The yin/yang dynamic of crude versus products

The yin/yang relationship between crude and clean products has long been exhibited in a symbiotic yet oppositional dynamic.

Market & trading calls

- Global crude benchmarks to come under pressure as strong crude exports in recent months result in material inventory builds by year-end.

- Diesel crack spreads to remain supported, particularly East of Suez amid ongoing refinery maintenance and lower exports.

One added dimension to the yin/yang relationship is currently exhibited through sharply diverging supply trends. Crude markets are riding a wave of export strength, while product markets, particularly diesel, face renewed tightness. The result is a structural imbalance that appears poised to persist.

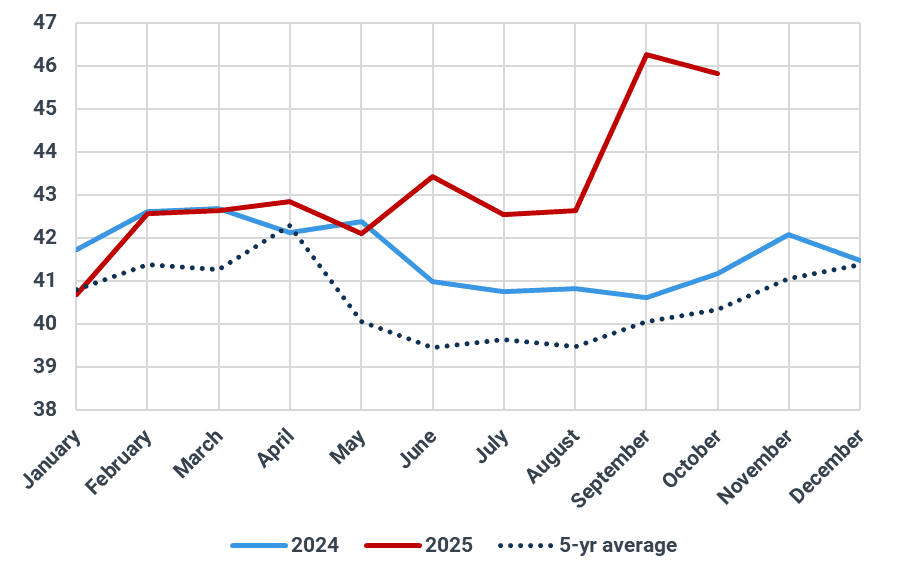

Global crude exports reached nearly 46Mbd in October, the second-highest level on Kpler’s records, trailing only September. The sharp climb reflects a confluence of surging non-OPEC flows and the partial unwinding of OPEC+ production cuts, both of which are adding significant volumes to seaborne balances. At a time when macro sentiment around demand has stabilised, the scale of this supply uptick is feeding oversupply concerns across benchmarks.

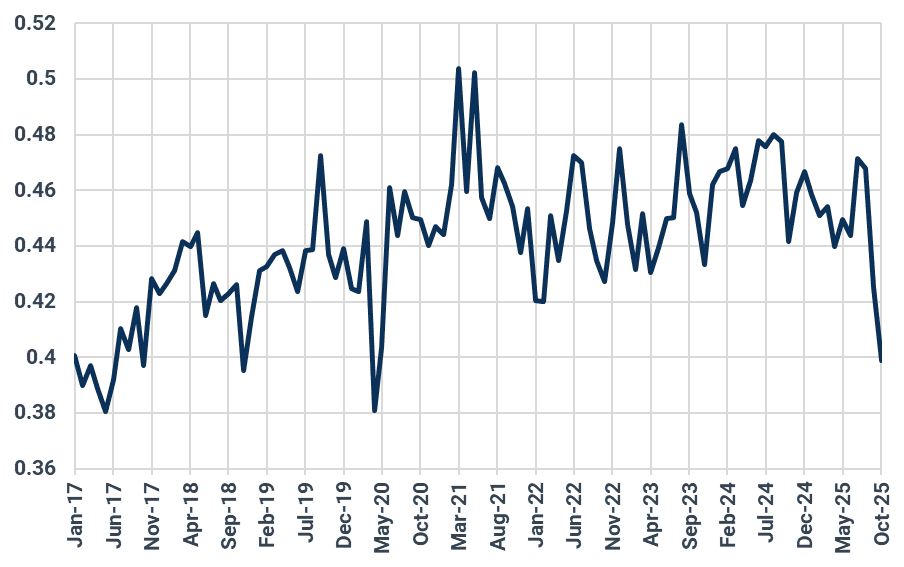

Global clean-product-to-crude export ratio

Source: Kpler

In stark contrast, global clean product exports slumped to a one-year low last month. This pushed the global clean-product-to-crude export ratio to its weakest level since April 2020, underscoring the widening gulf between upstream strength and downstream constraints. While October typically sees a dip in product exports due to refinery maintenance and seasonal demand lulls, the scale of this year’s drop is particularly sharp.

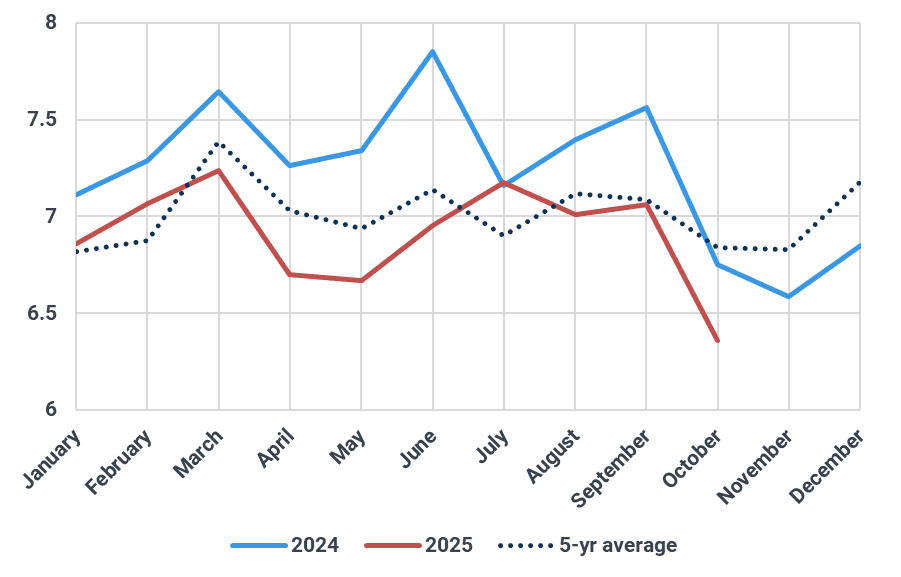

Global clean product exports, Mbd

Source: Kpler

Diesel is the core driver of this underperformance. Through the first ten months of 2025, diesel exports have averaged 430kbd lower y/y, despite refinery runs climbing by 860kbd over the same period. This disconnect highlights a key structural shift: a lighter crude diet across the refining system. Amid changing feedstock slates and operational constraints, refiners have skewed toward producing more light ends at the expense of distillates. Adding to the squeeze, distillate barrels have been increasingly directed toward restocking depleted inventories, further reducing supplies available for export. With inventories still below multi-year norms in key consuming regions, this internal demand is unlikely to abate quickly—particularly as winter sets in and heating-related diesel demand ramps up.

Global diesel exports, Mbd

Source: Kpler

Meanwhile, the outlook for crude supply remains biased to the upside. Ongoing non-OPEC growth, led by Brazil, Guyana and Canada, continues to add barrels. The gradual reversal of OPEC+ cuts has been providing further tailwinds and will do so into year-end, reinforcing a fundamental surplus in crude markets.

Given the expectation of ongoing strength in crude supply, as well as increased demand for diesel due to a cold start to winter, the yin-yang dynamic between crude abundance and product tightness looks set to persist.

Global crude exports, Mbd

Source: Kpler

Want market insights you can actually trust?

Kpler delivers unbiased, expert-driven intelligence that helps you stay ahead of supply, demand, and market shifts. Our precise forecasting empowers smarter trading and risk management decisions.

Unbiased. Data-driven. Essential. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler

Expert research & analysis driven by proprietary data

.jpg)