Stable TTF as increasing Norwegian supply balances colder temperatures; Asian LNG pressured by ample LNG inventories and weaker Thai demand

Market & Trading Calls

European TTF front-month price outlook: Stable as a significant drop in temperatures next week will be offset by additional capacity coming online in Norway as maintenance gradually winds down. The 19th EU sanctions package on Russia, expected to be published soon, poses a risk to the outlook.

Asian LNG front-month price outlook: Slightly bearish, as elevated LNG inventories, weaker Thai LNG demand, and cooler Northeast Asian weather all pressuring prices, while Pacific supply holds steady under scheduled maintenance.

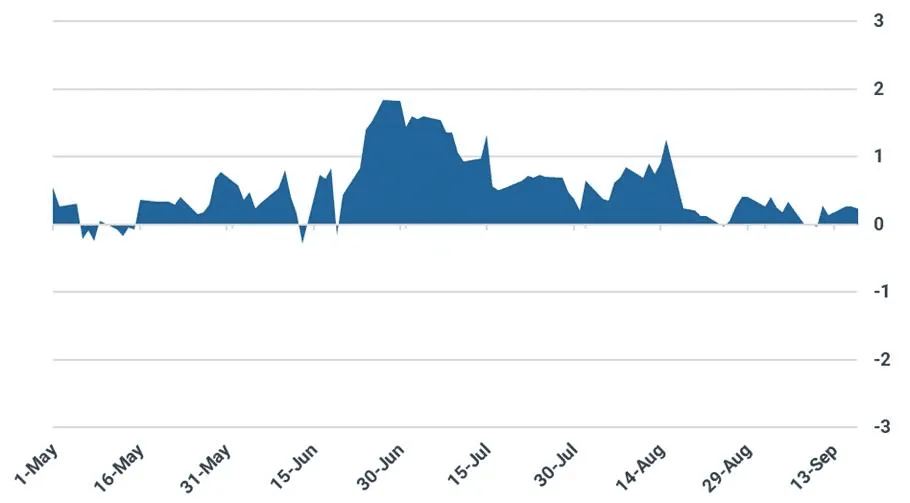

Asian LNG – TTF spread outlook: Slightly narrower as stable TTF contrasts with further downside risk in Asian LNG. The spread widened by $0.27/MMBtu to $0.24/MMBtu on 17 September.

US Henry Hub front-month price outlook: Steady as bullish momentum from revised weather forecasts showing broadly above-average temperatures for the remainder of September are counteracted by strong underground storage injections and stable production.

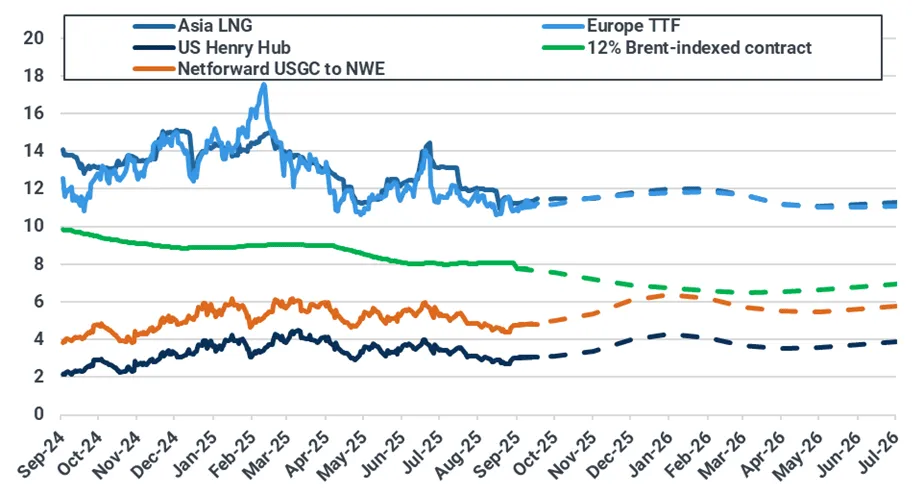

Key natural gas and LNG front-month prices ($/MMBtu)

Source: ICE, NYMEX, Spark Commodities. Brent-indexed price represents 12% slope of 90-day moving average of Brent contract. Netforward USGC to NWE calculation is 115% Henry Hub contract plus shipping and regasification costs into Gate (Spark Commodities).

Asian LNG-TTF front-month spread ($/MMBtu)

Source: ICE, Kpler Insight

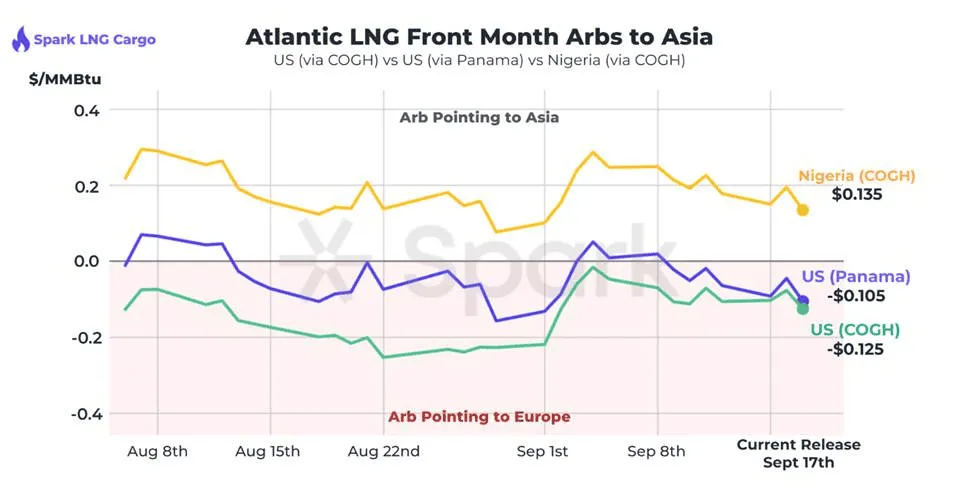

Atlantic basin LNG front-month arbs ($/MMBtu)

Source: Spark Commodities, incorporating ICE-listed Spark Freight and Spark Cargo products. For a full M+12 forward curve and netback cost breakdown, contact Spark at info@sparkcommodities.com.

Europe: Colder temperatures and additional Norwegian supply to keep TTF prices rangebound

European TTF front-month prices declined slightly to $11.24/MMBtu on 17 September, down $0.12/MMBtu from $11.36/MMBtu on 10 September. The decrease was primarily driven by weak domestic demand as temperatures rose more than previously forecasted, paired with strong wind generation in NWE. Additionally, Norwegian and Algerian maintenance continued as planned and has been so far much lighter than last year, contributing to increasing EU-27 USG levels at around 81%. Robust exports from the US despite a short-lived drop in feedgas flows into Sabine Pass last week and additional unloadings of Arctic LNG 2 cargo at the Beihai port, helped to keep a lid on prices. However, recent downward revisions to temperature forecasts into next week provided some price support in the last couple of days.

For the week ahead, Kpler Insight maintains a stable outlook for the TTF front-month contract as a significant drop in temperatures next week will be offset by additional capacity coming online in Norway as maintenance gradually winds down. The 19th EU sanctions package on Russia, expected to be published soon, poses a risk to the outlook.

On the supplyside, EU pipeline imports slightly fell by 1.7% w/w to 2.76 bcm driven mainly by lower imports from Norway as seasonal maintenance continued.

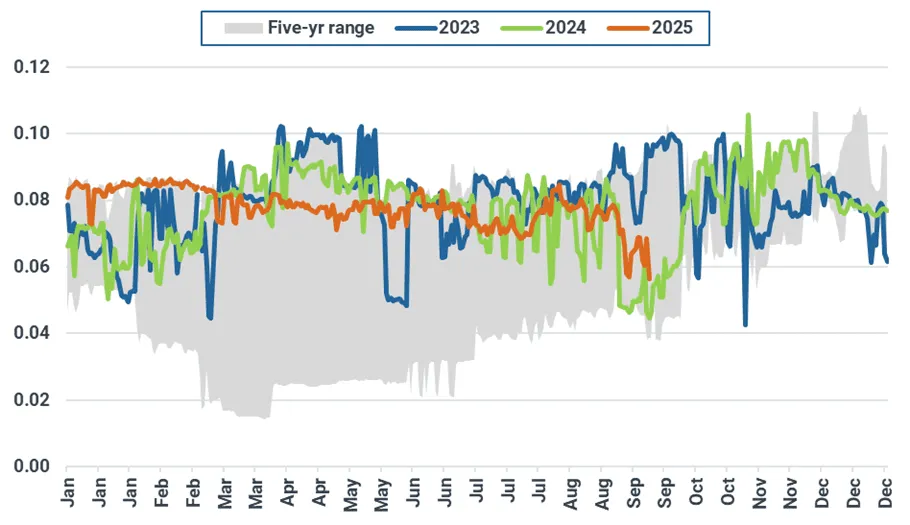

Norwegian daily net pipeline flows to the EU (bcm)

Source: ENTSOG, Kpler Insight

Similarly, Algerian exports to Spain fell on 16 September due to ongoing maintenance in the former; however, volumes are expected to recover gradually towards the end of the month.

Algeria daily net pipeline flows to the EU (bcm)

Source: ENTSOG, Kpler Insight

Looking into next week, EU-27 net pipeline imports are anticipated to increase as Norwegian maintenance starts to wind down. In addition, planned maintenance works between 22-26 September at the Mosonmagyaróvár interconnection point between Austria and Hungary could reduce exports to the latter by from Austria by around 50% and potentially impact exports to Ukraine. Lastly, light maintenance continues to take place at the VIP Pirineos point between France and Spain, slightly reducing available capacity for bidirectional flows between the countries.

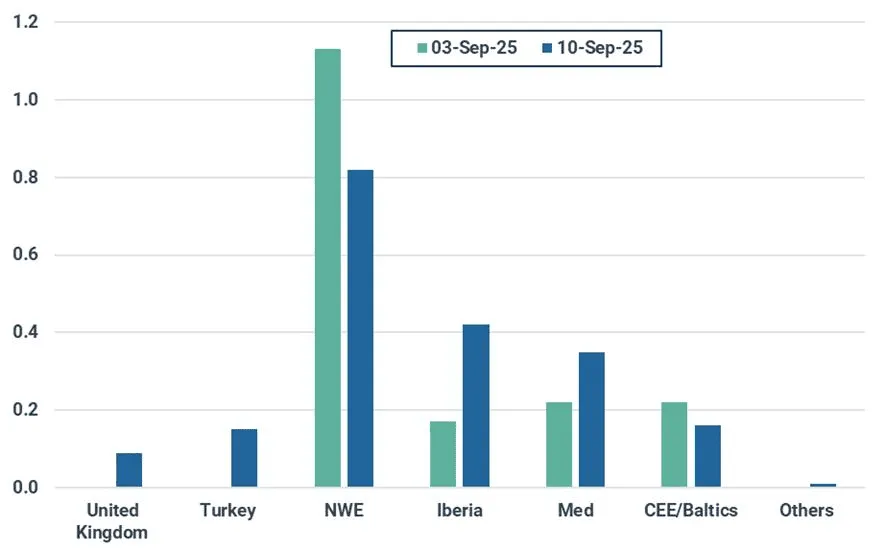

European LNG imports rose by 15% w/w to 2 mt as higher demand in Iberia and the Mediterranean region likely to compensate for the partial loss of pipeline supply into Southern Europe. Additional demand emerged from Turkey and the UK, marking the gradual seasonal increase for the two countries now that the summer season nears its end.

Looking ahead, we expect LNG volumes to increase slightly despite planned maintenance at Germany’s Brunsbüttel, France’s Montoir and Fos Tonkin, and the continuation of works at Spain’s Cartagena.

EU-27 weekly LNG imports by region (mt)

Source: Kpler Insight. Data represents week commencing 03/09 and 10/09. NWE=FR, BEL, NL, GER. Iberia=ESP, POR. Med=ITA, HVR, GRE. Baltics/CEE=FI, LT, POL. Others=SWE, MT.

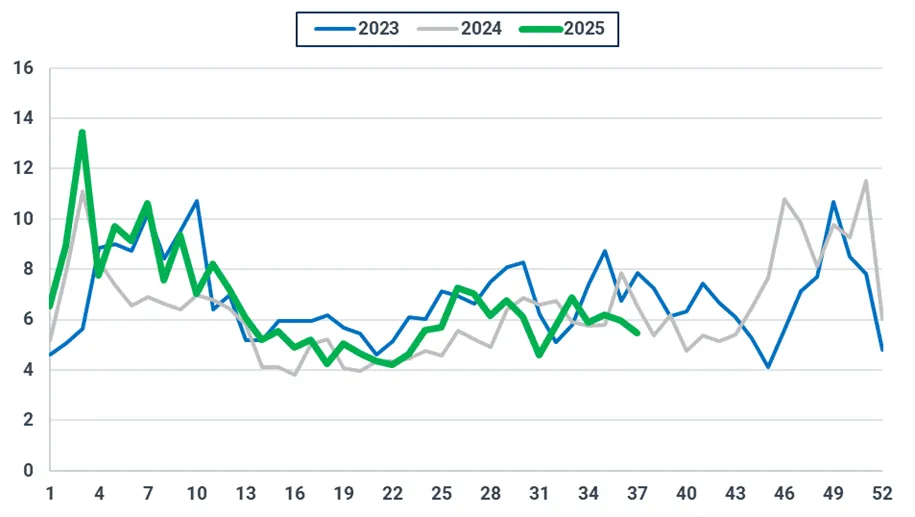

On the demand side, EU-24 gas-fired generation decreased by 8% w/w to an estimated 5.5 TWh, mainly due to strong wind generation in NWE and above-average temperatures that kept overall power demand in check. Looking ahead, with forecasts indicating a gradual reduction in temperatures and renewable generation into next week, we anticipate an increased in gas-fired generation, particularly towards the back end of the week.

EU-24 weekly gas-fired generation (TWh)

Source: Kpler Power, Kpler Insight.

Average forecast temperatures for selected European countries (°C)

Source: Kpler Power. As of 18/09 00:00 UTC.

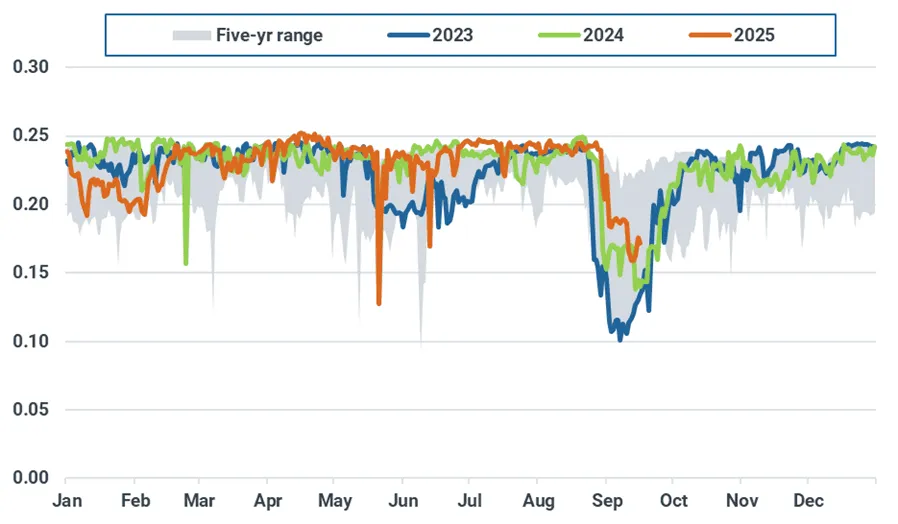

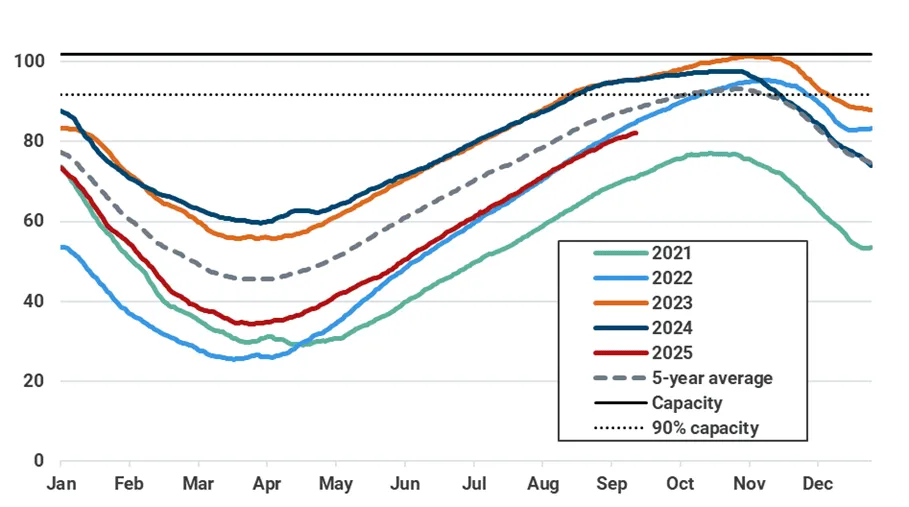

EU-27 underground gas stocks increased to 81% on 16 September, 6.5 percentage points below the five-year average. Net injections increased last week as strong wind generation and higher-than-average temperatures weakened domestic demand, making it more profitable to inject gas into UGS facilities. Looking into next week, we expect net injections to decrease as temperatures are forecast to drop along with renewable generation.

EU-27 underground natural gas inventories (bcm, left) as of 16 September

Source: GIE, Kpler Insight. Latest data as of 16/09/25.

Asia: Ample LNG Inventories, cooler Northeast Asian temperatures, and weak Thai demand to weigh on prices

Asian LNG prices climbed slightly by $0.14/MMBtu w/w to $11.48/MMBtu on 17 September, with the November contract rollover providing a modest bullish push amid otherwise subdued prompt demand in Northeast Asia.

Asian LNG prices are expected to lean slightly bearish into next week, pressured by ample inventories in South Korea and China, weaker prompt demand in Thailand, and cooler temperatures across Northeast Asia. On the supply side, Pacific volumes remain above 5-year ranges, despite planned maintenance progressing as scheduled.

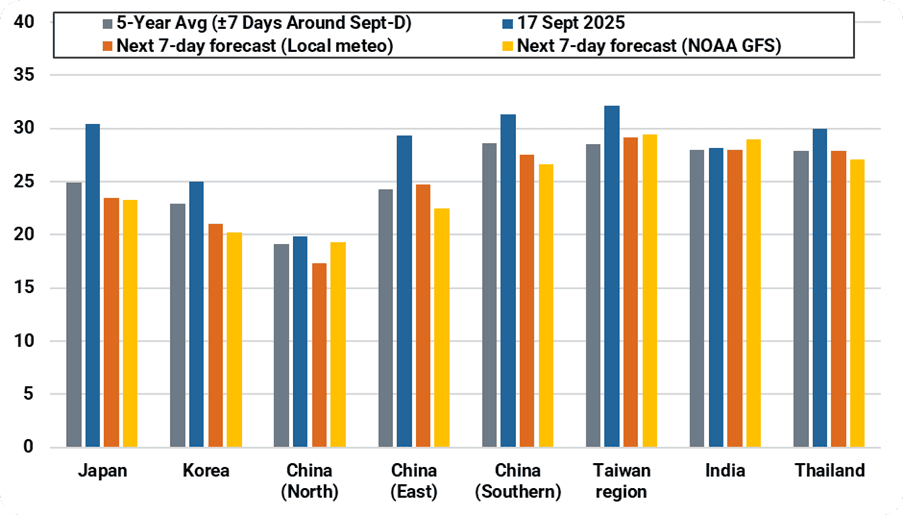

Gas-for-power demand in Northeast Asia is expected to ease into next week, with temperatures tracking at or below 5-year norms, except in Taiwan and East China where they remain slightly above average. In South and Southeast Asia, temperatures are forecast at average to slightly above average levels, supported by the gradual withdrawal of the southwest monsoon.

Forecasted average temperatures for Asian countries (°C)

Source: Meteostat, Kpler Insight. As of 17 September 2025 00:00 UTC (10 Sept data pending). Population-weighted average temperature of selected major cities across a country is shown for both historical and forecast.

Japan’s major utility LNG stocks fell for the third straight week, down 0.05 mt w/w to 1.76 mt as of 14 September, leaving inventories 0.5 mt below the five-year average amid persistent September heat. With cooler temperatures expected to ease power demand, stocks are projected to rebuild seasonally to 2.7 mt in October and 2.8 mt in November on the back of term deliveries, reducing the need for spot buying. As inventories recover and fundamentals remain weak into Q4, near-term price pressure is expected to stay skewed to the downside.

Want the complete report?

The full report is available within Insight and contains:

- Market & Trading Calls

- Europe: Colder temperatures and additional Norwegian supply to keep TTF prices rangebound

- Asia: Ample LNG Inventories, cooler Northeast Asian temperatures, and weak Thai demand to weigh on prices

- US Henry Hub: Prices to remain near $3.00/MMBtu as above-average temperatures clash with robust storage levels

- LNG Supply: Malaysia leads modest global decline; Nigeria, Indonesia rebound as Arctic LNG 2 deliveries rise.

Trade smarter. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler

Research & analysis driven by proprietary data