EFS Squeezes west-to-east crude arb as Trump tariffs add new uncertainty

A widening of the Brent-Dubai Exchange of Futures for Swaps (EFS) has choked off the once-lucrative arbitrage for light sweet crude flowing from West to East, exacerbating the supply picture in the Atlantic Basin.

Key takeaways:

- A wider Brent-Dubai EFS is severely curtailing West-to-East light sweet crude flows, leading to a supply build up in the Atlantic Basin.

- The closed arbitrage is evident in trade data: West African light sweet exports dropped to an 11-month low of around 500 kbd in June, while CPC Blend flows to the East have collapsed since May.

- Significant new uncertainty has been injected into the market after US President Trump on Wednesday announced tariff demands of 50% on Brazil and 30% on Libya, Iraq, and Algeria, with oil supplies potentially affected.

This fundamental market shift, largely driven by OPEC+ strategy, is now being complicated by a new layer of geopolitical risk following fresh US tariff threats, creating a highly uncertain outlook for global crude flows.

West African and Libyan light sweet grades along with CPC Blend have seen a pronounced drop off, as inter-regional spreads and freight rates disincentivise flows.

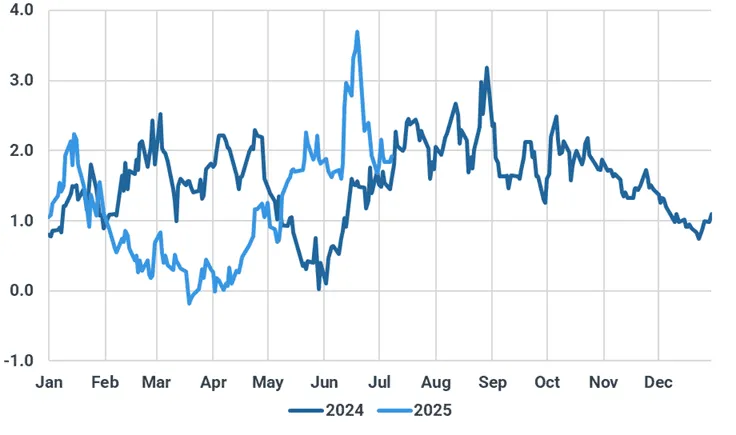

The Brent-Dubai EFS — the premium of Ice Brent futures over Dubai swaps — averaged around $1.50/bbl in May, up over $0.40/bbl in April. The spread has appreciated around $2/bbl since Mid-March, when it was near parity, according to Argus Media. A wider EFS makes Dated-linked grades less attractive to Asia-Pacific buyers, who otherwise buy crude priced against the Dubai benchmark.

Brent-Dubai front-month EFS, $/bbl

Source: Argus Media

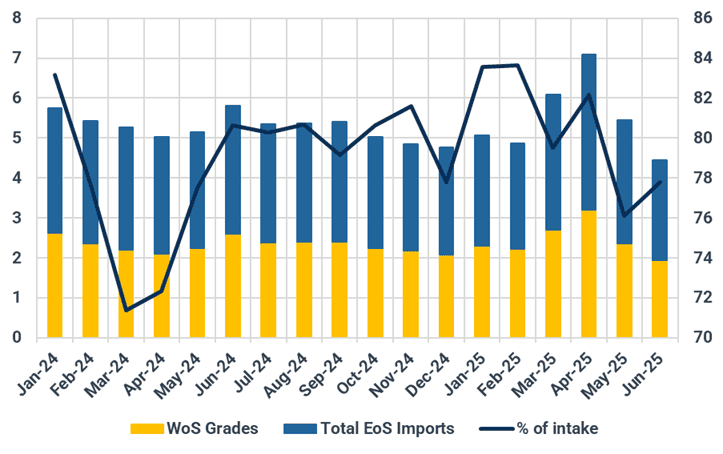

The impact on trade flows has been pronounced. West African light sweet exports fell from 944 kbd in April to an 11-month low of around 500 kbd in June. Similarly, East of Suez flows of CPC Blend have collapsed from a 342 kbd average (Feb-Apr) to just 12 kbd since May. The absence of CPC competition may have partly played in Aramco’s stronger boost for its light barrels into the Asian market.

Unfavourable freight dynamics, with VLCC rates from the Mideast Gulf to China trending lower than those from the Atlantic, have further disincentivised long-haul movements.

Proportional West of Suez origin light sweet crude to East of Suez, Mbbls (LHS), WoS % of total intake (RHS)

Source: Kpler

This pattern appears to be a direct consequence of OPEC+ strategy. By accelerating the return of barrels to the market, the group has successfully weighed on the Dubai complex relative to Brent. Speaking today, UAE energy minister Suhail al-Mazrouei affirmed the market needs the additional supply, citing the absence of stockbuilds. This supports murmurs from the OPEC seminar in Vienna suggesting the group will favour another accelerated supply increase of 548 kbd for August before pausing.

While the market was grappling with these fundamental shifts, Washington introduced a significant wildcard. On Wednesday, President Trump unveiled a new round of tariff demand letters, including a steep 50% rate on Brazil and a 30% rate on Algeria, Libya, and Iraq. While it remains to be seen if crude oil will be exempt, the threat alone could alter trade flows. The US imported an average of 270 kbd of Brazilian crude last quarter, primarily medium sweet Tupi into PADD 5. A similar combined volume of Libyan and Iraqi crude also arrives in the US monthly. Should these flows, totaling over 500 kbd, be disrupted, alternative grades from Guyana or Argentina could be called upon to fill the gap. For now, the uncertainty over these potential levies will be a key factor for charterers and traders pricing crude from the affected nations.

Want market insights you can actually trust?

Kpler delivers unbiased, expert-driven intelligence that helps you stay ahead of supply, demand, and market shifts. Our precise forecasting empowers smarter trading and risk management decisions - backed by the most accurate oil price predictions two years running.

Unbiased. Data-driven. Essential. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler

Expert research & analysis driven by proprietary data

Related posts