Soybean crush margins in South America squashed by record exports

Current US-China trade policy prices US soybean exports to China out of competition, leading to record South American imports. Resulting market distortion has lifted the lid on the price of South American soybeans as they no longer need to price as competitively on the world stage for demand. This has tightened soybean crush margins in South America and China. The weaker crush margin will temper the rise of Brazilian soybean values and therefore see US soybean prices remain low in efforts to retain export demand. The slowdown in soybean oil and meal production in South America may also offer fundamental support to the crush margin.

- Chinese import tariffs on US soybeans have lifted the lid on South American soybean values, therefore challenging crush margin profitability.

- Soybean crush demand in Brazil and Argentina slows following tighter crush margins.

- Chinese demand for South American soybeans has been unprecedented with no imports of US soybeans on the books, but domestic crush margins have become tighter.

- As Chinese crush margins narrow, the price of Brazilian soybeans may weaken to support export demand. Therefore, US soybean values will need to remain competitive to uphold export demand.

- Dec-25 CBOT soybean board crush may widen under a tighter soybean by-product supply and US soybean price competitiveness.

South American soybeans prefer to sail then split

For Brazil, exports and crush are the two key factors of soybean usage and both compete for supply. At times when price is high, crush demand can slow first due to a weak margin if the sum return of soybean meal and oil is not higher than the input cost of the soybean.

After Brazil harvested a record soybean crop earlier this year, the next step has been finding demand to leave stocks near exhaustion come the end of the marketing year; with the market anticipating a larger soybean crop in 2026. This goal has been greatly assisted following the development of higher import tariffs between the US and China.

At a spot FOB basis, US soybeans have been pricing less than Brazil since mid-June. Recently, for Sep-Oct shipment, US soybeans were reported to be 80-90 ¢/bu cheaper than Brazilian origin but Chinese tariffs add $2/bu to US soybeans making them uncompetitive. This distortion in the market has supported Brazilian soybean exports to China, despite their rise in value, with the US having to find demand elsewhere.

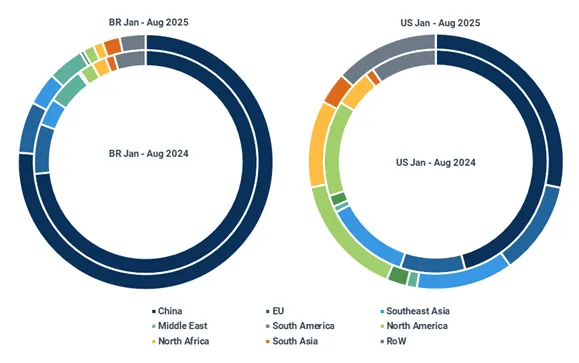

Brazil acquires a greater share of Chinese demand, US sweeps up demand elsewhere (% exports)

Source: Kpler Insight

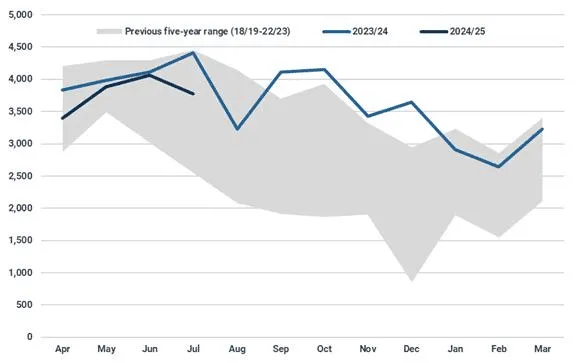

As Brazil’s export pace has remained strong despite the higher price, this has seen domestic crush demand fall back, contrary to the usual positive correlation between production and crush. In recent years, Brazil’s soybean crush demand has accounted for approximately one-third of total usage and has increased nearly every year for the past 15 years. However, since the beginning of the 2024/25 marketing year, Brazil’s soybean crush has underperformed relative to last year due to a weakening crush margin.

Brazilian crush demand underperforms despite larger crop (Kt)

Source: ABIOVE

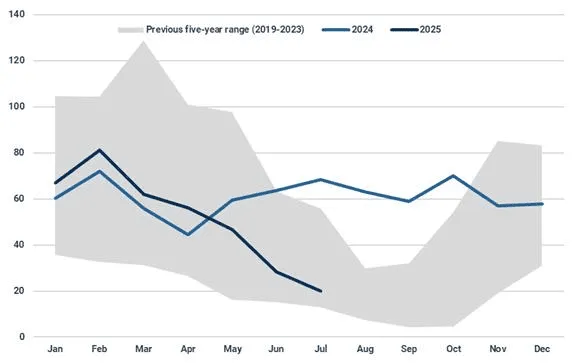

In July 2025, an indicative soybean crush margin for the port of Paranaguá was $20.06/t, the lowest since September 2023.

Brazilian soybean crush margin falls to marketing year low in July (FOB Paranaguá, $/t)

Source: ABIOVE, Kpler Insight

The tightness in the margin comes as a result of the higher price of soybeans and the significantly weaker soybean meal price. Despite the relative strength in soybean oil, its smaller proportion of overall crush output limits its influence on the profitability of the margin.

Brazilian soybean crush weighed by relatively firm soybean and weak soymeal values (FOB Paranaguá, $/t)

Source: ABIOVE

Argentina, the world’s largest soybean oil and meal exporter, is also seeing crush volumes fall lower than last year despite producing a similar-sized soybean crop y/y.

Argentine soybean crush also falls below the pace of last year (Kt)

Source: Buenos Aires Grain Exchange

As seen with Brazil, both the higher value of soybeans and lower value of soybean meal have led to a tighter crush margin in Argentina. It has been reported that the FOB crush margin had reached break-even in August due to the challenging and varied fundamental demand across the soybean complex.

From March to August, Argentine soybean exports to China neared 5 Mt, the largest for that time period since 2020. The vessel line up for September suggests this strength will continue, currently above 1.5 Mt, of which more than half is in transit.

Cumulative Argentine exports to China rise to highest since 2020 (Mt)

Source: Kpler Insight

High tariffs price out the US, causing robust Chinese imports of South American origin

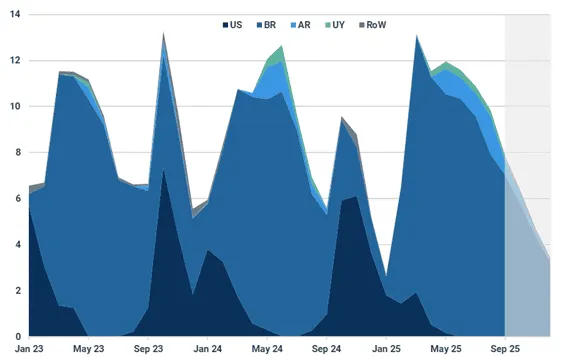

China’s appetite for South American soybeans has been extremely firm, bucking the seasonal trend where China pivots towards the US at this time of year, leading to less South American imports. From January to August, soybean exports from Brazil, Argentina, and Uruguay to China sum to 72 Mt; the greatest on record for the period and surpassing the previous record set last year by 8%. Although total volume is sliding lower y/y, vessel line ups for September suggest this record pace will continue, with approximately 8 Mt of soybeans to be shipped to China from these three origins.

South American exports to China remain elevated as US pushed to sideline (Mt)

Source: Kpler Insight

After the US and China extended their pre-existing trade agreement in August by 90 days this pushed the expiration date to 10 November 2025. In recent years, US soybean exports to China have peaked in either October or November, with either month usually accounting for approximately 25% of total US exports to China.

Therefore, the expiration date of the trade agreement poses a significant threat to US soybean sales as China will return to South America at the turn of the new year. So, the current trade policy between the US and China remains a key watch point as any developments regarding this situation will greatly influence the CBOT soybean market.

Fundamentally, soybean supply in South America is ample enough that China will not need to import soybeans from the US before the 2026 Brazilian crop comes online. However, depending on the extent, if China lowers its import tariff on US soybeans this could bring some demand to the US.

CBOT soybean board crush should widen

So, as the lid has been lifted for South American soybean values following the absence of US competitiveness, this has been challenging the profitability of crush margins in South America. Chinese crush facilities are also feeling the pinch, with all regions reportedly seeing extremely tight, in some cases negative, crush margins. Although, China’s National Grain and Oil Information Center reported that domestic crush facilities will uphold the already high crushing pace during September.

The relative weakness in South American soybean crush margins has been curtailing crush demand on the continent. Therefore, this will be reducing the production of soybean meal and oil. In addition, as Chinese margins fall below break-even, Brazilian soybean values are unlikely to rise higher. So, US soybean values will struggle to appreciate due to risk of losing export demand. With less soybean meal and oil available and a ceiling being found for soybeans, it is likely to see the CBOT soybean board crush for Dec-2025 widen in the short-term.

The direction of the CBOT soybean board crush for the Mar-26 and May-26 contracts will be significantly influenced by the size of the 2026 Brazilian soybean crop. On paper, Brazil is expected to produce a larger crop than last year due to larger acreage. However, as sowing has just begun, acreage and yield hang in the balance. The market will be paying close attention to how accommodating weather will be as this crop develops in the coming months.

See why the most successful traders and shipping experts use Kpler

Gain clarity on dry bulk flows, rates & fundamentals to navigate market shifts precisely