India back in Russian oil market, shrugs off US pressure, squeezes Dubai

India’s return to the Western Russian crude market effectively shuts the door on China’s short-lived opportunistic buying. Should this “business as usual” trend hold, Middle Eastern producers will be under mounting pressure to cut OSPs next month to secure a foothold in Chinese demand.

Key takeaways

- India’s state-owned refiners have resumed September–October Urals purchases, with prices now aligning with their buying expectations.

- Chinese refiners are effectively sidelined in the Urals market and are now fully concentrating on ESPO liftings.

- Middle Eastern producers may be forced to trim OSPs next month to stay competitive for Chinese demand, should India continue to prioritize Russian barrels.

India’s state-owned refiners are back in the Urals market, snapping up September- and October-loading cargoes, according to media reports. In fact, they never stepped away — even as U.S. President Donald Trump threatened higher import tariffs over India’s role in the Russian oil trade. Market participants told Kpler that Indian refiners had been leveraging geopolitical tensions to pressure Russian sellers into lowering prices, and now, with prices aligned to their expectations, buying activity has picked up again. Urals is currently trading at roughly -$3/bbl against Dated Brent on a delivered basis in India, widening from the $1.5–$2/bbl discount seen in late July, they said.

The return of Indian refiners suggests their Chinese counterparts have once again been edged out of the market after a brief opening in the purchasing window. State-owned and mega-sized private refiners are believed to have secured around 13 cargoes of Western Russian crude for October arrival and two cargoes for November as of Aug. 15. Since then, however, no new trades have surfaced, likely because Indian demand has absorbed the bulk of available barrels, leaving little room for other buyers.

That said, India’s imports of Russian crude are still expected to ease in September, as refiners have secured additional spot cargoes from the Middle East and the U.S. as a contingency against potential Russian supply disruptions. At the same time, Indian refiners remain notably absent from the September ESPO market, where they typically lift at least three cargoes per month. With President Trump showing no intention, for now, of penalizing China over its Russian oil purchases, Chinese refiners are actively securing available ESPO cargoes in the market.

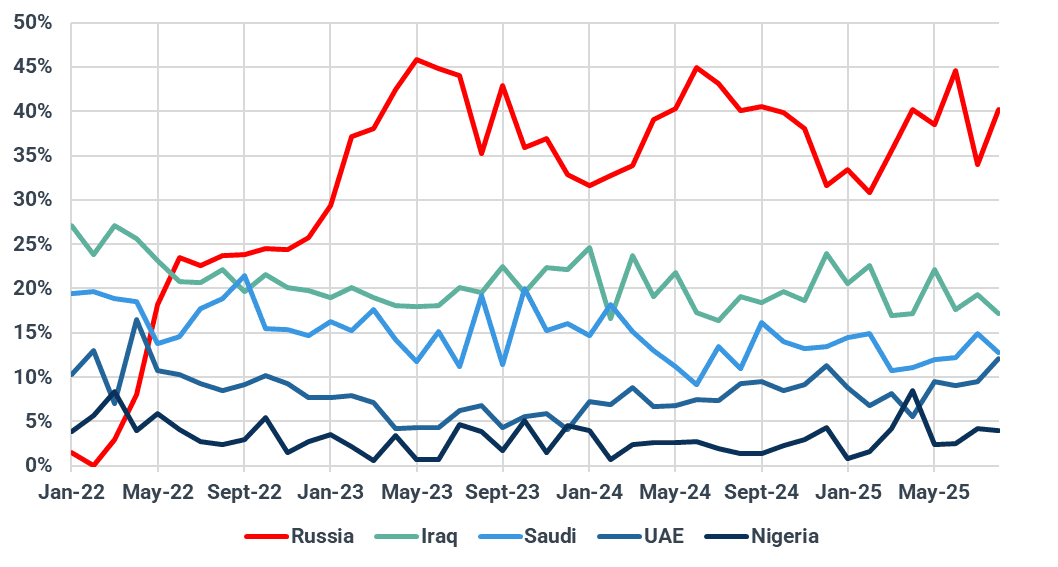

Share of key suppliers in India’s total crude imports, %

Source: Kpler. August Figures Predictive as of Aug 21

As Indian refiners and New Delhi reaffirm their commitment to maintaining Russian energy trade — brushing off Washington’s tariff threats — Russian oil flows continue largely as usual. If there are no major shifts in the geopolitical or sanctions landscape over the next two to three weeks, India is expected to keep prioritizing Russian crude over Middle Eastern barrels, driven by more attractive pricing. This sustained preference would intensify pressure on Middle Eastern producers, forcing them to contend with a growing supply overhang, weakening domestic demand, and elevated output levels stemming from their adjusted quotas. Saudi Aramco raised its September OSPs to the upper end of market expectations, buoyed in part by India’s demand to replace Russian barrels. However, if that support fades, Aramco and its fellow NOCs may be forced to cut their October OSPs to better align with the softening Dubai structure. The Dubai M1–M3 spread has averaged around $2.4/bbl so far in August, narrowing from nearly $3/bbl in July, according to Argus Media data.

One bullish factor Saudi Arabia and other Middle Eastern NOCs may be counting on is China’s ongoing SPR replenishment, which is likely to keep Chinese SOEs in the market for additional barrels over the next two to three months. However, with the Brent–Dubai EFS narrowing, booming production in the Atlantic Basin, and rising supply within the Middle East itself, regional producers are set to face mounting competition for Chinese demand. This could trigger a round of price adjustments — if not an outright “price war” — with the first signal likely to be a meaningful cut in October OSPs.

Want market insights you can actually trust?

Kpler delivers unbiased, expert-driven intelligence that helps you stay ahead of supply, demand, and market shifts.

Trade smarter. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler

Get research & analysis driven by proprietary data