Valero’s St. Charles refinery in mid-June.

Given their refinery configurations and product yield structures, refiners in PADD 3 require medium and heavy sour crude to sustain operations. However, they appear to be struggling to immediately replace Venezuelan barrels, as heavy crude supplies have been tight globally this summer due to strong demand and unplanned outages. Meanwhile, strong HSFO cracks this year have prompted refiners to reduce residual fuel use within their systems and instead boost their intake of heavy crude — further tightening an already constrained heavy crude market. Seaborne crude imports to PADD 3 fell to a four-month low of 1.04 mbd in June and have remained at a similar level so far in July.

The potential resumption of U.S. purchases of Venezuelan crude is expected to trigger a downward correction in Canadian oil prices, both in the U.S. and in Asia. Western Canadian Select (WCS) crude is currently priced near record highs at around -$2.50/bbl against WTI at Cushing, while WCS at Hardisty recently saw its discount widen to approximately -$11/bbl — down from around -$9/bbl in June, but still markedly stronger than the -$14/bbl level seen in July last year, according to Argus Media assessments. As a result, landed prices for high-TAN Canadian crude in China rose to around -$1.50/bbl versus ICE Brent, a sharp increase from -$2.50/bbl last month, despite expectations that crude loadings from the TMX system on Canada’s West Coast would increase in August and September.

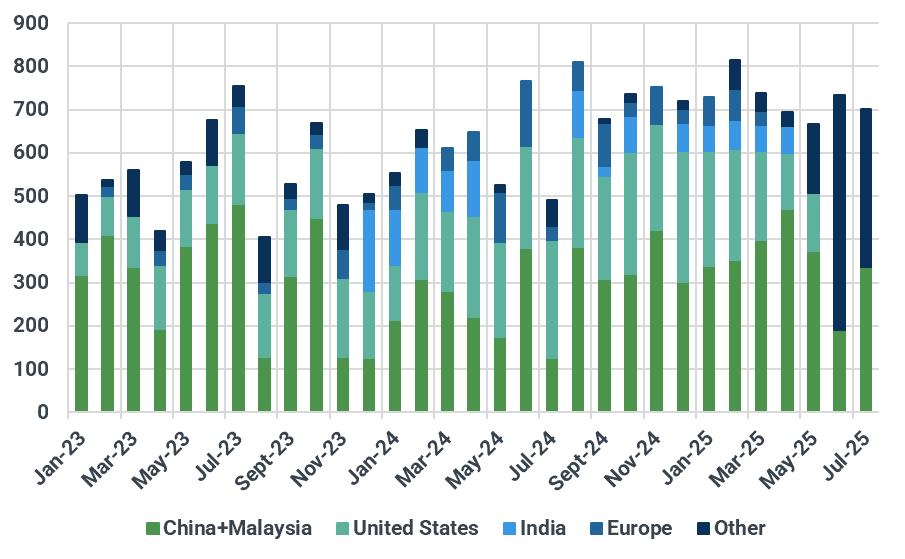

China’s teapot refiners are likely to be the clear losers in the U.S. policy reversal. Since Washington reinstated sanctions, Caracas has relied almost exclusively on China as its primary export outlet, with over 650 kbd of crude shipments in June potentially destined for the Chinese market — a sharp increase from the monthly average of around 370 kbd during the January–May period. That shift has pushed down the price of Venezuela’s Merey crude in China to around -$6.50/bbl versus ICE Brent, from -$5.50/bbl last month. Lower feedstock costs and a higher tax rebate ratio on fuel oil imports were expected to boost teapot refining margins and support elevated run rates. However, the U-turn on Chevron’s license may cloud that outlook, potentially bringing an early end to the summer hurrah for teapots.

That said, the reauthorization of Chevron’s operations in Venezuela is likely to be accompanied by permission to export U.S. naphtha to the country to support upstream activity, suggesting potential upside revisions to Venezuelan oil production. Kpler had previously expected crude oil output from the Latin American country to decline to around 750 kbd by end-2025, down from approximately 940 kbd earlier this year, due to shortages of diluent. So far, Venezuelan production appears to be holding up, supported by pre-stocking of U.S. naphtha in April and May, along with continued purchases of Russian naphtha and likely light crude.

Venezuela’s crude/co exports by destination, kbd (As of Jul 25)

Source: Kpler

Want market insights you can actually trust?

Kpler delivers unbiased, expert-driven intelligence that helps you stay ahead of supply, demand, and market shifts.

Trade smarter. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler

Expert research & analysis driven by proprietary data