EU’s 18th sanctions package to tighten Russian tanker supply

For the tanker market there were three key elements to the EU’s 18th sanctions package announced last week. The crude price cap will be lowered and then shift to a floating mechanism; a new ban on EU imports of refined products made from Russian crude, even made in third countries and new vessel sanctions will be introduced after the grace period is over in early 2026.

Market & Trading Calls

- A floating crude price cap will restrict discretionary EU vessels from Russian trade.

- Discretionary tonnage only trades Russian cargoes when the crude price is under the cap.

- Ban on EU imports of refined products made from Russian crude could boost clean tanker demand as Suezmax usage from India is cut

- Limited impact on utilization of additional vessels sanctioned by the EU

The key transition and implementation dates are listed here but for the tanker market the first date to be aware of is the implementation of the $47.60/bbl price cap. The 45-day transitional period begins on 3 September, with the switch to the new cap finalised on 18 October.

Lowered and then floating price cap

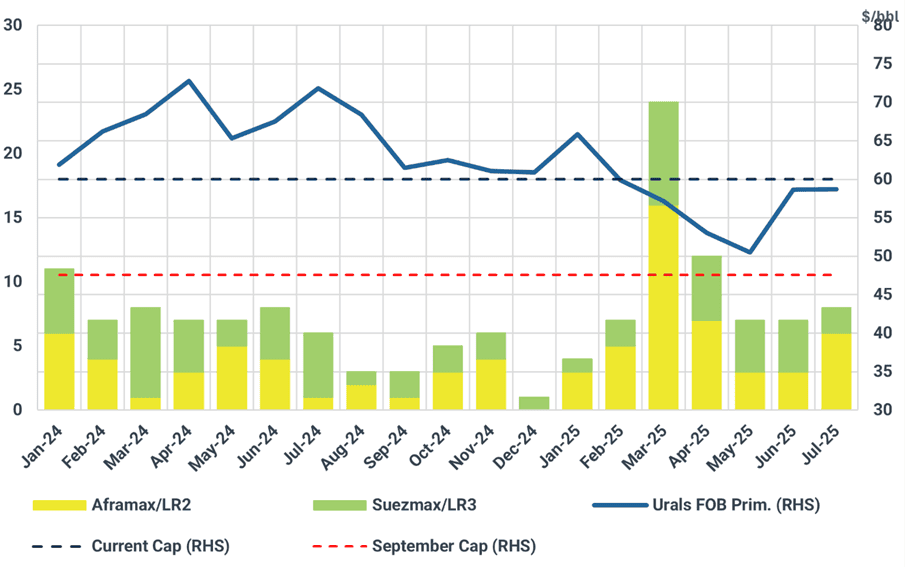

In March, Urals dropped below the $60/bbl price cap level. In the period since then, more than 20 Greek-owned Aframaxes and Suezmaxes have started trading Russian crude per month. By lowering the price cap, this is what the EU wants to restrict.

Vessels entering the Russian Crude trade following a 12-month break (LHS) and Urals fob Novorossiysk ($/bbl)

Source: Kpler, Argus Media

The first step will reduce the cap to $47.60/bbl, likely pushing most, if not all, Greek and other EU-owned vessels out of Russian trades. These vessels have only been active when the Urals price has been below the cap. Early next year, the cap will shift to a floating mechanism, essentially excluding discretionary tonnage from Russian trades on a more permanent basis.

This creates secondary effects. As discretionary tonnage withdraws, the shadow fleet, vessels operating almost exclusively in Russian trades, will need to compensate. Initially, this impact will be muted; when Urals previously dropped below the cap in March, existing supply remained sufficient to sustain exports. However, as previously covered, OFAC sanctions have already forced the shadow fleet to boost productivity. Crude freight rates from Russia stabilized after the January sanctions surge, but they could rise again later this year if additional incentives are needed to attract tonnage.

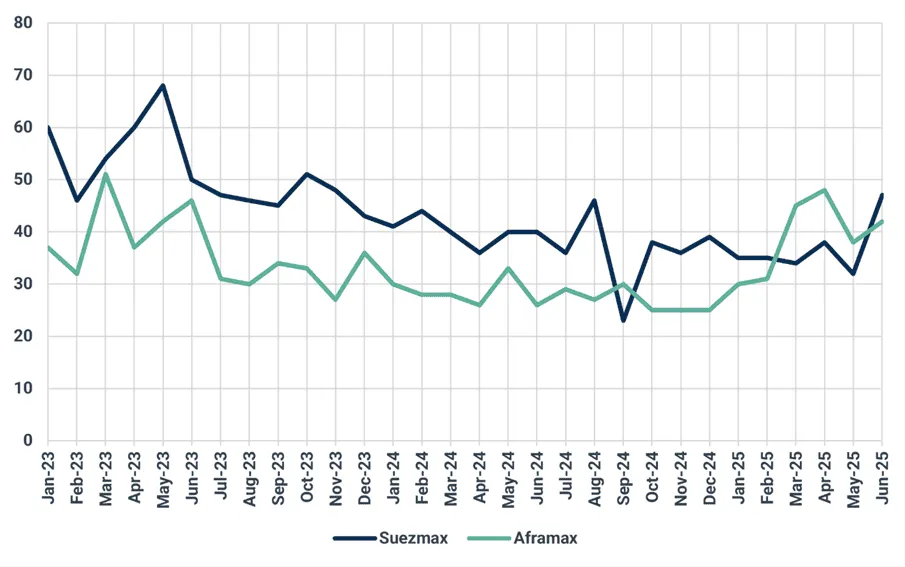

Russian crude cargo loads by Greek-owned tankers

Source: Kpler

Ban on imports of refined products made from Russian crude

In addition to revising the price cap, the EU will restrict imports of refined products made from Russian crude, even when refined in third countries. This will come into force on 21 January 2026. As discussed in this article, the primary impacts will be felt through EU imports from Turkey and India.

For the clean tanker market, the effect will be nuanced. A reduction in direct flows from India to Europe will have the greatest ton-mile impact. However, this shift may benefit conventional clean tankers.

So far this year, India has exported 227 kbd of clean products to Europe, and the largest share at 86 kbd was on Suezmaxes. The increased use of dirty tankers over the last year has been a thorn in the side of the clean market.

To offset reduced Indian flows, European buyers will likely pivot to the Middle East and the US. If the Middle East absorbs the increase in demand, LR tankers stand to benefit. So far this year, Middle Eastern exporters have only used Suezmaxes for 37 kbd out of a total of 850 kbd exported to Europe suggesting future flows will skew toward LRs. While it remains unclear how enforcement will be implemented, the measure may prove effective as a deterrent regardless.

Newly sanctioned vessels

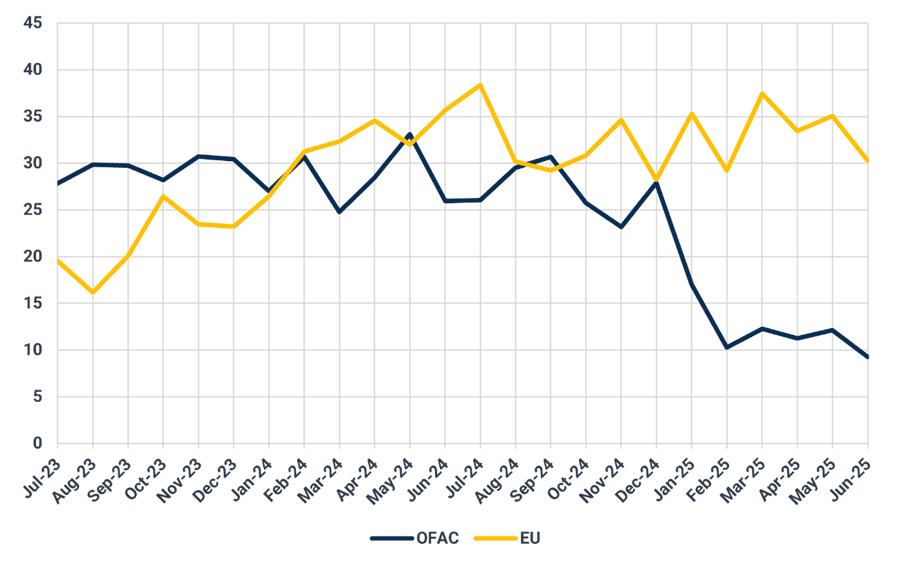

The third element of the latest package which impacts the tanker market was an additional round of vessel sanctions. There has been a net addition of 35 ships to the total list of sanctioned tankers.

We do not expect these sanctions to materially affect utilization of these vessels. Previous EU rounds have had minimal impact on ton-miles for sanctioned vessels. In contrast, OFAC sanctions, particularly those introduced in January, have proven far more effective at limiting vessel employment.

Russian crude export ton-miles on vessels only sanctioned by the EU and those sanctions by OFAC (Bn)

Source: Kpler

Want market insights you can actually trust?

Kpler delivers unbiased, expert-driven intelligence that helps you stay ahead of supply, demand, and market shifts.

Trade smarter. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler

Expert research & analysis driven by proprietary data