How Russia is dealing with sanctions in 2024

What are the effects of sanctions against Russia? What impact do the sanctions have on Russia's economy? The following is an extract from Kpler’s latest whitepaper 'Russia in 2024: Learning to live with sanctions'. Read below to find out more.

The introduction of the price cap has been a key trigger in rerouting Russian crude oil flows towards Asia. European countries have stopped buying Russian barrels one after another in anticipation of the December 5 deadline – Lithuania bought its last cargo of Urals in March, Finland in July, Romania in October, whilst Italy, South Korea and the Netherlands stopped in late November – paving the way for higher flows to Asia. As such, India’s ascent as a buyer of Urals par excellence has been gradual, starting off from a low point of just one single cargo back in January 2022 to 59 by December 2022.

Thanks to a higher production base overall (see Production above) and lesser pipeline volumes delivered to Europe, Russia’s seaborne flows rose by 4% y/y and averaged 3.504 Mbd in 2023. This marks the second highest annual pace of exports after the 2019 all-time high of 3.532 Mbd (which was in its turn mostly driven by the chloride contamination story that effectively halted deliveries via the Druzhba into Central Eastern Europe for several months).

In 2023, India consolidated its standing as the largest buyer of Russian seaborne crude. Whilst in 2022 the annual average it imported from Russia stood at 685 kbd, a twelvefold increase compared to the 2021 tally of a mere 50 kbd, last year the same metric soared to 1.751 Mbd. In total, Indian buyers bought eight different grades of Russian crude, with the list spearheaded by Urals (1.222 Mbd), followed by Sakhalin’s Sokol (139 kbd), Russian CPC from Lukoil’s Caspian assets (98 kbd) and ESPO (89 kbd).

Buying of Russian crude was by no means the exclusive behaviour of a selected few; all of India’s commercial-scale refiners with access to coastal ports were buying across 12 installations. That said,IOC accounted for 27% of all purchases at 467 kbd, overtaking Reliance as the largest Indian buyer sinceApril 2023 (India’s largest private refiner bought 406 kbd last year). As trading moved into 2024, the prevalence of IOC might be in doubt as other refiners such as BPCL have been ramping up their purchases.

With an ascent into Russian purchases as steep as India’s, there remain many headwinds to maintain such fast-paced imports. First, Russian sellers and Indian buyers are still yet to iron out their differences on the future currency of such oil flows – the Russian rouble is largely unusable for India’s refiners and vice versa for the Indian rupee, whilst the Chinese yuan is a far cry from being politically palatable in Delhi. Second, sanctions from G7 have so far not been a game changer but they’ve recurrently put a spoke in Moscow’s wheel by needing to revamp shadow shipping companies’ insurance coverage or change the particulars of financing. Third, the pricing environment for Indian buyers in early 2024 differs greatly to the one seen a year ago when delivered Urals to India was trading at a -$12 to -$10/bbl discount to Brent. Higher differentials weaken the appeal of Russian crude, and the discrepancies between Rosneft and IOC over a potential extension of a supply deal that would send Sokol cargoes to India in 2024, too, attests to those pressures being real. That said, we consider it unlikely that India would fall below the 1.5 Mbd pace of Russian purchases over the course of 2024.

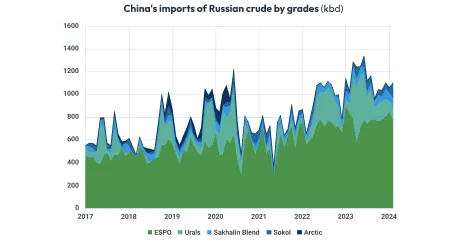

India has become the largest buyer of seaborne Russian crude, but China remains the largest buyer per se. This is thanks to two pipeline routes delivering Russian barrels to China, the ESPO-1 conduit that bifurcates in Skovorodino and ends in Heilongjiang’s Mohe and the Kazakh transit via the Atasu-Alashankou pipeline. Onland deliveries of crude have been relatively stable in 2023 at 815 kbd, marginally up compared to 811 kbd in 2022. Whilst there has been no sizable change in pipeline flows, seaborne supplies have increased a whopping 35% y/y in 2023, tallying 1.3 Mbd. China’s appetite for Russian crude has been as multi-pronged as India’s. Most notably, Russia’s Far Eastern medium sweet flagship grade ESPO has become intrinsically connected to the Chinese market, becoming even more a staple of Shandong refiners.

Thanks to additional volumes of Eastern Siberian barrels being delivered to Kozmino via rail, ESPO volumes soared to a record high of 862 kbd last year, an increase of 70 kbd compared to 2022. Of this, China bought 90% on an annual average, however even this figure hides the ratcheting up of Chinese interest in H2 2023 and beyond. After Russian sellers of ESPO flirted with the idea of diversifying away from China and have been supplying 200-230 kbd of the grade to India in H1 2023, the dominance of Chinese buying emerged in full swing in the first months of 2024 when Indian refiners were effectively squeezed out of the market. In January 2024, there was just one laden tanker sailing towards India, 97% of all exports going to Chinese buyers.

China’s imports of Urals did not increase as steeply as India’s, the 178 kbd imported in 2022 compares to the 254 kbd taken in last year. Apart from a relatively unchanged pull from China’s state-owned refiners, the uptick is also coming from private refining majors tapping into the Russian market – neither Hengli nor Shenghong were buying Russian barrels in 2022, but the two combined rose to almost 100 kbd in 2023.

Chinese refiners also started to buy more Arctic barrels and the opening up of the Northern Sea Route has been a great boon in sending more of these volumes across in the summer navigation period. Easily surpassing the heretofore record one cargo per year from 2022, last year saw 14 deliveries from Russia to China sailing through the Northern Sea route, starting in July and ending in early October. With increased navigation activity across the NSR, this number is guaranteed to rise higher over the upcoming years, especially in an environment when the Suez Canal and the Red Sea become the shipping industry’s Gordian knot.

The data, analytics and research behind this report was all sourced from Kpler's intelligence platform.

Enabling you to pinpoint opportunities and minimise risk across commodity markets, these powerful tools are critical for global commodity professionals. To learn more, contact us today.

Did you know?

The data, analytics and research behind this report was all sourced from Kpler's intelligence platform.

Enabling you to pinpoint opportunities and minimise risk across commodity markets, these powerful tools are critical for global commodity professionals. To learn more, contact us today.

See these in action. Get your demo of the service now.

See why the most successful traders and shipping experts use Kpler