Crude oil: Top 5 market drivers in 2026

This article was first posted on Kpler Insight on 7 January.

After a volatile but mainly bearish 2025, the crude oil market enters 2026 in a seemingly awkward position. The year started with a bang with Maduro’s capture by the US, but this doesn’t change the picture fundamentally. Supply appears ample, inventories are rebuilding but Brent is anchored in the low-to-mid $60s. Yet beneath the surface, the market is becoming more fragile, more segmented, and more dependent on a narrow set of buffers.

The key questions for 2026 are not just about volumes, but about resilience: what could go wrong, who can absorb shocks, where supply growth is fading, who controls the marginal barrel, and why crude quality is once again shaping price formation. These five themes will define how tight or loose the market ultimately feels this year.

1. Geopolitics and sanctioned supply: resilience with rising friction

Sanctioned crude will continue to flow in 2026 but will become increasingly inefficient, raising risks for Russia, Iran and Venezuela.

Russia remains the anchor of sanctioned supply. Despite progress in Russia-Ukraine negotiations via the US, the talks still lack a major breakthrough. Therefore, Ukrainian drone strikes on energy infrastructure are likely to persist, supporting global refining margins. For Russia, it also raises operating and repair costs, meaning that reliance on oil sales to help keep the war financing system afloat will increase.

US sanctions on Rosneft and Lukoil are not likely to significantly decrease Russian seaborne exports, which are expected to remain broadly stable around 3.5 mbd. Then again, this may not have been their main goal. Sanctions are succeeding in deepening discounts, which are here to stay (approaching $8/bbl discount to ICE Brent and Oman/Dubai for ESPO and Urals into China and India, respectively). In parallel, the dark trading ecosystem is becoming more expansive to sustain.

Lower oil revenues will debilitate Russia’s ability to outmanoeuvre the US on Ukraine. Persistent outflow to floating storage (which ended at 10 mbbls at the end of 2025) could result in marginal (~100 kbd) production shut-ins. Ultimately, this could push Moscow to agree to a partial deal. This will not result in a worldwide normalisation of Russian oil flows (immediately) but will incentivise more buying in Asia and allow Russia to invest in its upstream sector.

Beyond Russia, Iran and Venezuela represent heavy geopolitical risks this year. The swift regime shift in Venezuela and erupting protests in Iran could lead to wider political changes, which will have a bearish long-term impact (measured in years) but will sustain prices this year. In the short-term, maintaining the US blockade on vessels could dent supply by some 200 kbd by February, and Iran’s exports could also decrease due to a combination of stricter sanctions and domestic spillage onto the oil sector. Nonetheless, global balances are long enough to cushion such losses without a major impact on oil prices.

Rising floating storage, which hit a 3-year high of 123 mbbls, building at a pace of 650 kbd since early September, are not just indicative of a weak oil market. The three quarters of the volumes originate from Iran, Russia and Venezuela, pointing to further political weakening due to higher discounts and, ultimately, lower revenues. Venezuela could see a relatively smooth political transition, potentially leading to a removal of sanctions later in the year, but risks around Iran and Russia are also high.

Market implication: The security of sanctioned barrels is going to weaken this year, embedding a persistent geopolitical risk premium into prices.

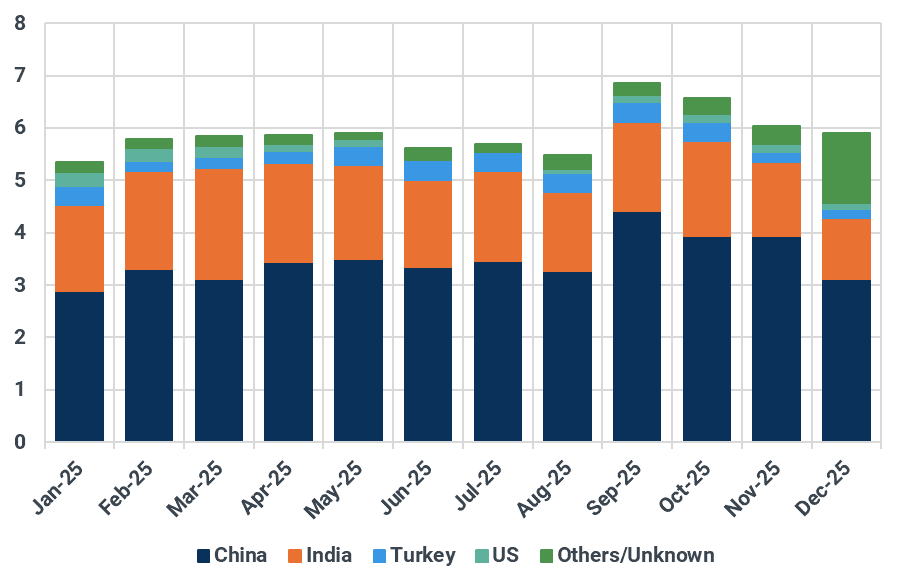

Russia, Venezuela & Iran seaborne crude exports by destination, Mbd

Source: Kpler. Includes loaded volumes that have not been sold yet and remain in floating storage

2. China’s crude stockpiling: the market’s shock absorber

China’s stockbuilding was a critical pillar of oil demand in 2025 and will remain a key stabiliser in 2026.

Rising risks around supply of sanctioned crude partly explains why China added substantial volumes to onshore inventories last year. Total onshore stocks built by 100 mbbls to historically high levels of 1.2 bn bbls, equivalent to over 100 days of imports and 77 days of consumption. This was driven by the launch of 32 mbbls in new storage capacity, opportunistic buying at low prices, and government mandates to refill strategic reserves.

Beijing could issue another round of SPR refilling orders or unofficially encourage refiners to maintain relatively high inventory levels in 2026 to cushion against potential supply disruptions, particularly given the country’s reliance on imported crude for around 75% of total demand.

Stockbuilding could repeat 2025’s pace and may even accelerate. China is set to bring online around 94 mbbls of new onshore storage capacity, alongside an estimated 200 mbbls of underground capacity. Even filling just 10% of nameplate capacity would generate roughly 30 mbbls of incremental demand.

If utilisation rises toward 60%, China could add up to 170 mbbls of crude stocks, equivalent to nearly 500 kbd over the year. This would help absorb a large portion of the 1.8 mbd surplus we foresee for this year, rovide a crucial floor to prices. With uncertainty around future supply of heavy sour crude from Venezuela, stockpiling will become even more strategic this year.

Market implication: China may not be driving demand growth in the traditional sense, but in 2026, it could once again act as the oil market’s shock absorber.

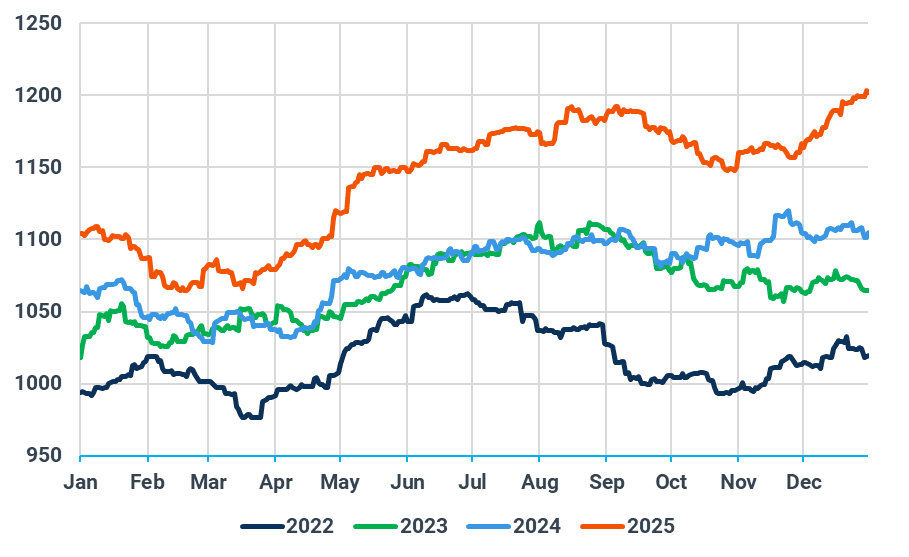

China onshore oil inventories, mbbls

Source: Kpler

3. The end of US crude supply growth

After a decade of expansion, US crude supply is finally set to plateau, and then decline.

US output averaged record levels of 13.6 mbd in 2025, up roughly 400 kbd y/y, but momentum is fading. Lower drilling activity, shrinking DUC inventories and rising decline rates are beginning to outweigh productivity gains. Mature basins such as the Bakken are already contracting, while growth in the Permian is slowing sharply. We expect output to have peaked near 13.8 mbd in late 2025 before falling back toward 13.6 mbd by end-2026. In this context, President Trump insisting that the US wants to control Venezuela’s oil could make sense: if US output is to decline in the long-term, Washington needs to have some sway over incremental oil supply in the Western hemisphere.

Non-shale supply offers little offset. Gulf of Mexico production will rise, but volumes are limited and skew sour. With Brent prices expected to remain in the $60–65/bbl range, there is little incentive for a renewed surge in upstream investment. While the average new well across all US shale basins is now producing roughly 100 b/d more than a year ago, with the current rate exceeding 1 kbd, lower activity and declining DUC inventory are keeping the current growth trajectory unsustainable. For the first time in years, the US is no longer the market’s automatic safety valve.

The rest of non-OPEC+ supply is likely more resilient this year, yet is grappling with the same natural declines as the US. Investments and new FPSOs should fuel Brazil and Guyanese output to fresh highs (4.28 Mbd and 893 kbd respectively). Canadian output is also set to rise, but runs the risk of climate-related production hiccups as in previous years, while Norway’s flagship Johan Sverdrup field is already declining from its plateau of 750kbd.

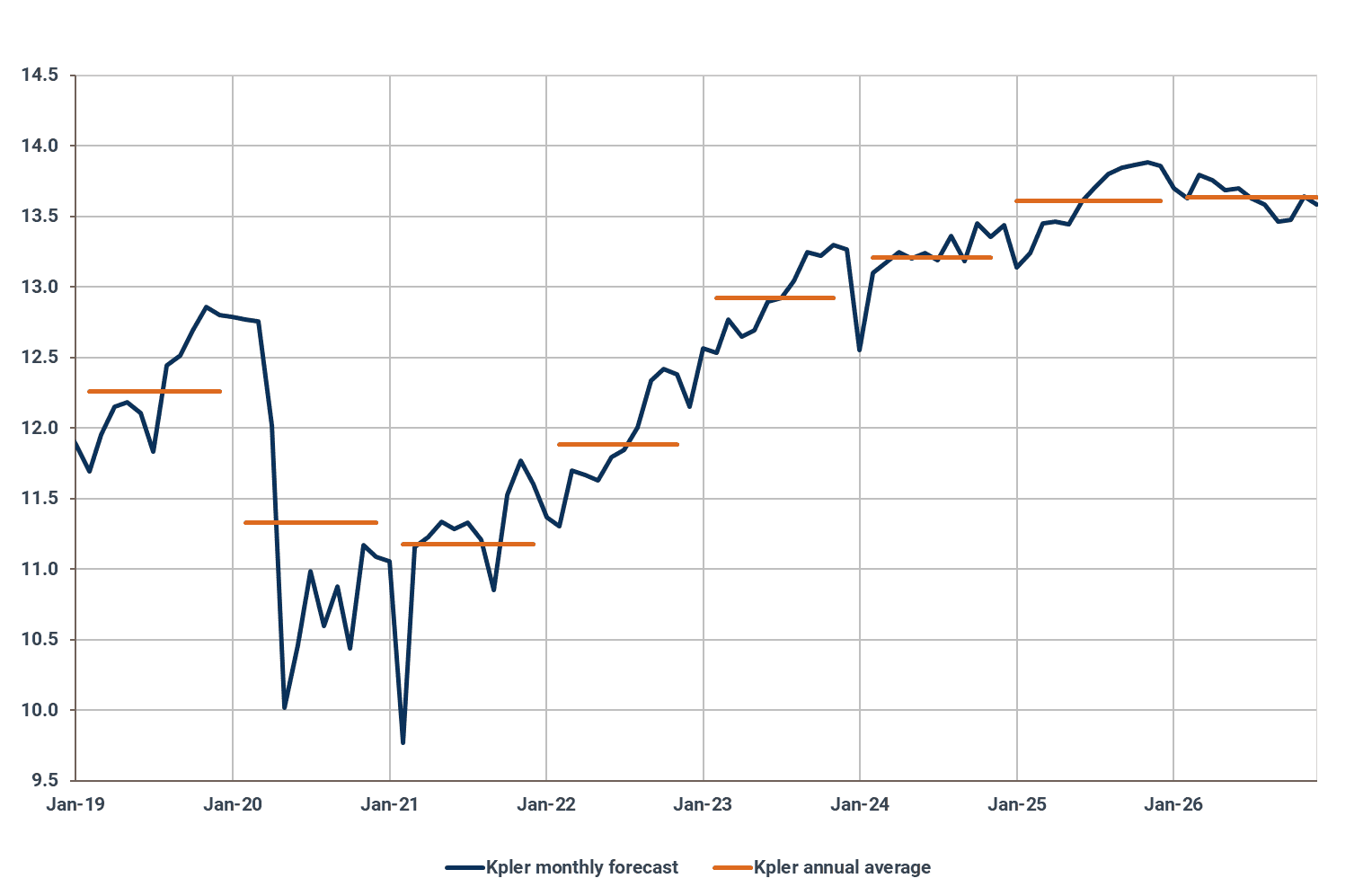

US crude and condensate supply, Mbd

Source: EIA, Kpler

Market implication: Any disappointment in non-OPEC+ supply will increasingly translate into tighter balances and a greater reliance on the OPEC+ response.

4. OPEC+ in 2026: optionality over certainty

OPEC+ enters 2026 with a clear strategy, but no fixed path.

After front-loading supply in 2025, the group has paused further headline increases through Q1 2026, citing the seasonal oversupply that typically characterises the first quarter. This pause does not signal a shift toward restraint. OPEC+ has repeatedly emphasised flexibility, retaining the ability to add supply, pause further increases or reintroduce cuts depending on how market conditions evolve.

The base case remains that the group of eight resumes production increases in Q2–Q3 if demand behaves as expected, with our global oil demand growth forecast at around 1.3 mb/d in 2026, close to OPEC’s own forecast. However, the group has been equally explicit that it will step back if inventories build too quickly or prices come under renewed pressure. In that sense, policy direction in 2026 is conditional rather than pre-committed.

This flexibility serves two strategic objectives. First, OPEC+ continues to prioritise regaining market share from non-OPEC+ producers, a process that accelerated in 2025. Second, the group is deliberately working to reduce spare capacity. Since early 2025, OPEC+ spare capacity has fallen sharply, and the group appears comfortable allowing it to shrink further.

By lowering spare capacity while maintaining the ability to respond quickly, OPEC+ increases price upside in the event of non-OPEC+ supply disappointments or geopolitical disruptions, whether from Russia, Iran or Venezuela, while still retaining the tools to cap downside if the market becomes oversupplied.

Lastly, tail risks such as renewed internal tensions within the alliance, reminiscent of the pandemic, remain low probability but cannot be fully dismissed. Although tensions between Saudi Arabia and the UAE over Yemen increased, OPEC+ cohesion remains a priority.

Market implication: OPEC+ is positioning itself to cap downside while preserving upside, making prices more convex to shocks.

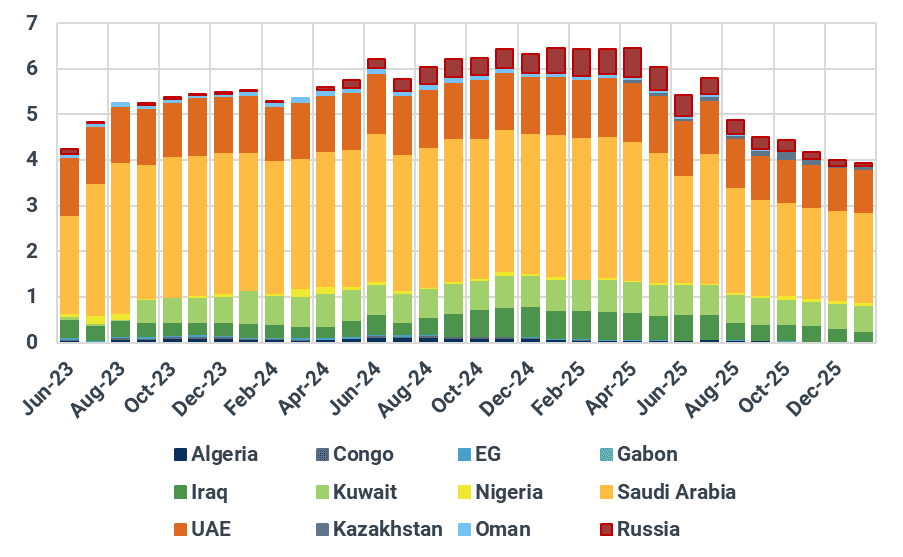

OPEC+ crude oil spare production capacity, Mbd

Source: Kpler

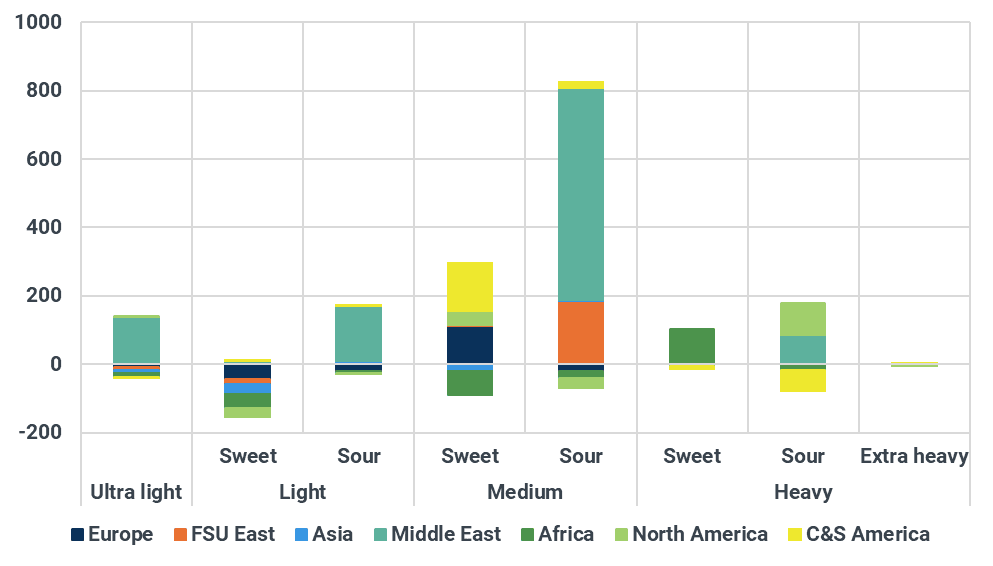

5. Crude quality in 2026: the market turns decisively sour

The crude market in 2026 will not just be about how much supply is available, but also what quality of barrels dominate.

Global crude supply growth is set to tilt increasingly toward sour grades this year, reinforcing the widening trend in sweet–sour differentials already visible since mid-2025. While non-OPEC+ supply growth is slowing, OPEC+ spare capacity remains concentrated in medium sour grades. Saudi Arabia, Iraq and the UAE account for most potential incremental barrels, and even in the UAE, new supply will lean more heavily toward medium sour streams than light sour Murban.

Even allowing for short-term volatility in Venezuelan output, growth in sour crude supply is expected to significantly outpace that of sweet crude in 2026. Our current balance assumes broadly stable OPEC+ output, yet even under this conservative scenario, sour output growth exceeds sweet by a wide margin. Should OPEC+ proceed with further production increases in Q2–Q3, the quality imbalance would become even more pronounced, as any return of withheld volumes would amplify the sour overhang.

Even in the US, the same pattern is evident. A plateauing Permian and declining Bakken will weigh on light sweet availability, while Gulf of Mexico output is set to reach a record near 2 mbd, composed predominantly of sour grades. Outside the US, Brazil and Guyana provide limited relief through medium and light sweet growth, but volumes from Búzios and Golden Arrowhead are insufficient to offset the broader shift.

This imbalance has already pushed sweet–sour spreads wider, particularly following the surge in OPEC+ exports in late 2025. While new East of Suez refining capacity may eventually absorb more sour crude, most projects only ramp up from H2 2026. In the interim, wider quality differentials, and a wider Brent–Dubai EFS, will increasingly shape flows and price formation.

Market implication: The supply mix is becoming structurally more sour, and wider quality differentials remain the path of least resistance.

2026 y/y crude and condensate supply growth by quality and origin, kbd

Source: Kpler

Conclusion: a comfortable market set for a transition year

At first glance, 2026 appears oversupplied. However, the market is increasingly underpinned by a narrow set of stabilisers: rising Chinese inventories, fading US supply growth and OPEC+’s ability to manage the marginal barrel actively. Meanwhile, geopolitically exposed supply continues to flow, but with rising fragility, leaving Iran and Venezuela as potential sources of short-term disruption.

While disruptions are more likely to trigger temporary price bounces rather than sustained spikes, 2026 could mark the year in which the oil market’s balance of risks begins to tilt modestly back to the upside.

Want market insights you can actually trust?

Kpler delivers unbiased, expert-driven intelligence that helps you to track critical crude oil market developments for your own analysis. Our precise forecasting empowers smarter trading and risk management decisions.

Unbiased. Data-driven. Essential. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler