Sweeping EU sanctions risk destabilising an already-fragile gasoil/diesel market

Sweeping EU sanctions risk throwing the gasoil market into fresh turmoil just as balances begin to normalize. By targeting products refined from Russian-origin crude outside Russia, Brussels is disrupting a vital trade link — with India and Türkiye now scrambling to reroute flows that once bridged up to 20% of EU diesel demand. The near-term outlook is bullish for cracks, especially in the Mediterranean, but ICE Gasoil's muted reaction hints the market is fatigued, and eyeing alternative supply from the US Gulf and Middle East.

Market & Trading Calls

- Sanctions inject fresh volatility into an Atlantic Basin already running tight on gasoil

- Constructive for cracks, but muted ICE Gasoil reaction hints at some fatigue — price action has been relatively tame

- Mediterranean set to spike as India and Türkiye scramble to reroute and redocument flows

(Updated Monday 1030 GMT)

The EU’s 18th sanctions package is far-reaching. It includes a variable price cap on Russian oil — set at a floating discount to market rates — extends shipping sanctions to dozens more tankers, cuts off 22 Russian banks from the SWIFT transfer system, and targets the Nord Stream gas pipeline. Crucially, it also broadens restrictions to cover oil products refined from Russian-origin crude outside Russia (except Canada, Norway, Switzerland, the UK, and the US) — a controversial extension that challenges long-standing legal norms around substantive transformation.

For the first time, the EU has explicitly sanctioned Nayara Energy’s 405 kbd Vadinar refinery — citing Rosneft’s 49.13% stake. This marks a major escalation in scope: not only are products refined from Russian-origin crude now restricted, but facilities outside Russia with Russian equity ties are being directly targeted.

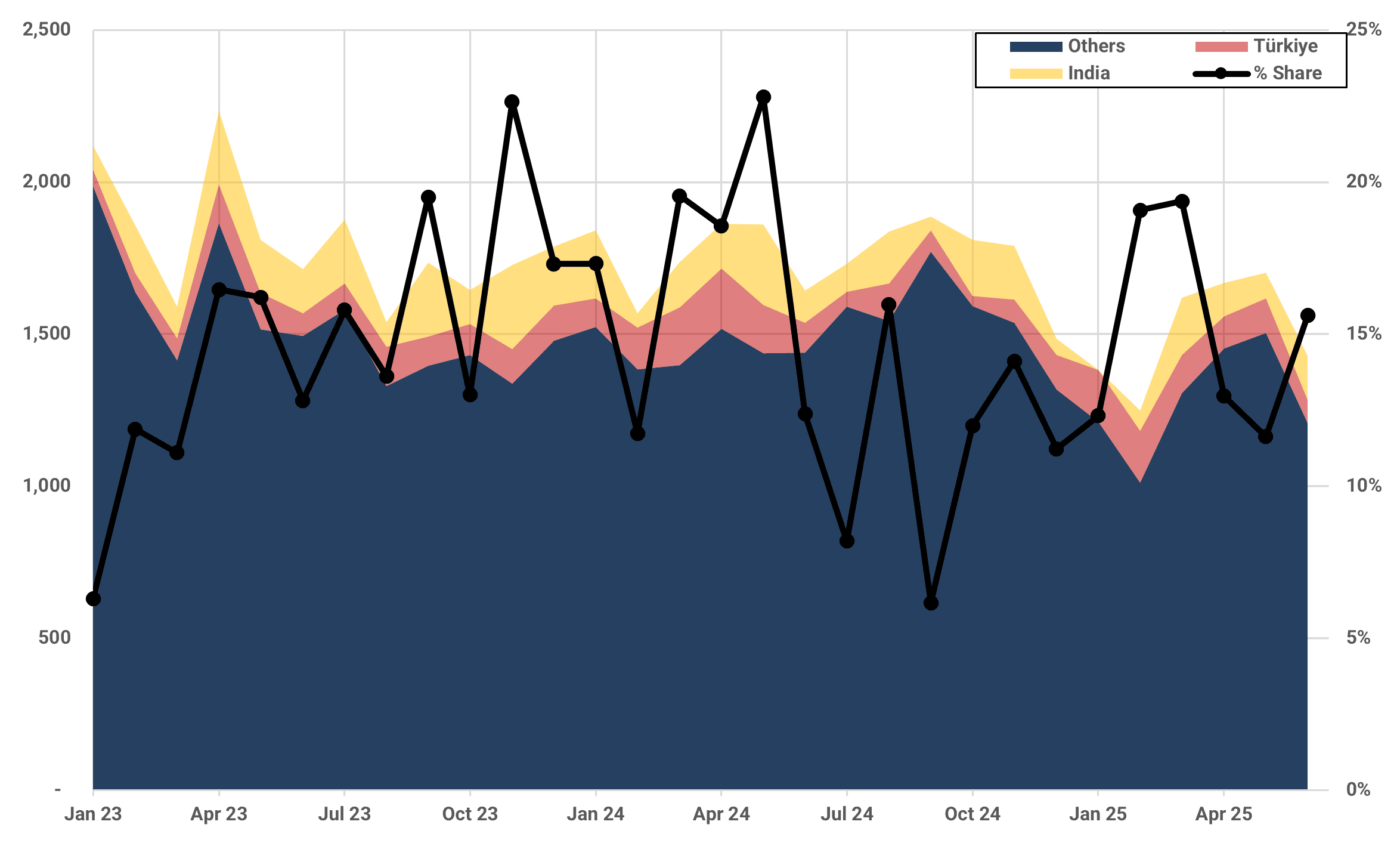

EU-27 imports (kbd) vs India, Türkiye market share % (RHS)

Source: Kpler

We have previously written about the legal grey zone this opens, and the real-world implications. The EU remains heavily dependent on gasoil and diesel refined from Russian crude — up to 15–20% of its imports. India and Türkiye have played a pivotal role in bridging this gap, importing a combined 2 Mbd of Russian crude and exporting over 200 kbd of gasoil to Europe. That trade route now risks disruption, either from regulatory risk or logistical paralysis.

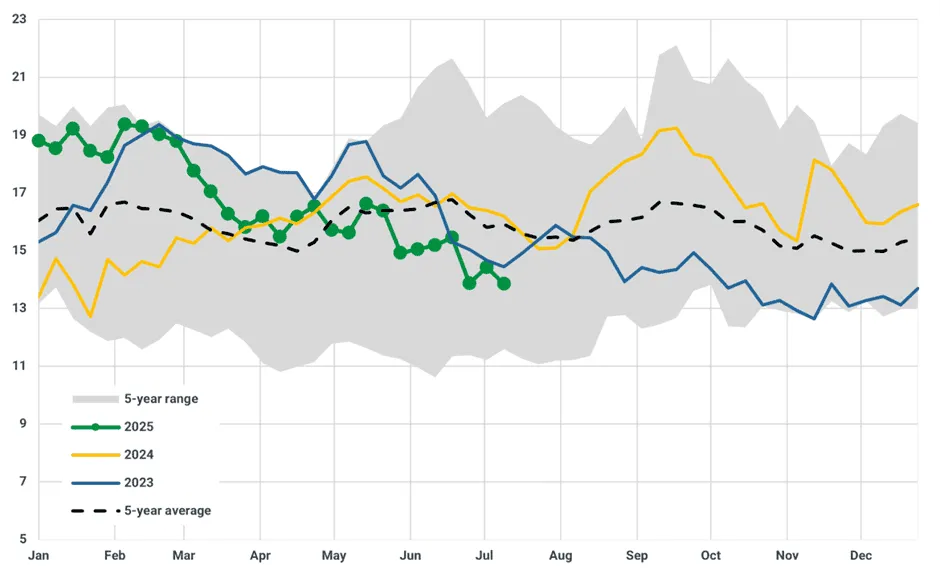

ARA: gasoil/diesel stocks in independent storages (Mbbls)

Source: Kpler using Insights Global

The timing could scarcely be worse. ARA gasoil/diesel inventories are sitting at 13.8 Mbbls — 14% below seasonal norms and hovering near multi-year lows. Atlantic Basin supply is visibly strained. But the market may already be on its way to easing. The prompt ICE Gasoil spread has rallied by around $9/t intraday — a relatively tame reaction that suggests speculative appetite is thin. As noted this week (see Middle Distillates), the barge market is showing early signs of easing, and some traders appear to be rotating out of length.

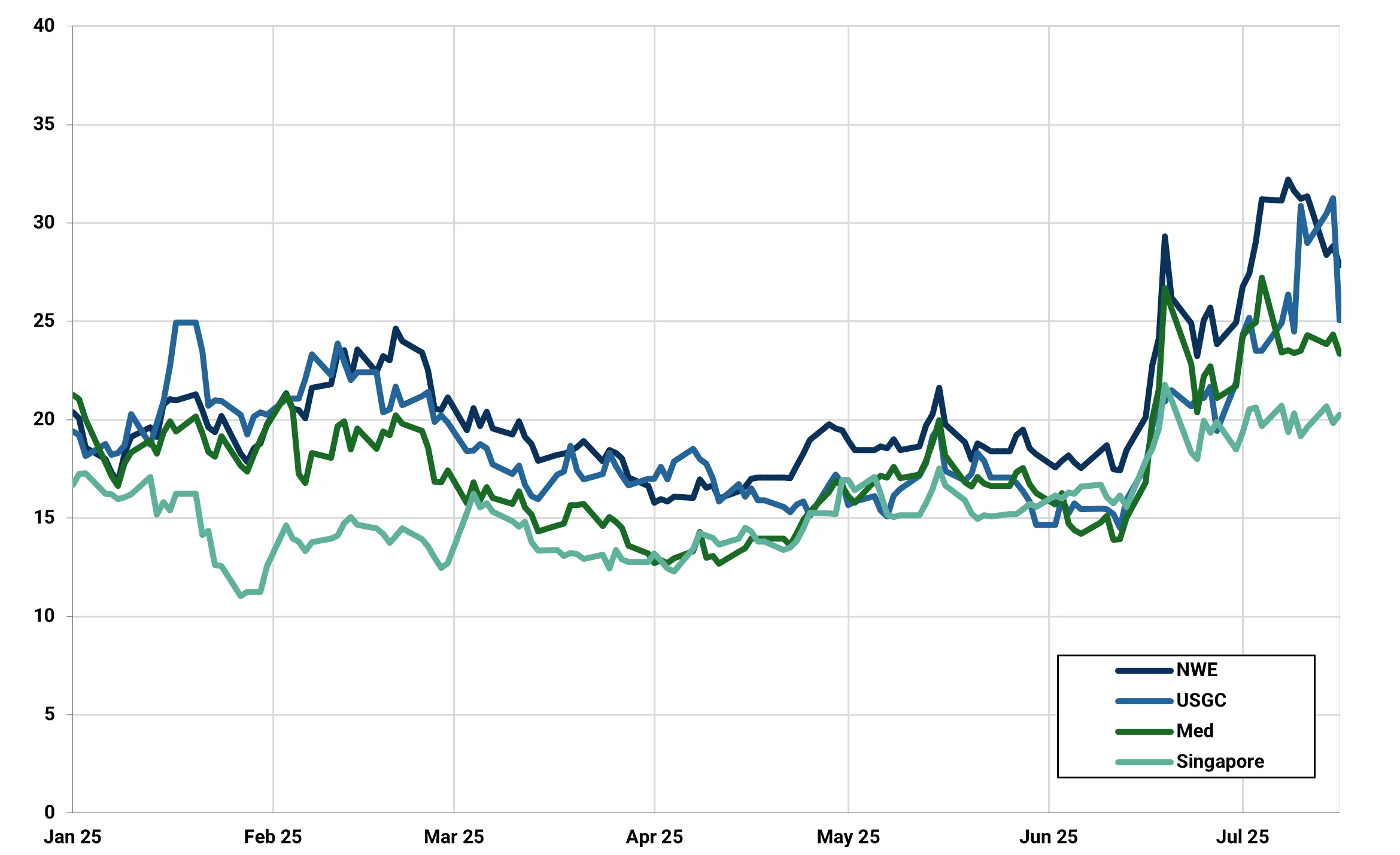

Global ULSD cracks ($/bbl)

Source: Kpler using Argus

Diesel on water bound for Europe is still running light — 22% lower y/y — but the arbitrage remains wide open. Spot flows from the USGC are incentivized at ~$4/bbl, and Middle East Gulf at ~$6/bbl. Both regions are well-positioned to step in, though timing and logistics remain critical.

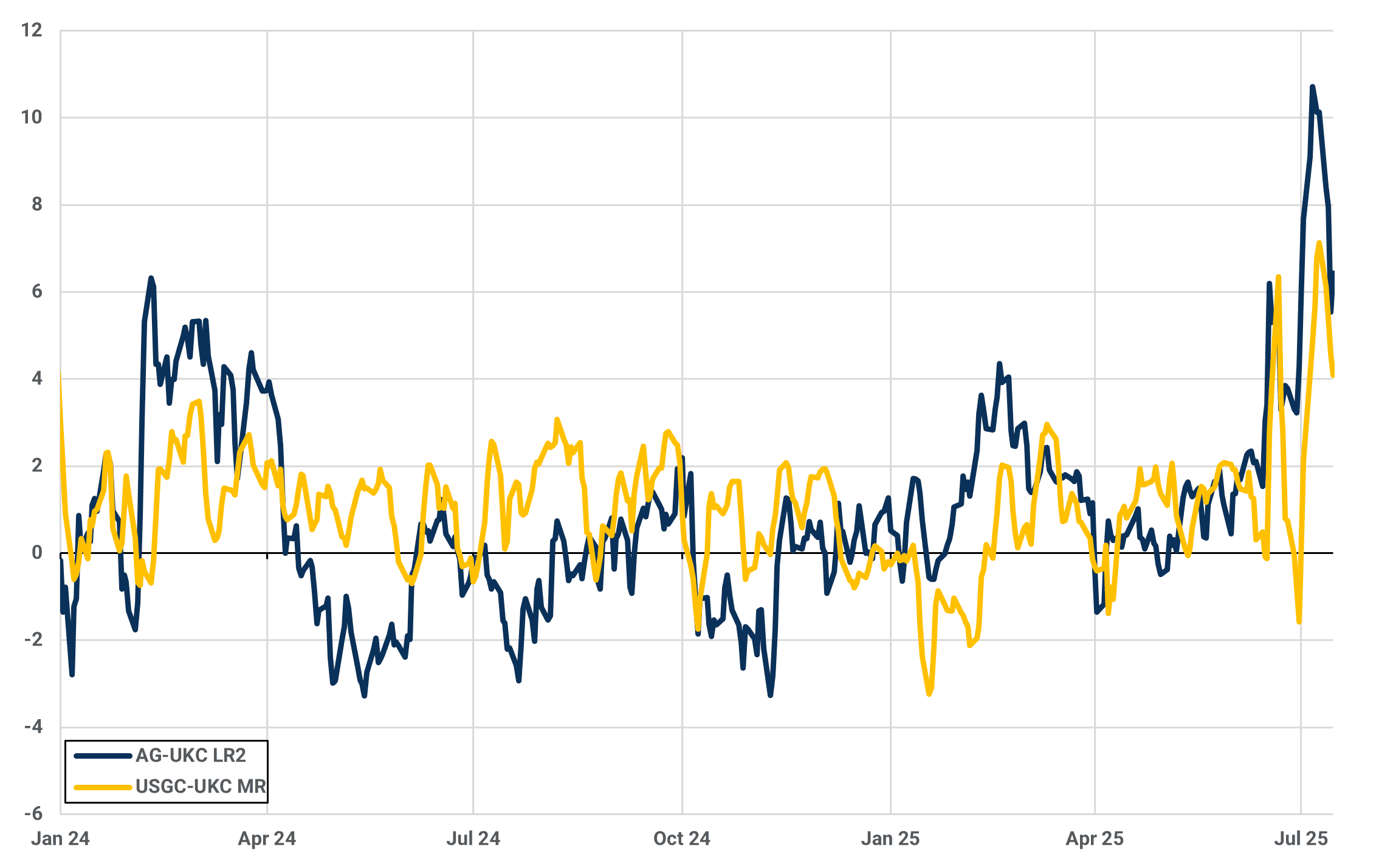

Arbitrage to NWE gasoil incentives 3 day moving average ($/bbl)

Source: Kpler using Argus

The Med is likely to feel the most immediate impact. With Türkiye now effectively constrained in its ability to re-export Russian-origin diesel, regional supply into EU ports will tighten. Indian and Turkish refiners are expected to pivot toward Africa and Latin America – crowding into Russia’s own export markets - while relying more heavily on established staging points in the Med and Middle East for possible blending and redocumentation. It will not be a seamless shift for some – Turkish refiners typically move Handysize cargoes, limiting flexibility. This rerouting adds friction, complexity, and cost, and it will take the market time to adjust.

Want market insights you can actually trust?

Kpler delivers unbiased, expert-driven intelligence that helps you stay ahead of supply, demand, and market shifts.

Trade smarter. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler

Expert research & analysis driven by proprietary data

Related posts