Qatar’s LNG exports hit a record daily high on 15 June, despite South Pars attack

After an escalation of the Israel/Iran conflict, Kpler Insight takes a closer look at the implications for LNG players in the region.

On 14 June, Israel expanded its attacks on Iran by striking critical oil and gas infrastructure. Among the targets was the South Pars gas field, jointly owned by Iran and Qatar, which supplies feedgas to Qatar’s 77 mtpa Ras Laffan liquefaction facility. Qatar’s LNG exports have been maintained since the attack, however, an LNG vessel carrying US volume to Kuwait has stopped in its track ahead of passing through the Strait of Hormuz.

Market & Trading Calls

- Middle Eastern LNG exports: Stable with no disruption to Qatari or UAE LNG exports. In fact, Qatari LNG loadings jumped to a record daily high a day after the South Pars attack.

- Middle Eastern LNG imports: Potential disruption with one US-laden vessel stalling ahead of passing through the Strait of Hormuz en route to Kuwait. As tensions rise, regional LNG importers—Kuwait, Bahrain, and the UAE—may need to increase their reliance on nearby exporters such as Qatar to secure supply in the peak cooling season.

- Asian LNG & European TTF price impact from South Pars attack: Stable with upside risk. Given the lack of disruption to Middle Eastern LNG exports, fundamentals remain intact with no impact to global LNG supply and limiting the price impact from the South Pars attack. However, prices are experiencing upward momentum due to the Israeli pipeline gas supply halt to Egypt and Jordan. There remains significant upside risk to global gas prices if the Strait of Hormuz is closed or if feedgas supply to Qatar is disrupted.

Israel’s 14 June assault on South Pars targeted Phase 14, where one of the four units caught fire, disrupting operations. This interruption led to an immediate halt of 12 mcm/d of gas supply.

Qatar relies on feedgas from the South Pars gas field; however, there has been no observed impact on its LNG loadings to date. In fact, Qatari LNG supply increased by 143% d/d on 15 June to the highest daily level on record of 0.56 mt. As such, Kpler sees no impact on Qatari LNG exports but supply is being monitored closely. Exports from UAE’s 5.8 mtpa Das Island plant also continue unscathed.

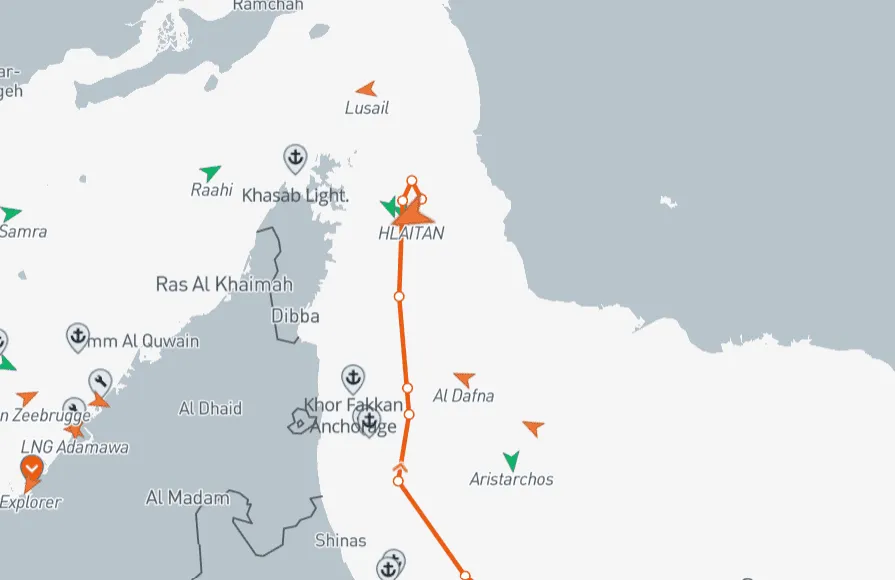

Loadings from Middle Eastern LNG plants continue to transit the Strait of Hormuz without disruption. However, Kpler is monitoring a ballast vessel – the QatarEnergy-controlled Hlaitan - bound for Ras Laffan that has entered a holding pattern ahead of passing through the Strait of Hormuz on 16 June.

Hlaitan LNG vessel track

Source: Kpler

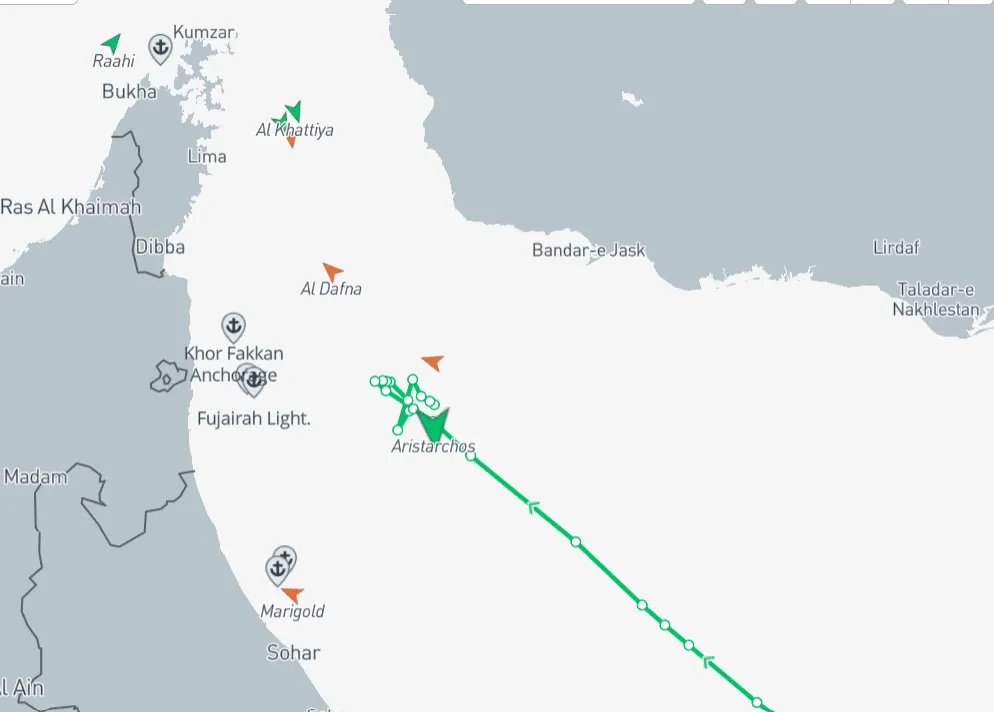

Increased caution is also being observed by non-Middle Eastern vessels attempting to enter the region. The Aristarchos LNG vessel, operated by U.S. exporter Cheniere and carrying cargo from the Sabine Pass terminal to Kuwait, has come to a standstill. The vessel halted off the coast of Fujairah on 14 June and has remained anchored offshore since then.

Aristarchos LNG vessel track

Source: Kpler

In the coming days, the Gui Ying LNG vessel, operated by Gunvor, is also set to enter the area, carrying a Nigerian loading to Bahrain.

As the Middle East enters peak cooling season, any disruption of LNG deliveries to regional importers – Kuwait, Bahrain and UAE – could strain domestic gas for power generation, triggering a switch to oil-based power generation or even energy shortages. Regional LNG importers may seek to rely more heavily on LNG supply from exporters closer to home – such as Qatar – leading to a reorientation of LNG trade flows.

In conclusion, while Qatari and UAE LNG exports remain uninterrupted following the 14 June attack on the South Pars gas field, the broader regional risk landscape has shifted. The stalling of vessels near the Strait of Hormuz highlights growing maritime caution amid heightened geopolitical tensions. With the Middle East entering its peak cooling season, a perceived threat to LNG import routes could prompt a near-term reorientation of LNG trade flows, with Gulf importers increasing reliance on Qatari volumes due to geographic proximity and supply resilience.

Though current fundamentals remain stable, any sustained escalation—especially one affecting Hormuz transit or South Pars feedgas—poses significant upside risk to global gas prices and trade patterns.

Want market insights you can actually trust?

Our analysts are updating Insight in near real-time, delivering critical intelligence on trade flows, pricing shifts, and geopolitical risk.

Updates are live across oil, LNG, and cross-commodity sectors.

Request access here.

See why the most successful traders and shipping experts use Kpler

Expert research & analysis driven by proprietary data