Chevron’s Venezuela licence downgrade threatens 200 kbd in output

GL41, the licence allowing Chevron to operate in Venezuela expired this Tuesday, 27 May, following the Trump administration's decision not to renew it. Although the US Major is able to retain its assets, the loss of operational authorisations will result in lost output from the country.

Market & Trading Calls

- Bearish Venezuelan crude: Expect production to decline from 863 kbd in May to 705 kbd by October due to Chevron’s restricted operational licence. ↓

- Bullish Latin American heavy sours: Colombian Castilla and Vasconia as well as Mexican Maya set to tighten as USGC refiners seek alternatives. ↑

- Neutral to slightly bullish Canadian heavy: Expect increased pull from USGC, with potential strengthening in WCS-WTI differentials. →

- Bullish Venezuelan flows to China: PDVSA may redirect ~60 kbd of extra-heavy crude to China long-term, with Merey discounts expected to widen. ↑

The Trump administration’s decision to reinstate restrictions on Chevron’s operations appears strategically timed. With oil prices under pressure and sentiment weak, Washington sees little risk of a market rally in response to declining Venezuelan supply. This allows the administration to maintain a hard stance on Venezuela, tightening immigration and diplomatic narratives, while limiting backlash from consumers or refiners. Over the medium term, however, domestic political pressures, particularly around border security and energy prices, could push the White House back to the negotiating table with Caracas.

Chevron currently operates around 230 kbd of crude production in Venezuela. The US Treasury’s decision not to renew Chevron’s GL41 licence has reclassified the Major’s operations in Venezuela. Effective from today, Chevron can no longer produce, drill, or export oil but retains its stakes in joint ventures, including Petropiar and Petroboscan, under a limited licence resembling its 2020–2022 restrictions. Any form of payment to the Venezuelan state including royalties or dividends remains prohibited.

This shift triggers a substantial operational vacuum. Petropiar, the Orinoco Belt upgrader jointly run by Chevron and PDVSA, relies heavily on Chevron’s technical capabilities, safety protocols, and supply chains, many of which involve US-origin equipment. Chevron’s exit is expected to sharply diminish reliability and throughput at the facility, replicating past patterns where PDVSA struggled to operate upgraders formerly managed with TotalEnergies and Equinor.

In theory, PDVSA could continue running the facility solo. In practice, deferred maintenance, brain drain, and unstable power supply point to an eventual decline in output. Furthermore, PDVSA would require imported diluents, primarily naphtha or light condensates, to maintain crude export quality. Venezuela has already sourced Russian naphtha and may soon seek Iranian condensate, though both imply higher logistics costs and limited flexibility. We estimate naphtha inventories in the country could sustain upgrader activity for another three to four months, at an estimated rate of around 80 kbd of naphtha used as a diluent.

Venezuela imports of naphtha by origin country, kbd

Source: Kpler

Venezuela’s crude output stood at 863 kbd in May, but production from Chevron’s JVs is expected to shrink by roughly 170 kbd. Total Venezuelan production could dip to 797 kbd by June–July, falling further to 705 kbd by Q4 2025. Imports of diluents will need to pick up, otherwise oil production could face a steeper decline by the beginning of Q4.

Venezuela crude oil production, kbd

Source: Kpler

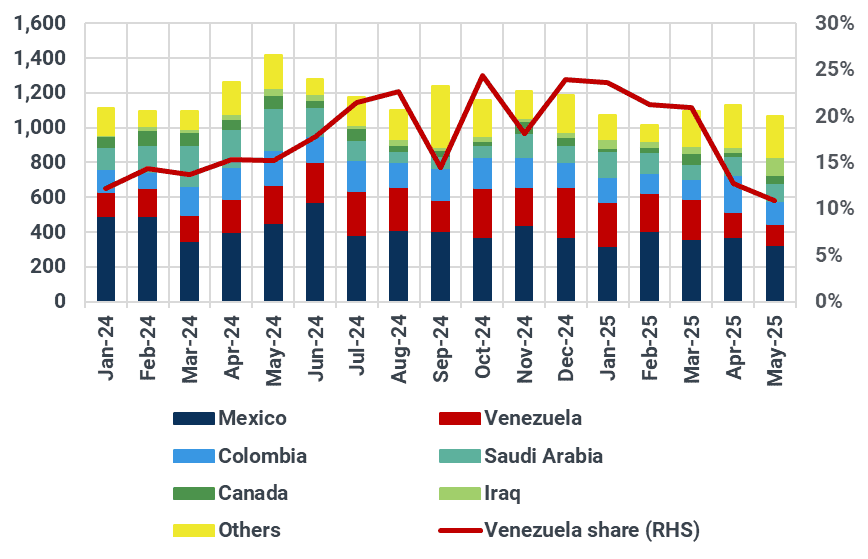

As mentioned last week, this sharp fall will directly affect the USGC, where Venezuelan heavy sour barrels, primarily to Chevron’s Pascagoula and Valero’s St Charles and Port Arthur refineries, represented 11% of total seaborne imports into PADD 3 in May, down from 22% in Q1. In response, we expect Maya to strengthen from a -$6.40/bbl discount to around -$5.00/bbl vs WTI, while Castilla flips from a -$0.46/bbl discount to a premium. Vasconia and Llanos blends are also well-positioned to capture the supply gap.

USGC seaborne oil imports by origin country (kbd, LHS) and share from Venezuela (%, RHS)

Source: Kpler

While PDVSA will reroute remaining volumes toward China, logistical constraints and declining production will limit gains. With a loss of 170 kbd from Chevron-linked assets, up to 60 kbd of extra-heavy crude may be redirected on a long-term basis, deepening the discount on Merey barrels in Eastern Asia.

Want market insights you can actually trust?

Kpler delivers unbiased, expert-driven intelligence that helps you stay ahead of supply, demand, and market shifts. Our precise forecasting empowers smarter trading and risk management decisions - backed by the most accurate oil price predictions two years running.

Unbiased. Data-driven. Essential. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler

Expert research & analysis driven by proprietary data