Copper: emerging US shortage to widen Comex-LME spread by October

Strong import volumes have so far prevented a near-term shortage, but rising demand and limited domestic capacity point to a widening Comex-LME spread by early Q4.

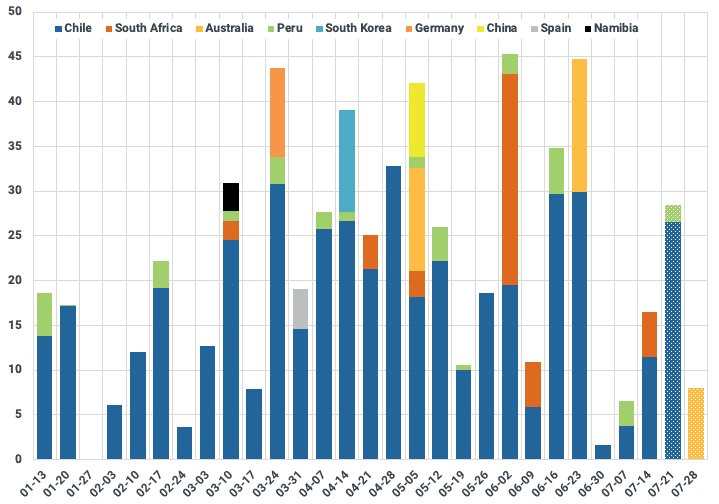

The announcement of a 50% tariff on imported refined copper into the US has triggered a widening of the Comex-LME spread from 11% to 27%. While this widening should not be surprising, the more interesting point is that the premium has remained well below the eventual tariff rate of 50%. Although this may reflect market expectations of a lower final tariff level, it is more likely explained by the absence of an imminent refined copper shortage in the US. After all, so far this year (through July 17), the US has imported 577 kt of refined copper in bulk—equivalent to 96% of the full-year 2024 total of 598 kt. Including volumes already en route to the US and expected to discharge before the August 1 deadline, total imports could reach an unprecedented 624 kt.

To achieve such record inflows, the US’s primary supplier, Chile, increased its shipments, while the US simultaneously expanded its supplier base. Between 2019 and 2024, Chile and Peru accounted for a combined 98% of US refined copper imports. In 2025 year-to-date, this share has declined to 80%, as South Africa (7 cargoes), Australia (3 cargoes), China, South Korea, and Germany (1 cargo each) have complemented the traditional South American volumes.

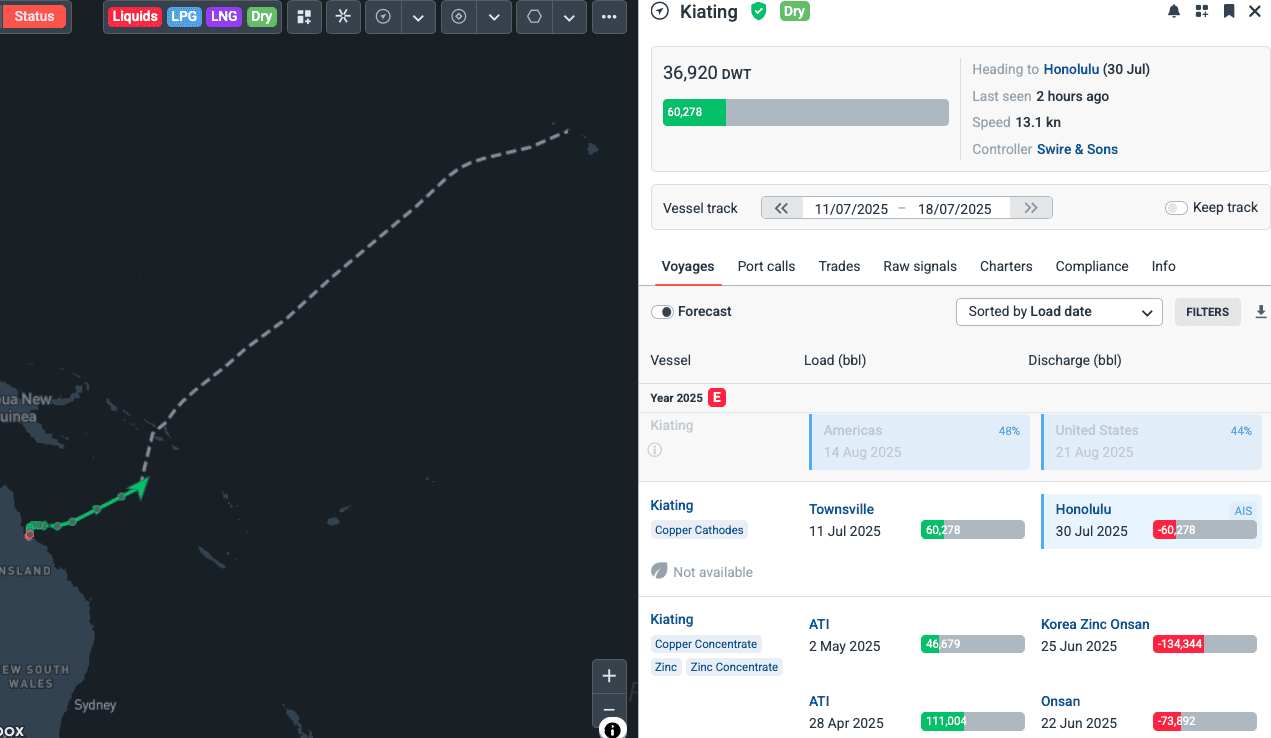

The most recent Australian cargo highlights how creative traders have become in capitalizing on current market dynamics. Kpler data shows that on July 16, the bulk carrier Kiating loaded refined copper in Townsville, Australia. To discharge on US soil ahead of the tariff deadline, the vessel’s AIS is currently pinging Honolulu—a destination that has not previously received such a cargo—rather than the primary US Gulf Coast copper hubs: New Orleans, Houston, and Panama City (FL). The most recent signal indicates an arrival date of July 30, making it a race against time. A subsequent intra-country transshipment from Hawaii to the Gulf Coast via the Panama Canal is likely.

If the US wants to attract sufficient volumes of refined copper once domestic inventories are drawn down, the Comex-LME spread will need to widen further. As a reminder, the US is a net importer of refined copper but a net exporter of copper concentrate, due to limited domestic smelting capacity. Even with potential fast-tracking of mining projects such as Santa Cruz in Arizona or Twin Metals in Minnesota, the US remains far from replacing refined copper imports with domestic output (see Under which circumstances could the US become self-sufficient in copper?). Based on our year-to-date import data and rising US copper demand—particularly from critical infrastructure investment—the Comex premium will likely need to increase significantly by early Q4, with traders expected to front-run the emerging supply gap. At current LME prices, a 50% premium would imply a Comex price of $6.58/lb, compared to $5.50/lb as of July 17. Assuming LME prices remain stable, we expect Comex to trade above $6.00/lb by October 2025.

Refined copper: Weekly US imports by origin in 2025 + prediction (kt)

Source: Kpler

Want market insights you can actually trust?

Kpler delivers unbiased, expert-driven intelligence that helps you stay ahead of supply, demand, and market shifts.

Trade smarter. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler

Expert research & analysis driven by proprietary data