May 19, 2025

Tariff reprieve stokes optimism in dry bulk markets

Iron Ore & Steel: Iron ore pierces the $100/t level after China and the US slash tariffs

- Global seaborne iron ore exports finished at 30.42 Mt in the week ending 11 May, down 2% y/y. Australian iron ore shipments slipped to a four-week low of 16.94 Mt, driven by a fall in Rio Tinto loadings to a three-month low of 4.15 Mt. It remains unclear whether the dip is tied to the launch of the company’s new Pilbara Blend Fines product (60.8% Fe, compared to 61.6% previously) or related to maintenance activities.

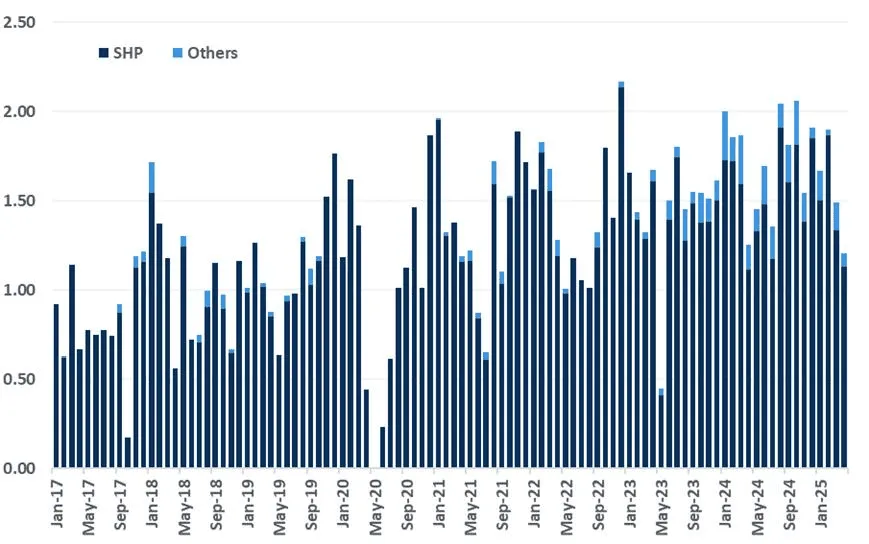

- Peruvian iron ore exports have virtually ceased following damage to the shiploader at Shougang Hierro Perú’s (SHP) port on 5 May. SHP has declared force majeure and expects the repair to take four to five months. As the dominant iron ore producer in Peru, SHP has a capacity of 20 Mtpa of iron ore concentrate in the country and produced 13.10 Mt in 2024. Given the oversupplied global market, the disruption will have limited market impact. However, the affected steelmaker, notably SHP’s parent company Shougang Group, might have to secure alternative supplies from external miners at short notice.

- On the demand front, Chinese iron ore imports totalled 25 Mt in the week ending 11 May, well above the previous five-year average of 22 Mt as firm steel output and strong steel exports continue to support consumption. Daily crude steel output by CISA member mills averaged 2.21 Mt in the first ten days of May, higher than the 2.19 Mt observed in the same period last year. With sellers frontloading shipments to avoid tariffs, April steel exports smashed expectations, reaching 10.46 Mt and the second highest since 2016. However, elevated exports are unsustainable and should fall in the coming months.

- Iron ore prices gathered momentum over the past few days as the easing of US-China trade tensions and disruption in Peru buoyed market sentiment, shrugging off the concerns over steel output curbs in China. The second-month SGX contract closed at $101.83/t on 14 May, breaching the $100/t threshold for the first time in six weeks and achieving a gain of 3.57% w/w. Meanwhile, the DCE’s most traded iron ore contract (Sept 2025) jumped by 4.61% w/w to 737 yuan/t ($102.20/t). However, we remain bearish over prices in the mid- and long-term as global supply increases. The commissioning of Guinea’s Simandou in November is set to intensify the global surplus.

Peruvian iron ore exports set to fall sharply following port accident (Mt)

Source: Kpler

Key Dry Bulk Market Developments

Source: Kpler

Dry Bulk Port Congestion

Source: Kpler

Want market insights you can actually trust?

Kpler delivers unbiased, expert-driven intelligence that helps you stay ahead of supply, demand, and market shifts.

The full Dry Bulk Weekly report is available within Insight and contains:

- Iron Ore & Steel: Iron ore pierces the $100/t level after China and the US slash tariffs

- Coal: Thermal coal volumes drop w/w, petcoke market stabilises on easing tariff tensions

- Grains & Oilseeds: Tariff bargaining boosts beans, but bearish balances burden grains

- Minor Bulks: China drives phosphate spike; Guinea tightens control on its mining sector

- Dry Bulk Freight: Capesize poised for recovery; Pacific earnings under pressure

- Key Dry Bulk Market Developments

Unbiased. Data-driven. Essential.

Trade smarter. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler

Request a demo

Expert research & analysis driven by proprietary data

Request access